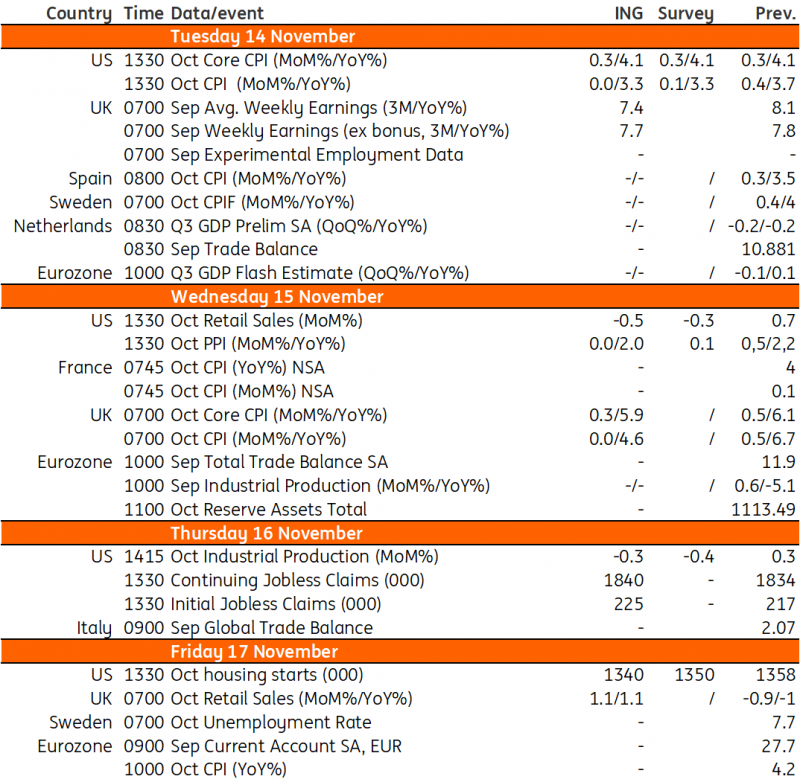

Key events in developed markets and EMEA next week

The BoE is set for yet another ‘on hold’ decision in December – barring any enormous data surprises, that is. Over in Poland, we expect third-quarter GDP growth to come in positive, while in Hungary we should see the country's technical recession coming to an end

US: CPI and PPI expected to come in flat on the month

Federal Reserve Chair Jerome Powell again acknowledged last week that monetary policy is “restrictive”, but remains unsure as to whether it's restrictive enough for inflation to return sustainably to 2%. We think it is, and we do not expect any further Federal Reserve interest rate hikes from here on out. This view should receive some support from upcoming data, including both consumer and producer price inflation along with retail sales and industrial production data for October.

The steep plunge in gasoline prices will have a major influence and could allow headline CPI and PPI to come in flat on the month, while also depressing the values of retail sales to the extent that we get a negative month-on-month reading. We already know that vehicle sales were down on the month and that credit card spending has also been subdued, pointing to a soft spending number. Industrial production is also subject to downside risk given that the ISM manufacturing index is in deep contraction territory. Meanwhile, housing starts look set to fall based on the long-run relationship with home builder sentiment. This has been damaged recently by mortgage rates hitting 8%, which appears to have been a catalyst for a big slowdown in prospective buyer traffic.

Core inflation readings may come in a bit higher with 0.3% MoM increases, though. This may keep markets on edge to some extent, but over the coming months, we expect to see slowing housing rents exert a greater influence – and this should lead to US consumer price inflation slowing to 2% by next summer. See our latest note on the outlook for US inflation for all the details.

UK: Bank of England set for another ‘on hold’ decision in December, barring any enormous data surprises

The messaging coming from the Bank of England suggests that the recent tightening cycle has indeed finished, not least because policymakers have now kept rates on hold at two consecutive meetings. We agree, and we think the next move in rates is likely to be down, with cuts starting next summer. But next week’s data is important, especially given that the inflation release will be the only one before the December meeting (although we’ll get one more set of wage figures, in addition to the ones on Tuesday). Headline inflation is set to take a big leap downwards, and that means Prime Minister Rishi Sunak can claim he’s been able to ‘half inflation’ as targeted earlier this year. That’s an artefact of electricity prices, and the fact that last year’s 25% increase in energy bills drops out of the annual comparison – and on top of that, prices fell by roughly 10% at the start of October.

By contrast, services inflation is likely to stay unchanged at 6.9%, and this is the area the Bank is most wary about. However, we expect more noticeable progress here next year as the lagged impact of lower gas prices and weaker demand reduce pressure on firms to raise prices. Private sector wage growth is likely to ease off fractionally in next week’s numbers, but we’d expect this to fall back to the 4% area by next summer. The jobs market does appear to be cooling, but issues with data collection mean that it’s hard to reliably say how quickly.

Barring any enormous upside surprises in both the services inflation and wage figures next week, we think the Bank will be comfortable with keeping rates unchanged again in December.

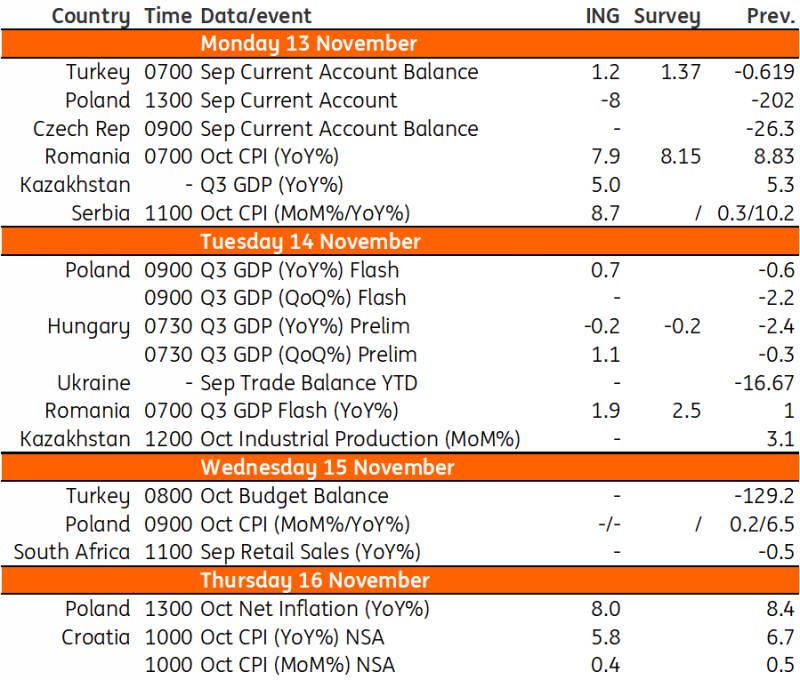

Poland: GDP expected to turn positive again in the third quarter

Current account (Sep): €-8 million

Poland’s foreign trade balance has been running positive since the beginning of 2023 as the most acute phase of energy shock abated and import prices started moderating. We forecast that in September the current account was broadly balanced, with surpluses in trade in goods and services covering negative gaps of primary and secondary income accounts. We estimate that in September exports fell 3.9% year-on-year, while imports nose-dived 12.7% YoY. In such a scenario, the 12-month cumulative current account surplus likely improved to 0.6% of GDP vs. 0.3% of GDP after August.

Flash GDP (3Q23): 0.7% YoY

According to our forecast, GDP turned positive again in the third quarter of 2023, expanding by 0.7% YoY after two consecutive quarters of annual declines. The biggest improvement is expected in household consumption, which we expect fell by only 0.2% in the third quarter, while fixed investment expanded by 7.5% YoY. The drag from change in inventories should be substantially lower than in the recent quarters. At the same time, a positive contribution from net exports was probably smaller than it had been previously. For 2023, we estimate economic growth at 0.4% before an acceleration to at least 2.5% in 2024.

CPI (Oct): 6.5% YoY

We expect the flash estimate of October CPI inflation at 6.5% YoY to be confirmed. The composition of price developments is likely to confirm that core inflation rose by 0.6% MoM after a decline of 0.1% MoM in September. It should still bring core inflation down to 7.9-8.0% YoY from 8.4% YoY in the previous month. At the end of 2023, headline inflation should be at levels close to those seen in October, with visibly lower core inflation. In 2024 we see annual average inflation around 5%.

Hungary: In our view the technical recession is coming to an end

The highlight of the week in Hungary will be the third-quarter GDP data. We expect a turnaround after four quarters of negative GDP growth on a quarterly basis. In our view, the technical recession is coming to an end. And it won't be a small improvement. The incoming high-frequency data points to strong growth (1.1%) on a quarter-on-quarter basis. Industrial production has improved compared to the second quarter, while a massive increase in August could turn the construction sector into a positive contributor to GDP growth. The services sector was boosted by a strong tourism season. Last but not least, agriculture could surge due to favourable weather conditions this year. This solid quarterly growth brings the year-on-year GDP index close to, but still below zero.

Romania: Inflation expected to decelerate further to 7.9%

Next week, we expect to learn that inflation decelerated further to 7.9%, mainly on the back of lower price pressures for food items. We also expect preliminary GDP data for the third quarter to show that the economy decelerated into an almost-stagnating state in quarter-on-quarter terms, but should still post a relatively decent 1.9% annual growth. This will be mostly due to a deterioration in private consumption, which robust investment activity and better data from the trade balance may find tricky to offset. A big unknown which could tilt the balance towards a positive surprise comes from the agriculture sector.

Key events in developed markets next week

Key events in EMEA next week

Download

Download article10 November 2023

Our view on next week’s key events This bundle contains {bundle_entries}{/bundle_entries} articles

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. Read more