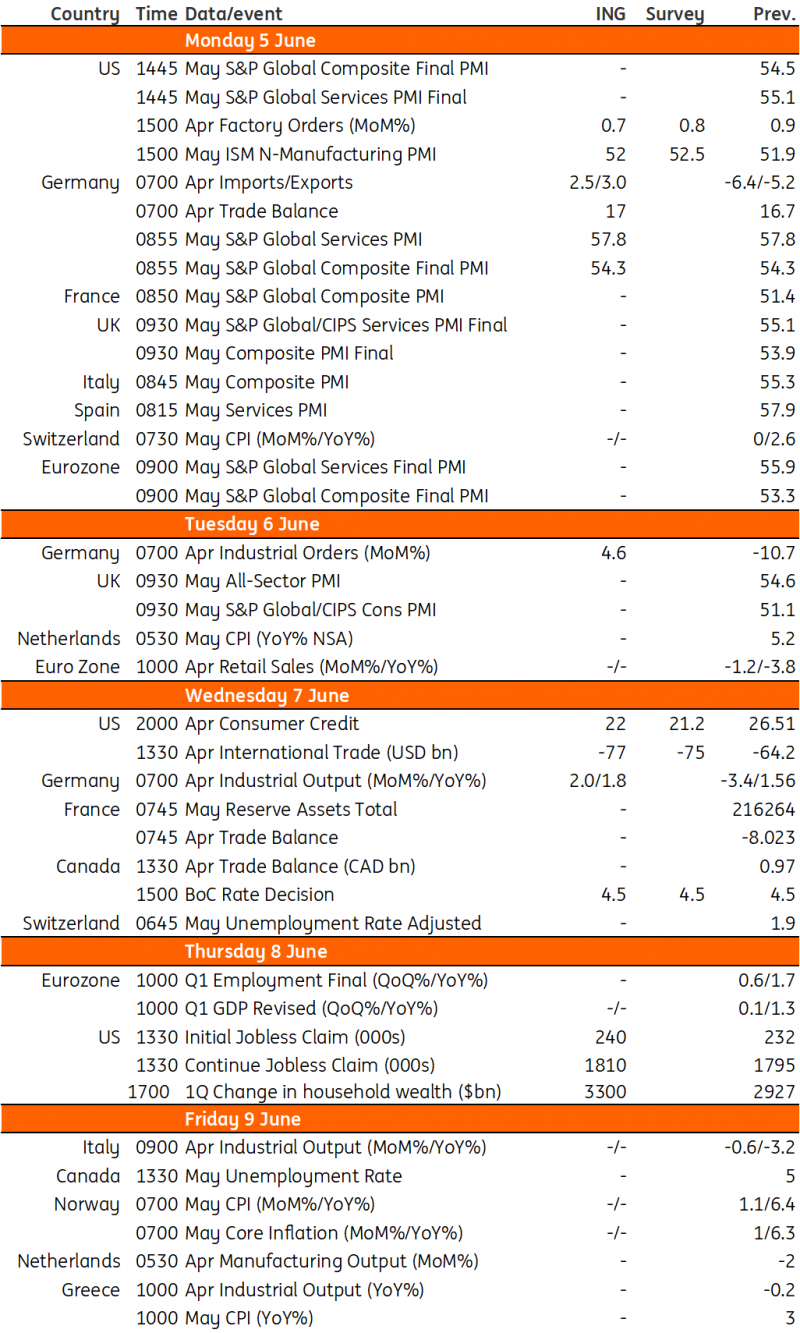

Key events in developed markets next week

The Bank of Canada will announce its latest monetary policy decision on Wednesday. We favour a hawkish hold as GDP and consumer price inflation have been stronger than expected, and the labour market remains robust. The US data flow in the coming week is unlikely to move markets much given the CPI release in the following week

US: All eyes on May core inflation

Market expectations for whether the Federal Reserve will hike interest rates again have swung wildly over recent weeks. Currently, the favoured narrative is that the Fed has raised interest rates significantly and tighter lending conditions will act as a brake so it may be best to hold rates unchanged at the June FOMC and re-evaluate the situation in July. If the jobs market is still hot and inflation continues to track well above target, they can then hike again. Nonetheless, there are hawks on the FOMC and if May core inflation, released 13 June, comes in at 0.4% or higher, the decision could become a very close call. With the Fed entering its quiet period ahead of the decision, there will be no officials discussing the outlook for monetary policy over the coming week. The data flow includes the ISM services index, inventory numbers, the trade balance and consumer credit together with an update on the state of household and corporate balance sheets in 1Q, published by the Federal Reserve. While interesting, they are not going to move markets much given the importance of CPI the following week.

Canada: A hawkish hold

The Bank of Canada is set to announce its latest monetary policy decision. The consensus is for no change, but after stronger than expected consumer price inflation and GDP and with the labour data remaining robust the market is pricing a 25% chance of a hike on 7 June with a 25bp hike fully discounted by the 6 September policy meeting. The BoC last raised rates on 25 January and has held them at 4.5% since then. The last statement warned that they were prepared to raise the policy rate further to ensure inflation returns to 2% and Governor Tiff Macklem stated that the bank remains concerned about upside inflation risks. Nonetheless, they also accept that monetary policy operates with long and varied lags. Consequently, we favour a hawkish hold, signalling that unless there is evidence of softening in price pressures very soon, they could raise rates again in July.

Key events in developed markets next week

Download

Download article2 June 2023

Our view on next week’s key events This bundle contains {bundle_entries}{/bundle_entries} articlesThis publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. Read more