Keeping an eye on private markets’ not so private vulnerabilities

The growth and influence of Non-Bank Financial Intermediaries are facing heightened scrutiny. Private markets, in particular, are attracting significant interest. The sector’s inherent opacity, links with the broader financial system, competition with banks, and increasing vulnerabilities make it an interesting sector to watch in 2025

Why you should keep an eye on NBFIs and private markets

Non-Bank Financial Intermediaries (NBFIs) have grown significantly since 2008 and as a result, the sector's influence has come under increasing scrutiny. One part of the sector, private markets, recently came under the spotlight due to its significant growth and the competition it represents for banks.

Private equity and credit entities have expanded their influence in today's economy by financing higher-risk corporations and providing a quicker, more flexible source of funding. However, their inherent lack of transparency, ties to the broader financial sector, and the lack of regulatory oversight indicate that their vulnerabilities may soon become more apparent.

We view the potential direct impact of stress in private markets on the banking sector as limited. However, indirect impacts could be more significant. Indeed, the growing interconnectedness within NBFI and with banks increases contagion risks to the broader financial sector.

Additionally, retail investors’ growing interest in private markets and the consequent increase in open-ended funds could also cause a shock spillover to the real economy and ultimately affect banks through higher default rates and lower credit quality. Considering all these points, we believe regulators and the banking sector should keep an eye on private markets in the coming year.

How is the NBFI sector doing?

The term NBFI is used to describe a large variety of institutions. We classify them as non-banks that take in cash and use it to generate a return. Most NBFIs take in cash, just as banks do, and deploy it in various securities and derivatives.

Part of the complexity of understanding and analysing the sector stems from the various ways of subdividing it. Different international institutions use distinct classification methods for NBFIs. The ESRB, for instance, separates Pension Funds and Insurance Companies, categorising the rest into two main groups: Investment Funds and Other Financial Institutions (OFIs). The graph below illustrates a non-exhaustive approach to viewing the different NBFI sub-sectors.

Non-exhaustive NBFI sector sub-division

In this article, we won’t explore each sub-sector individually. Instead, we’ll assess the challenges posed by the broader NBFI sector and delve into the specifics of private markets. Private markets encompass, but are not limited to, private equities and private credit entities. Before turning to the sector’s vulnerabilities and what this means for banks, an update on NBFI developments is necessary.

NBFI's significant growth after the 2008 Global Financial Crisis mainly stems from the stricter capital and liquidity requirements on banks. These made some parts of lending less attractive for the banking sector. Therefore, NBFIs took over portions of this business as regulatory requirements grew for banks. Read more on this in our previous piece here.

Nowadays, the crucial role played by NBFIs in the broader economy is widely acknowledged. The share of assets held by the sector increased continuously between 2011 and 2019 to reach more than 50% of total global assets. However, since 2020, the sector’s total asset size has stagnated, remaining between $215tr and $230tr. Furthermore, as global financial assets have grown, the NBFI sector’s share decreased to 47% of total assets in 2022.

NBFI's share of global financial assets dropped by nearly 3pp in 2022

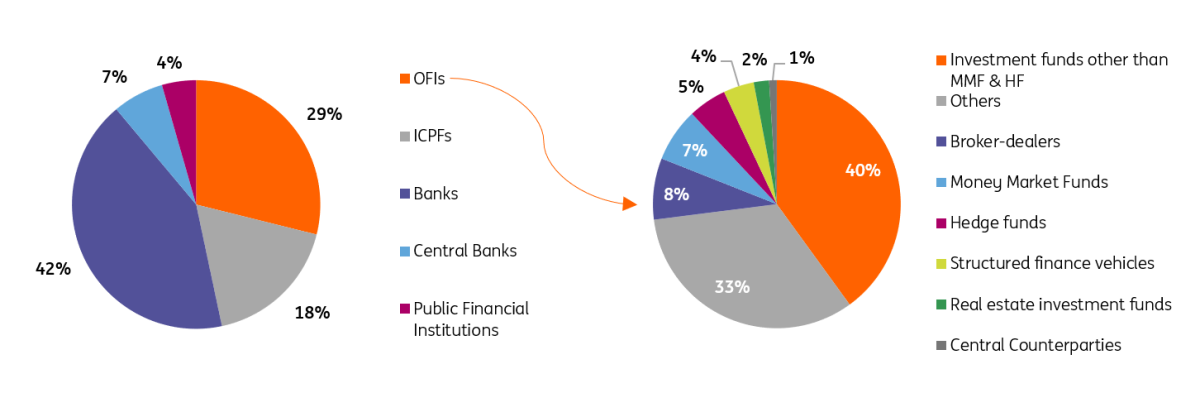

Data from the Financial Stability Board (FSB) indicates that a very large part of the NBFI sector is composed of insurance companies and pension funds (the aggregate of these two segments is known as ICPFs). At the end of 2022, ICPFs accounted for 18% of global financial assets, while other financial intermediaries (OFIs) made up 29%.

The OFI segment remains extremely diversified. Indeed, 7% of it is composed of Money Market Funds, 8% of broker-dealer entities and 40% is a diversity of investment funds.

Insurance companies and pensions funds represent 18% of global financial assets

At the European level, data shows that despite significant growth over the last two decades, NBFIs are not yet as developed as they are globally. Looking at the sector excluding pension funds and insurance companies, the largest entities are equity funds followed by bond funds and mixed funds, each representing 17% of EU NBFI assets at the end of 2022.

Largest share of European OFIs are equity funds

Private markets, an opaque but growing sector

Four percent of European OFIs are private markets. Private finance entities aim to provide funds to companies, mostly unlisted ones, via debt and equity investments. It therefore provides alternative funding sources to companies aside from public equity, corporate bonds markets and bank lending. The European Central Bank (ECB) underlines the importance of the sector as it provides financing to riskier entities through the risk-bearing capabilities of long-term investors.

Private markets are composed of unlisted assets, private equity (investing in firms’ equity), private credit (lending to firms) as well as real estate and infrastructure (investing in real estate and infrastructure assets).

Private equity entities represent the largest part of private markets and include three main investment types:

- Venture Capital funds (VC): investing in small firms in the growth phase, filling their need for liquidity, especially when they have limited bank credit access. It generally aims to hold minority equity stakes in those young firms.

- Leverages Buyout funds (LBOs): funding more mature firms with an investment horizon of up to 10 years which may be extended and aims to acquire controlling stakes in those entities. It thus includes larger investments than for VC due to the bigger size of the financed entities.

- Growth funds: stand halfway between VC and LBOs to fulfil the need for higher investments for small firms in the growth phase, such as unicorns (start-ups valued over $1bn), but still taking a minority stake in the company.

The graph below shows the aggregated assets under management (AUM) of each of the three private equity segments as well as for the rest of the sector at the end of 2022. The majority of the funds are situated in North America, with the exception of venture capital concentration in Asia.

North America holds the highest AUM in the private markets sector

Private equity funds have grown significantly over the last few years to reach 65% of private finance’s AUM. This increase was mainly driven by investors’ search for higher returns (especially during the low-interest rate period) as well as companies’ need for faster and more flexible funding.

The growth in venture capital at the global level is particularly significant, with an 8pp increase between 2019 and 2022. On an aggregate level, there has been a 10pp decrease in LBOs globally, despite a 2pp rise in Europe between 2019 and 2022, followed by a decline in 2023. Although less pronounced, there has also been a notable decrease in growth funds and venture capital. Overall, the decline in the three main private investment types over the past two years has returned them to pre-Covid levels.

European private equity investments declined in 2023

Despite lower investments, data from the ECB shows continuous growth in total assets held by private equities in Europe. The sector reached historically high levels of more than €700bn in total assets in the second quarter of this year.

European private equity total assets have still grown since 2015 reaching €700bn

One reason for the continuous growth of European private equity is the rising valuation of the sector’s assets. This leads us to the sector’s vulnerabilities, which we will discuss in the section below.

Private markets face five vulnerabilities

In our previous piece, we identified three vulnerabilities the broad NBFI sector faces. We estimated those risks as the largest known unknowns for the financial sector. With the recent public interest in private markets, this section will focus on the NBFI sub-sector and identify associated vulnerabilities.

As previously mentioned, private markets’ significant growth over the last decade can be explained by three factors: the development and increased regulatory burden on the banking sector making some parts of the economy less attractive for the sector. The second factor is investors’ search for higher returns during the extended low interest rate period. And last but not least, the sector has developed due to entities’ need for a faster and more flexible source of funding. Overall, private markets play a crucial role in the economy by providing funding to smaller, riskier and innovative firms. This is especially true when it comes to innovation for the green and digital transformation.

That being said, like any other NBFI, the sector is prone to several vulnerabilities: financial leverage, high interconnectedness, liquidity risk, valuation risks and procyclicality. In this section, we dive into each one of these risks before turning to the impact on the banking sector.

Overview of private market vulnerabilities

1. Financial leverage

Although the IMF classifies financial leverage in private markets as low, we consider it medium due to significant data gaps, particularly regarding entities’ use of complex financial leverage. The lack of reliable data makes it challenging to accurately assess the sector’s true exposure. Additionally, the use of complex financial leverage complicates the quantification of these risks.

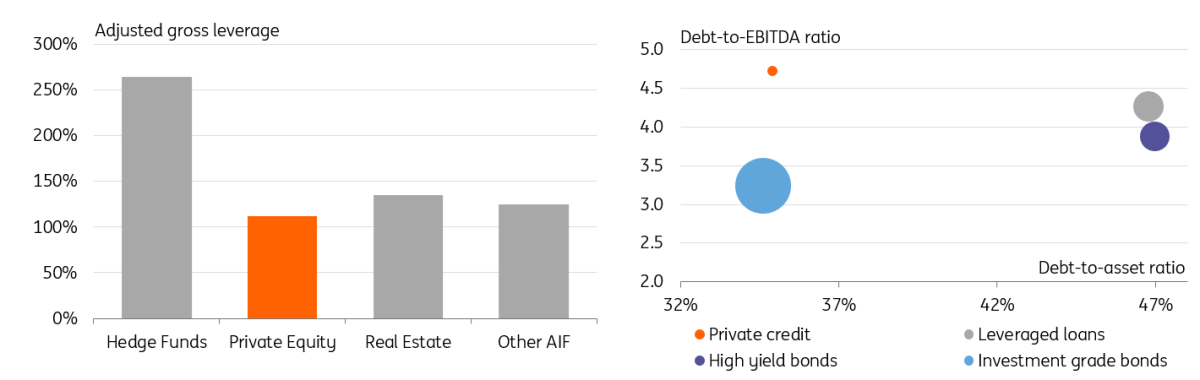

That being said, available data shows that private equities have lower gross leverage than real estate funds and other investment funds. Nonetheless, it remains a point of attention as recent data from the IMF points out that the private credit sector is prone to higher debt relative to earnings while being smaller than high-yield or leveraged bonds.

Private markets show lower gross leverage but more debt to earnings

Private equity gross leverage remains lower than for other IFs while private credit entities carry more debt relative to their earnings.

2. Interconnectedness

As discussed in our previous piece, NBFI's interconnectedness has grown significantly over the last decade. It implies ties both within the sector and also with the rest of the financial market such as banks. Private markets don’t deviate from the general trend. Indeed, interconnections appear on several levels for the sector.

Firstly, we note the growing links between private credit and private equity. While these two entities used to be well-defined and act separately, this dividing line is getting blurred. For example, the IMF reports that 82% of private credit assets under management are now handled by firms also active in private equity funds. This number drops to a little over 40% when looking at the number of credit funds under management. However, it exemplifies how intertwined private markets have become.

Over 80% of private credit assets are managed by entities also active in private equity funds

Secondly, interconnections between private markets and other NBFIs have increased. For instance, we note the prominence of ICPF investments in both private equity and credit sectors. These represent a little over 40% in private credit and 20% in the private equities sector. The second largest investments stem from OFIs (at 20% and 40% respectively).

The graph below also points out the relatively small share of banks’ direct investment in the sector, representing less than 10%, but we will come back to that in the next section.

Split of investors in private credit and equity indicates large NBFI contributions

More importantly, the investment flow stemming from ICPFs has grown sixfold over the last eight years reaching over 3.5% of total investment in the private credit sector. The main reason for this is the sector’s search for higher returns during the low-interest rate period.

ICPF investment in private credit funds has grown sixfold to reach over $600bn globally

Last but not least, the direct link between banks and the broader NBFI sector has increased in recent years. As illustrated in the graphs below, the share of NBFI’s total assets funded by banks, as well as their exposure to banks, increased between 2021 and 2022. Banks now fund just under 5% of OFIs’ assets globally and slightly over 1% of ICPFs’ assets.

Increased interconnectedness with banks relative to NBFIs assets globally

The growing links between the banking sector and NBFIs, in addition to the significant interconnection within NBFIs, exacerbates vulnerabilities. Indeed, interconnectedness implies greater spillover risks. It also indicates that the less regulated part of the financial system is growing in complexity, which complicates the potential development and implementation of both regulation and safeguards.

3. Liquidity risks

One very well-known NBFI vulnerability is its exposure to liquidity risk. Although private markets typically target illiquid assets, this sector is relatively sheltered from liquidity risks because most funds are closed-ended, preventing early redemption and limiting run risks. However, it’s important to note that nearly 40% of European private credit entities are open-ended, allowing for early redemptions.

A large majority of European private funds remain closed-ended

Despite that, liquidity risks remain contained even when looking specifically at the open-ended section of both private equity and credit funds. Indeed, most open-ended funds allow only infrequent redemptions from their investors, with 60% of private equity funds allowing for quarterly and longer redemptions while this represents a little over 40% of private credit funds. Consequently, the risk of sudden liquidity withdrawal from both types of funds is limited.

Within European open-ended private funds, the large majority restrict frequent redemptions

Nonetheless, over the past few years, private markets have increasingly attracted retail investors. To do this, they have developed new fund types of which a larger share is open-ended and allows for frequent redemptions. While we consider liquidity risks low, the development of retail investors and the consequent increase in open-ended funds might trigger growing liquidity risks.

4. Valuation risks

In contrast to the public market, supervisory oversight surrounding asset valuation and pricing is not as overarching for private markets. This adds to the inherent opacity of the sector and complicates the assessment of potential losses for external investors.

A report from the French Market Supervision Organisation points out that in addition to being infrequent, private market valuations suffer from three other vulnerabilities. Firstly, due to the nature of the projects funded, assessments often lack comparison potential. Secondly, the assets linked to the valuation are frequently intangible or linked to innovation making it difficult to estimate the liquidity premium. Finally, the sector’s development also increased its complexity which makes valuation more difficult. Consequently, models used to derive private assets’ valuation inherently contain a large part of subjective assumptions.

The difficulty of deriving a realistic assessment of private funds’ underlying assets and the large place for assumptions in the models used adds to the infrequent reassessment of those valuations. All these variables make the sector prone to hiding potential losses and underlying volatility. The IMF estimates that in a downside scenario, the lack of transparency and adequate data could result in a deferred loss realisation for the sector. This could lead to a spike in defaults and a confidence loss in the assets.

5. Procyclicality

Private markets also suffer from procyclical features. While the sector’s exponential growth stems from the low interest rate period and investors' search for yields, the extended period of higher interest rates may expose the sector to higher risks.

The higher for longer interest rate environment, in addition to inflation, exposes the private sector’s vulnerability on two sides. On the one hand, financed companies might suffer from inflation with higher costs and lower revenues. On the other hand, private finance funds might see their financing costs increase and, in some cases, struggle to refinance debt issued, even if we see this as a lower risk.

Next year’s economic forecast points to sluggish growth despite some additional interest rate cuts. Higher interest rates for an extended period accompanied by slow economic growth could hit the sector and result in higher default rates. This circles us back to the importance of accurate valuations.

Private markets but not so private vulnerabilities

We have now identified five vulnerabilities that private markets face. However, one question remains: how does this affect banks? To answer this, we will examine the effects in two sections: direct impacts and indirect impacts.

Direct impact

As shown in the section above, banks only represent a limited part of the interconnectedness private markets have with the rest of the financial sector. In fact, credit institution investment in private credit represents less than 10% of their total funds and this number drops to about 4% for private equities. A shock on the sector would therefore have only a very limited direct impact on banks.

However, the heavy development of the sector over the last decade and especially its appetite for larger deals implies an important new source of competition for the banking sector. Some institutions point out that the growing competition could trigger a race to the bottom in deal quality. Some underline the risks of a deterioration in underwriting standards as well as weaker covenants. Nonetheless, we view these direct risks as limited simply due to the already low underwritings and covenants quality.

Indirect impact

Despite viewing direct impacts on banks as limited, it doesn’t mean credit institutions would not suffer from stress in the sector. Indirect impacts are, in our view, of bigger concern and could be of a larger magnitude than direct ones.

While banks have limited direct exposure to private markets, they have a significant one in other parts of the NBFI sector. While we note that banks’ exposure to the NBFI sector has stagnated as a whole over 2022, it still represents up to 22% of banks’ claims and 20% of their liabilities globally.

Banks’ claims and liabilities to the NBFI sector over time

We have established the increased connectivity between private markets and the rest of NBFIs, especially pension funds and insurance companies, and it is clear how indirectly the banking sector is connected. Stress on the private sector could spill over to the rest of the NBFI sector and ultimately also to banks.

As discussed in the liquidity section of this piece, we also note retail investors’ increasing interest in private markets. Besides being generally less informed of the risks related to private investments and potential individual losses, the increased share of retail investors could amplify the impact of stress in the sector. Indeed, retail investors, aside from very high-wealth individuals, could pass on their losses from the private market to the real economy by lowering consumption. In the medium term, that could also translate into an increase in default rate and ultimately affect banks.

Due to the fundamental role private markets play in the economy, through financing small entities and startups, especially in the sustainable and innovation sector, stress would also hit the real economy with a spike in defaults and higher credit costs. Such a downturn could, in turn, affect banks’ credit quality.

All risks listed above are based on the assumption that the stress originated from the private sector. However, a shock in the banking sector as we witnessed in early 2023 could quickly spill over to the real economy via the interconnectedness of banks to NBFIs including private markets. Considering the important role played by private equity and credits to innovative firms, a shock transmitted to private markets would enhance the pain to the real economy.

Conclusion

To conclude this piece, we would like to open the discussion to future expectations. While private markets proved resilient during the banking stress episode of early 2023 as well as through the higher interest rates period, we believe financial sector participants should keep an eye on two points in 2025.

The first point concerns the sector’s procyclicality. As mentioned previously, private markets are prone to pro-cyclical behaviours. However, its recent development has made it an inherent and crucial part of the financial system and real economy. While the sector developed over the extended period of low interest rates by offering investors higher yields, the extended period of higher interest rates will test the private market’s ability to counter the increasing competition. We therefore expect to see more performance variation among private market participants.

As economists’ consensus points to another year of sluggish growth despite pencilling in several additional rate cuts, 2025 will test the private market's strength against credit risks.

The second point to keep an eye on is the development of the sector, especially when it comes to its share of retail investors. While the sector is expected to find new ways to develop and counter the competition increase linked to higher interest rates, the subsequent increase in retail investment could switch liquidity risks from low/medium to medium. In addition, a structural change of the sector towards more open-ended funds would increase liquidity mismatches.

While major financial market regulators such as the Bank of England and the Federal Reserve are still battling over the enforcement of the Basel requirements, the development of regulation targeting NBFIs is lagging.

The lack of data especially when it comes to the sector’s financial leverage and interconnection is the main challenge to adequate regulatory oversight. Considering the inherent international characteristics of the NBFI sector and more specifically private markets, international cooperation will be crucial in the coming years to enhance transparency and improve data collection and sharing.

Overall, the rise of private markets could come with hefty and not-so-private consequences. Therefore, the monitoring and development of data-gathering solutions to enhance the understanding of the sector’s vulnerabilities is essential to ensure the financial market’s stability.

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. Read more

Tags

BanksDownload

Download article

13 November 2024

Bank Outlook 2025: Clearing the fog – bank risks and market shifts This bundle contains 6 Articles