Key events in developed markets next week

- 14 June 2019

- Key Events

Politics and central banks dominate next week. The race to become the UK's next leader is well underway, and throw in an important European Council Meeting, a possible Norges Bank hike and the Fed appearing come off its “patient” stance, we have a very exciting week ahead

Fed: An Easing Bias

At this stage, neither China nor the US seem willing to make the required concessions to get a deal done on trade, and if anything it looks as though tensions will escalate further in the near term, with a strong likelihood Europe and Japan are sucked into the malaise. The recent US data flow suggests the economy is becoming less resilient to the negative trade headlines than it was in late 2018 with payrolls numbers and manufacturing figures a clear cause for concern. We are now seeing a shift in language from Federal Reserve officials, with the term “patient” seemingly having been dropped with regards their assessment of on the timing of whether a change in interest rate policy was going to be required. Consequently, we believe that they will use the June FOMC meeting to signal an easing bias.

This would perhaps be through repeating Jerome’s Powell use of the “closely monitoring” phrase and downward revisions to their economic projections and their “dot” diagram, which currently has a rate hike in for 2020. We imagine they will be pencilling in one, possibly two rate cuts into their revised forecasts. Financial markets are currently pricing for 100bp of rate cuts, but we think President Trump wants to get a deal done ahead of next year’s Presidential election and this could limit policy easing to precautionary cuts amounting to 50bp. We favour September and December rate cuts.

Race to become the UK’s next leader set to move to the next stage

Through a series of votes, the contenders to be the next leader of the UK Conservative party will be whittled down to a final short-list of two. As things stand, the former foreign secretary is odds-on to win, once the final two are put to a vote of party members. At face value, his comments suggest he would be prepared to take the UK out of the EU without a deal. However, in this case, we think parliament would vote down the government, and the risk of a late-2019 election is rising.

All of this uncertainty is continuing to weigh on economic growth, and data from the British Retail Consortium indicates that May was another tricky month for the high street. Despite a modest improvement in real wage growth over recent months, confidence remains low among shoppers. Elsewhere, core inflation is set to remain below target which adds another reason for the Bank of England to stay on hold next week. We don’t expect rates to shift during 2019, particularly given the possibility of an election later this year. But given the better news on wage growth over the past six months or so, we wouldn’t be surprised to hear the Bank talking up the possibility of earlier/faster rate hikes than implied by a virtually flat market curve.

Eurozone: A 'meaty' Council meeting

Next week, the eurozone will focus on Brussels for a meaty European Council meeting. Quite a few things are on the agenda, including the EU budget and strategic agenda. The market focus will be on top EU jobs haggling that will happen during the meeting. Whether decisions will actually be made remains to be seen as this game of musical chairs is particularly challenging with no less than five key positions up for grabs.

After all that, leaders will discuss EMU reform on Friday afternoon. Will leaders still have the energy to put the hammer down on eurozone reform or will there just be small steps announced? The latter seems more likely. Also, keep an eye out for the PMIs and consumer confidence as concerns about the eurozone economy persist. With regards to the German economy, its another light week, with only the ZEW index to look out for.

Norges Bank set to hike rates and signal more to come

The Norges Bank told markets last month that it intended to hike interest rates at its June meeting. The bigger question now is how it adapts its interest rate projection for the rest of the year.

The economy is benefitting from an energy-driven spike in investment, and this is also translating into wage growth. Meanwhile, the Norwegian krone has weakened since the last projections, not strengthened as the central bank had assumed. This should translate into a steeper near-term interest rate projection, with a further rate hike possibly pencilled in for later this year. However, this will be tempered by the recent dip in oil prices and it's, therefore, possible we see a more gradual interest rate forecast further out.

We currently expect another rate hike in December.

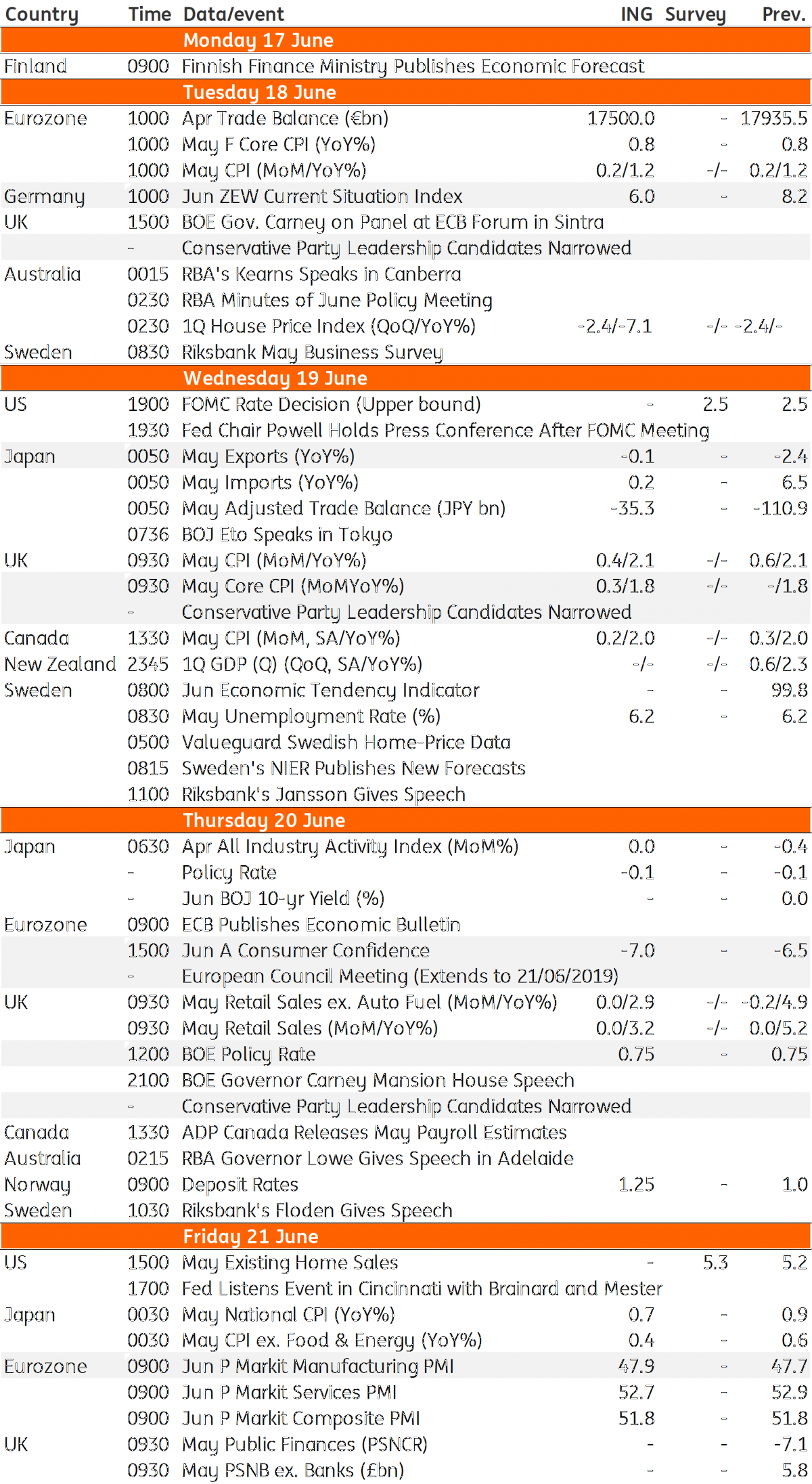

Developed Markets Economic Calendar

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more

Authors

Included in the following bundle

Our view on next week’s key events

- This bundle contains 3 Articles