Japanese investors turn cautious on sovereign bonds ahead of global quantitative tightening

- 9 February 2022

- Rates

Much has been said of the support foreign buyers offered to developed sovereign bond markets in the era of ‘global quantitative easing (QE)’. Even before this era turns from global QE to global quantitative tightening (QT) sometime in 2022, Japanese investors have adopted a more cautious stance on foreign sovereign bond markets

Japanese investors see the writing on the wall

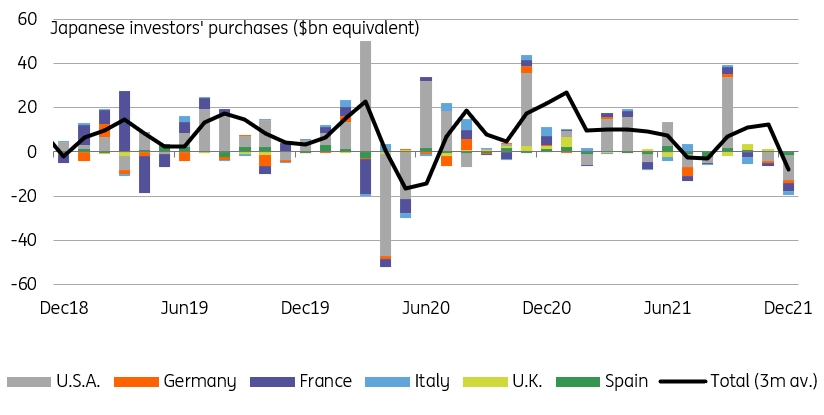

In December 2021, the Japanese ministry of finance reported that domestic investors turned net sellers of foreign government securities by the largest amount since the height of the Covid-19 pandemic in May 2020. They turned net sellers of all of the six large bond markets we focus on here, for a total of US$22bn equivalent. Even with this reversal of appetite for foreign bonds, net buying amounted to US$48bn in 2021, but this was a step down from US$114bn in 2020, and US$104bn in 2019.

December saw indiscriminate selling of sovereign bonds

This is far from enough evidence to declare the end of Japanese investors buying foreign bonds. And yet, this gradual decline comes at a challenging time for government bonds. It isn't much of a leap to assume that investors, seeing the Fed rush to end its own purchases of US Treasuries, also thought it an opportune time to reduce their exposure.

From global QE to global QT

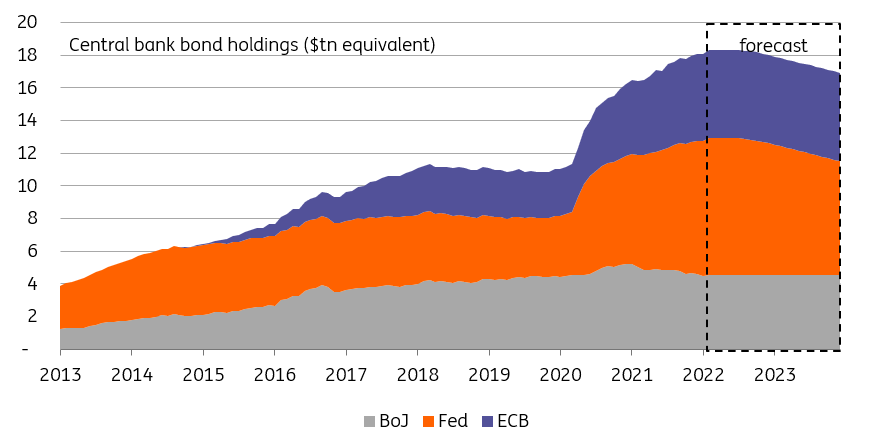

Bear in mind this data relates to December 2021. Since then, the Federal Reserve has turned more hawkish, and said in no uncertain terms that it intends to start reducing its bond portfolio (QT) in 2022, a troubling thought for any group of investors having accumulated foreign bonds in the hundreds of billions over the years. And what to say of the European Central Bank (ECB) hinting last week that it might cut short its own bond-buying programme in the face of higher inflation?

The Fed reducing it balance sheet heralds the start of global QT

Only time will tell if this thesis proves correct, but global investor flows deserve even greater attention than usual. The Bank of Japan is further away from tightening policy than the Fed and the ECB, but it has also been reducing its purchases. Due to the combined effect of rising global yields, Japanese Government Bonds (JGBs) now offer more attractive returns to local investors. Combined with the risk of greater losses on bonds denominated in US dollar (USD) and euro (EUR), this could make JGBs an increasingly attractive alternative.

Five 25bp Fed hikes implies reduced FX-hedged demand for Treasuries as 2022 progresses

Japanese lifers usually disclose their portfolio allocation preferences around the end of the fiscal year (in March). This will be a good indicator of how much interest there is in foreign bonds going forward. As the Fed and other central banks raise rates, so will the foreign exchange (FX)-hedging cost for buyers based in other currencies. Our expectation of five 25bp Fed hikes implies reduced FX-hedged demand for Treasuries as 2022 progresses. Things are less pressing for euro sovereign bonds, but they risk being caught in a general reduction in Japanese investors exposure to foreign rates products.

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more