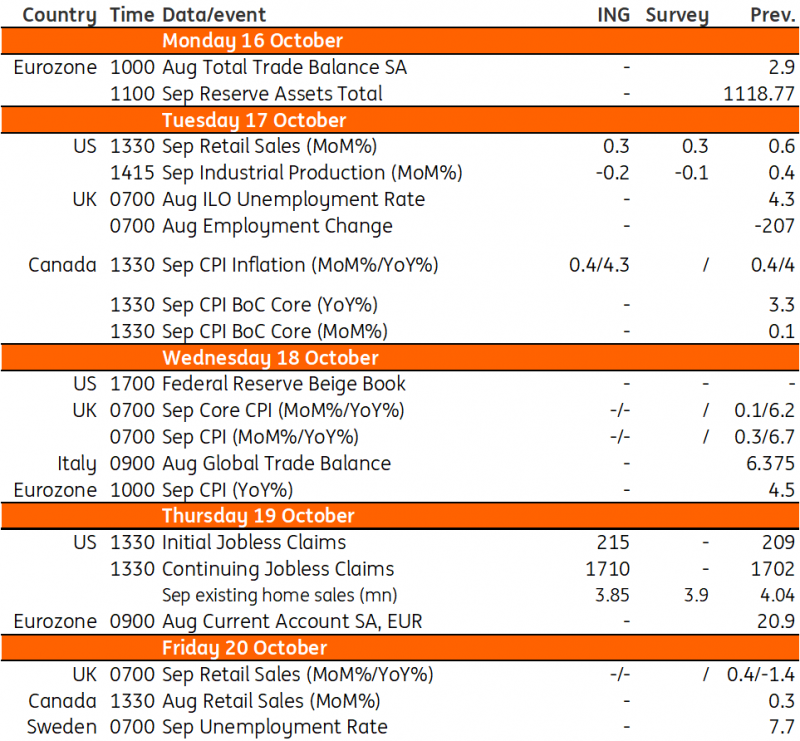

Key events in developed markets and EMEA next week

In the US, we expect retail sales and industrial production to show signs of weakness. In Canada, all eyes will be on the CPI as a hot reading could make a rate hike more likely at the end of the month. Over in Poland, an increase in the minimum wage is putting upward pressure on average wages

US: retail sales expected to show evidence of weakness

The US economic outlook is becoming more uncertain with geopolitical tensions adding to the perception that the Federal Reserve is likely finished tightening monetary policy. Indeed, this has been the main theme from Fed speakers despite US inflation figures suggesting a certain degree of "stickiness" persists in the core services sector. The grinding higher of longer-dated Treasury yields is amplifying the monetary policy tightening with Boston Fed President Susan Collins arguing this is generating "some tightening of financial conditions. If it persists, it likely reduces the need for further monetary policy tightening in the near term.

The market is currently pricing in a one-third chance of a final 25bp rate hike this year and that could decline further if we are right and the details of the retail sales and industrial production report show evidence of weakness. Headline retail sales will be lifted by higher vehicle sales and higher gasoline prices, but strip these out and it is likely to be a far weaker report. High-frequency credit card spending numbers have been soft in September and that is normally a good barometer of direction for general spending trends. The Fed's Beige Book and the minutes of the FOMC meeting also mentioned growing evidence of household savings being run down and in an environment where real household disposable income has been shrinking, the pressure on household finances is growing. Industrial production may show a modest rise in manufacturing, but the risks are skewed to the downside from auto-related strike action which has not only impacted vehicle production but also hurt suppliers. Lower oil and gas drilling could also weigh on total industrial production, as will utilities.

Also watch the Fed's new updated Beige Book for anecdotal evidence of a further softening in activity. Last time, they mentioned concerns about the prospects for consumer discretionary spending while commenting that the "last stage of pent-up demand for leisure travel from the pandemic era" was likely over. Meanwhile, housing data will soften further with very weak pending home sales pointing to existing home sales dropping below a 4mn annualised rate, which was last seen during the global financial crisis. Mortgage rates are fast approaching 8% and this will also hurt home builder sentiment and limit the upside for housing starts.

Canada: hot CPI data will make rate hike more likely

Just to mention briefly that in Canada, CPI will be closely followed given the uncertainty over whether the Bank of Canada will hike again at the end of this month. A hot print could make it close to a 50-50 call. Currently, there is a one third chance priced in.

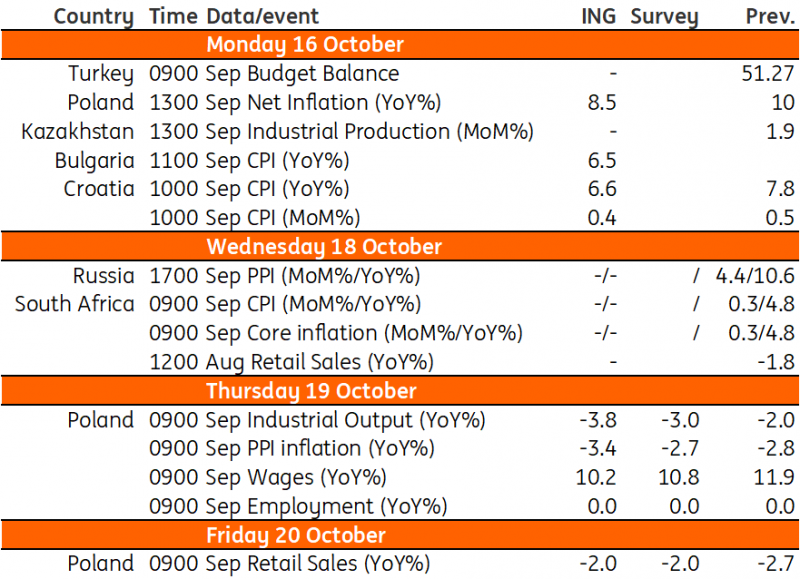

Poland: minimum wage growth boosts average wages

Industrial output (September): -3.8% YoY

New manufacturing orders continue to shrink, albeit at a slower pace. We forecast that manufacturing output in September was substantially below levels seen a year earlier, partially as a result of the lower number of working days this year. Global trade and conditions in German industry remain unfavourable, but recent PMI readings suggest some signs of stability and chances for improvement ahead.

PPI (September): -3.4% YoY

Despite an upswing in global crude oil prices and the zloty weakening against the US dollar last month, wholesale gasoline and diesel prices declined markedly in September (down by around 6.5% month-on-month on average). We project prices in other key sectors of manufacturing declined as well, driving producer prices down by 0.4% MoM, and pushing headline PPI inflation down 3.4% YoY. Deflation is expected to continue in the coming months.

Wages (September): 10.2% YoY

Average wages and salaries in the enterprise sector are projected to have eased to 10.2% year-on-year in September from 11.9% YoY amid a higher reference base and lower number of working days, which should translate into slower growth of wages in manufacturing. Demand for labour is cooling down in some sectors of the economy but remains solid in various services. At the same time, minimum wage growth is putting upward pressure on average wages.

Employment (September): 0.0% YoY

Employment in the enterprise sector has stopped growing in recent months. We forecast a slight decline in the level of employment in monthly terms which should not have an impact overall. Despite poor economic conditions, there are no substantial lay-offs in the economy as labour is scarce due to supply-side factors. The working-age population is shrinking and some of the immigrants are leaving Poland.

Retail sales (September): -2.0% YoY

Falling inflation and strongly rising nominal wages are translating into improving real disposable income of households. As a result, we see some green shoots in retail sales and expect a turnaround in the coming months. We forecast that in September, retail sales fell by 2.0% YoY vs. -2.7% YoY in August. Consumers seem to be finally close to finding solid ground after a long period of freefall.

Key events in developed markets next week

Key events in EMEA next week

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. Read more

Download

Download article

13 October 2023

Our view on next week’s key events This bundle contains 2 Articles