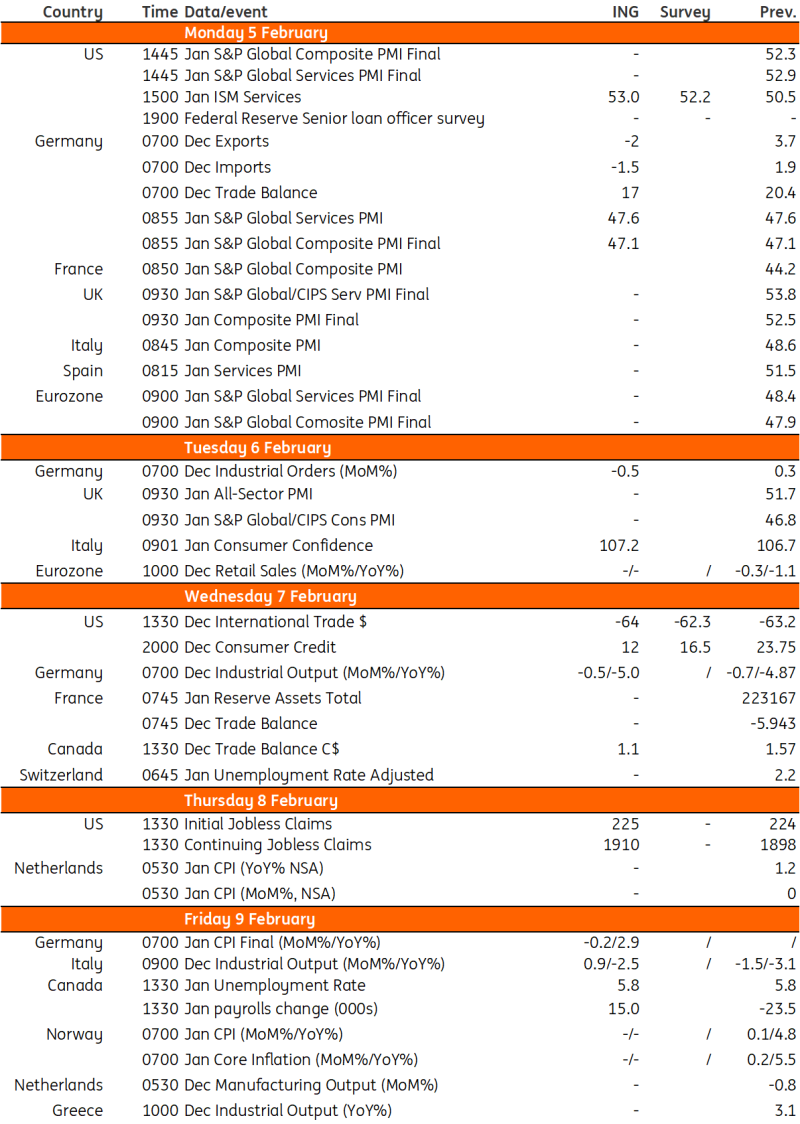

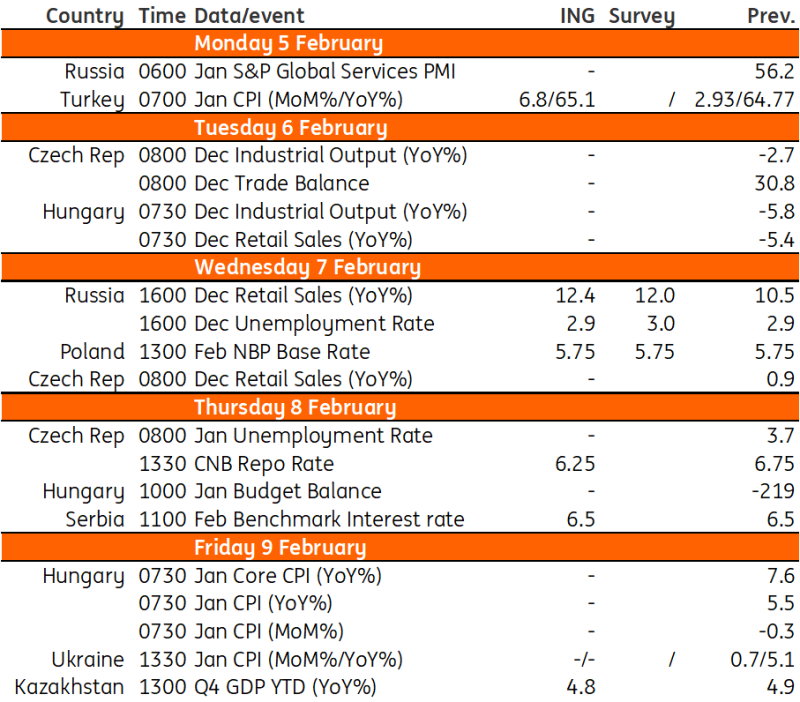

Key events in developed markets and EMEA next week

A quiet week ahead in the US features the ISM services employment component as the main data release to look out for. In the CEE region, we expect the National Bank of Poland to keep rates unchanged, while optimistic forecasts could see the Czech National Bank increasing the pace of its rate cuts to 50bp. In Turkey, inflation is likely to remain under pressure

US: ISM services employment in focus

The Federal Reserve has firmly pushed back against the chances of a March interest rate cut and the market now accepts our long held view that May will be the start point for the Fed’s policy easing cycle. Inflation is heading in the right direction, but the economy is still posting decent growth rates and the labour market remains tight. We suspect that the Fed recognises its credibility was damaged by its "inflation is transitory" assertion in 2021, only to have to rapidly reversed course with significant rate hikes through 2022 and 2023. The last thing the Fed wants to do is get it wrong again at a key turning point by loosening too soon, too quickly and reigniting inflation pressures. It'll therefore be waiting for more data to fall into line, and once it's comfortable, we expect a series of rate cuts that will see the Fed funds rate down at 4% by the end of the year and 3% by summer 2025.

It is a relatively quiet week for data, with Monday the main day of interest. The ISM services employment component collapsed in January, deep into contraction territory, catching everyone by surprise. It has been brushed off as a rogue data point by markets, but if we see a repeat, it'd be a huge story and could see the market refavouring a March cut once more. Later in the day we have the Federal Reserve’s Senior Loan Officer Opinion survey. This has an excellent lead relationship on bank lending and is currently pointing to lending turning negative in year-on-year growth terms. We expect it to indicate that fewer banks tightened lending conditions in the fourth quarter – but that's a long way from saying that conditions are becoming easier. Bank caution – likely reignited by recent headlines surrounding New York Community Bancorp’s struggles – may mean that lending remains constrained through the current quarter.

Poland: February MPC meeting to keep rates unchanged

The National Bank of Poland's reaction function has seen a shift since the country's elections from ultra-dovish to neutral. The central bank's rationale behind that is the uncertain inflation outlook. NBP Governor Adam Glapiński suggested the Council would eye macro data and review its policy in March, after acknowledging the new NBP staff macro projection. The short-term inflation outlook improved markedly vs. the November projection. The mid-term prospects are a bit more uncertain (i.e., the timing of rising VAT on food and lifting the freeze on energy and gas prices), but still, the inflation picture is not too different than before the elections.

Still, Governor Glapiński has stated that he'd be unwilling to take any steps before gaining more knowledge about mid-term CPI path and the balance of risks. Given the expected inflation upswing in the second half of this year, the room for NBP rate cuts seems narrow (25-50bps), but markets bet on an aggressive rate cuts over the next 12 months. This month, the MPC will keep rates unchanged despite a disappointing performance for the economy in the fourth quarter of last year amid stagnant household consumption.

Czech Republic: Optimistic forecasts could speed up the pace to 50bp rate cuts

The Czech National Bank will meet on Thursday next week and will present its first forecast published this year. We are going into the meeting expecting an acceleration in the cutting pace from 25bp in December to 50bp, which would mean a cut from the current 6.75% to 6.25%. This means a revision in our forecast, which previously saw an acceleration taking place in March. Still, it's certain to be a close call given the cautious approach of the board – which could bring about a 25bp cut. The board will have a new central bank forecast, which is likely to be a key factor in decision-making. Here, we see the need for revision in a few places, but overall everything points in a dovish direction.

We see from public statements that the dovish wing of the board will push for a faster pace of rate cuts given inflation numbers indicating a quick return to the 2% inflation target this year, and that it may be open to more than 50bp of rate cuts. For the rest of the board, we think the inflation indication for January and beyond in the central bank's new forecast is key. We are currently expecting 2.7% for January headline inflation, with room for it to come in lower if the anecdotal evidence of January's repricing is confirmed. This, in our view, will give the rest of the board the confidence to accelerate the pace of cutting as early as this meeting.

Turkey: Inflation expected to be 65.1% in January

Inflation will likely remain under pressure in the near term given a higher-than-expected minimum wage hike and increases in administrative prices due to special consumption tax and revaluation rate related adjustments. Accordingly, we expect the annual figure to be at 65.1% in January (with 6.8% month-on-month reading) vs 64.8% a month ago

Key events in developed markets next week

Key events in EMEA next week

Download

Download article2 February 2024

Our view on next week’s key events This bundle contains {bundle_entries}{/bundle_entries} articles

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. Read more