Key events in developed markets next week

- 8 October 2021

- Key Events

Look out for speeches from members of the Bank of England, as well as UK employment and GDP data. US jobs numbers and the eurozone’s industrial production numbers are also key figures to watch

US: Fed tapering on the horizon

Assuming the US jobs numbers come in close to consensus (we are still awaiting publication at the time of writing) we can be pretty sure that the Federal Reserve will announce the tapering of its QE asset purchases at the 3 November FOMC meeting. Indications from officials suggest they want this concluded by the summer, which implies a reduction in asset purchases of $15b each and every month starting from December. The coming week’s data shouldn’t change this outlook.

The key report to watch will be September’s consumer price inflation. After a reopening spike in key areas we have seen the rate of price increases moderate, but it is still faster than we saw pre-pandemic with higher food and housing costs particularly evident. This will keep the YoY inflation rates elevated with the risk being that they rise further in coming months given supply chain issues and inventory shortages as we go into the key holiday season.

Other releases include the National Federation of Independent Businesses sentiment survey and the key area we will be focusing on is the price intentions series. We have seen an increasing proportion of companies looking to raise their prices in an environment where costs are going up and demand is strong. This improving pricing power will keep consumer price inflation higher for longer and expectations for Fed rate hikes inching higher. Meanwhile, retail sales will be dragged lower by the plunge in vehicle sales. This is more a function of a lack of supply than a drop-off in demand given the dearth of inventory to sell, the ongoing production bottlenecks and the fact second hand car prices are up 45% this year. Outside of autos, the figures should remain positive with rising incomes and surging household wealth providing strong underpinnings.

UK data unlikely to test market’s Bank of England conviction

Markets are pricing almost three UK rate rises by the end of 2022, and expectations for earlier hikes have been fuelled by recent rises in energy prices. Given the UK’s chronically low gas in storage, further power price pressure is possible. However, we aren’t convinced this makes a rate hike more likely – and if anything, it is a dovish factor given it’ll act as a brake on consumer activity. Instead, the prospects of tightening hinge on wage growth and here, hopes may get a lift from another solid jobs report.

Weekly data points to another fall in the three-month unemployment rate, and hiring data generally has pointed to an encouraging recovery in demand over recent months. Vacancies are high, though we’re also likely to see some redundancies over coming months as the furlough scheme ends. The impact on unemployment may not be huge, partly because some of the job losses will show up as ‘inactive’.

In short, the jobs market is in a state of mismatch. So the question for policymakers is whether the sharp pay rises in shortage roles (e.g. lorry drivers) spread elsewhere – and the jury’s still out. We think the cost of living spike over the winter means caution is likely to prevail at the Bank of England, and we’re not expecting the first rate rise until May 2022. We have a couple of BoE ‘doves’ in the calendar next week too, and it’ll be interesting to see if they push back on current market pricing.

Separately, we’ll get August’s GDP figures which are likely to see a bit of a pick-up in growth after July’s stagnation. High-frequency data points to roughly 0.5% growth for the month.

Eurozone: Dip in production expected but trade continues to increase

The eurozone focus will be on manufacturing this week as trade and production data are set to be released for August. Shortages continue to bite on the production front, and expectations are for another decline in August. Despite all of the supply chain frictions and transport problems, trade continues to increase though. This will make the August trade balance an interesting figure to watch to get a bit of a sense of how net exports will perform in the third quarter.

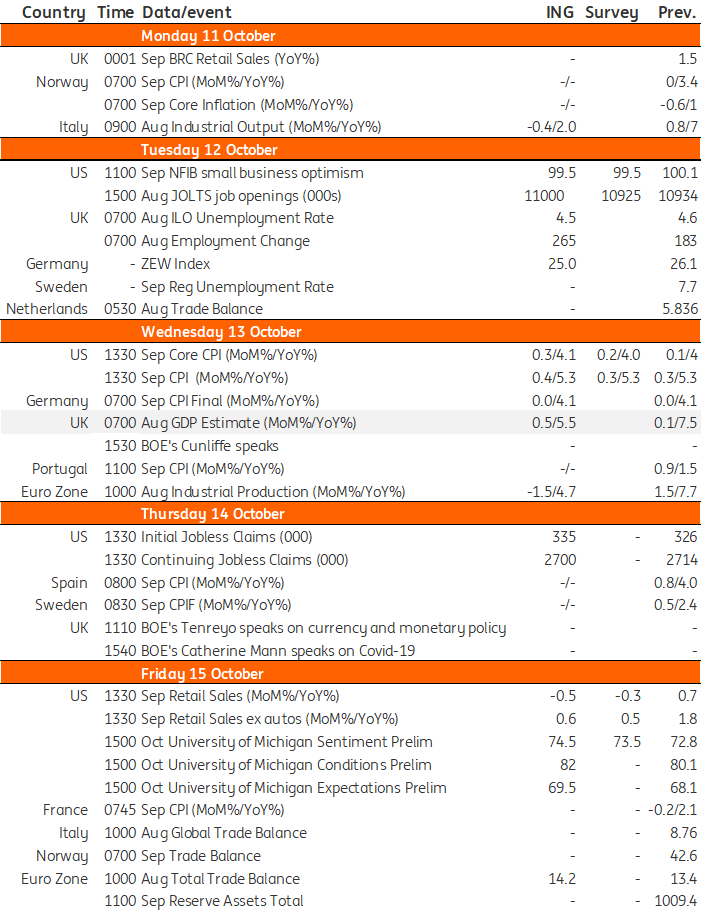

Developed Markets Economic Calendar

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more

Authors

This article is part of the following bundle

Our view on next week’s key events

- This bundle contains 3 Articles