Key events in developed markets next week

- 1 April 2022

- Key Events Canada United States

April rate hikes are firmly on the table in the US and Canada with this week’s second-tier releases unlikely to hinder central bank plans

US: Subdued consumer sentiment will limit upside for PMIs

The US data calendar is largely second-tier releases this coming week with the ISM services index the likely highlight. It has fallen sharply over the past three months from an all-time high of 68.4 in November to a 12-month low of 56.5 in February. The Omicron wave was likely responsible for the bulk of the decline, although the squeeze on spending power from surging inflation may also have hurt demand. We are hopeful of a corrective bounce in March, but with consumer sentiment remaining subdued and a growing sense that aggressive interest rate hikes are on their way, the upside for the ISM is likely to be limited.

We will also be closely following the minutes of the March Federal Open Market Committee meeting. The Federal Reserve raised interest rates 25bp and has since signalled more aggressive 50bp moves are firmly on the table at upcoming meetings. At the accompanying press conference, Chair Jerome Powell suggested that the Fed would soon announce plans to shrink its $9tr balance sheet, and some details could emerge from the minutes.

Powell suggested that the run-off will be similar in structure to 2017-19, but could happen at a faster pace. The Fed could potentially announce such action at the May meeting, but it could come later if it wants to see how a series of 50bp hikes are digested by markets. We suspect it will start how it ended the last round of quantitative tightening – by allowing $50bn of maturing assets to run off their balance sheet each month. This could quickly be stepped up to $100bn given the doubling in size of the balance sheet since the start of the pandemic.

Canada: Strong employment figures could boost rate hike expectations

In Canada, there is a growing likelihood that the central bank will follow up its initial 25bp rate hike in early March with a 50bp move in April. The Canadian economy has recovered all output lost during the pandemic while employment is at all-time highs and inflation is running at the fastest rate since 1991. This week’s data flow includes the March jobs report and another gain is expected after February’s post-lockdown surge. We will also get the quarterly Bank of Canada business outlook survey and a firm reading here given Canada’s strong commodity production background amid surging prices could boost expectations for a 50bp hike on 13 April.

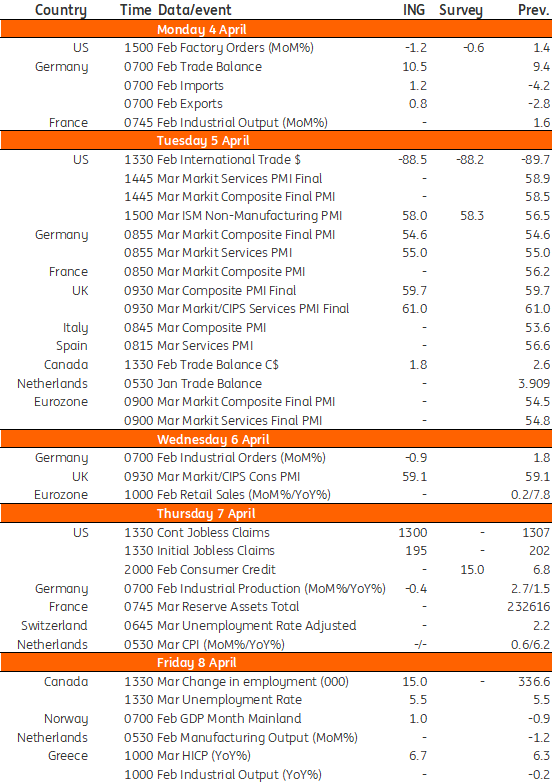

Developed Markets Economic Calendar

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more

Included in the following bundle

Our view on next week’s key events

- This bundle contains 2 Articles