Japan: Riding their luck

- 30 November 2020

- Japan

A reasonable pandemic so far looks at risk of a sudden rise in infections, though longer-term growth prospects should be supported by the recent pledge to shift the economy to net-zero greenhouse gas emissions by 2050. The near term outlook, however, is unpredictable and will almost be driven by the pandemic. Japan has been lucky twice, but a third time?

The Japanese economy has not had a particularly bad pandemic, despite limited measures undertaken to prevent the spread of infection. Helped by some very generous fiscal stimulus, Japan's recovery should be no slower than most other G-7 peers. But despite (and perhaps because of) decades of failed stimulus policies, the biggest boost to Japan’s economy might come from its new pledge to be a net-zero carbon emitter by 2050.

Though this will be hugely disruptive, it will require tens if not hundreds of trillions of yen to achieve and could provide an engine of growth for years to come.

Is Japan's luck about to run out?

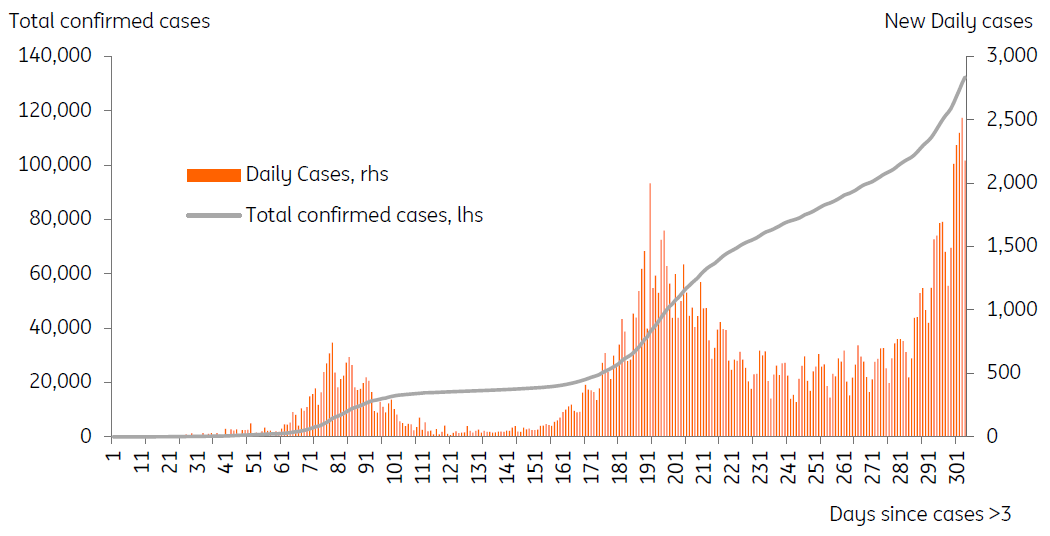

Admittedly, the current numbers don’t look very encouraging, but so far Japan has been extremely lucky during this pandemic.

With a large volume of passenger traffic between Japan and China in the early stages of the outbreak, Japan could easily have seen a much higher rate of infection back in March and April this year. Instead, the maximum daily case rate back then did not rise much above 750.

Japan hasn't really been a role-model during this pandemic. It held back from widespread testing to avoid over-burdening the health system with people with only mild symptoms (which it would be legally obliged to treat), and also managed to avoid a national lockdown. The northern island of Hokkaido was quick to implement a regional national emergency on 28 February but lifted it less than three weeks later on 19 March.

Exactly why Japan had such early success with the virus is still a matter of much debate but whatever it was, Japan did experience a second wave which saw cases spiking to a daily high of 1998

That came just before a 3-day weekend during which people went out to celebrate the end of their confinement, and probably sowed the seeds of the next wave, which three weeks later, had reached a new peak before a new state of emergency for 7 prefectures was announced by former prime minister Shinzo Abe on April 7, and then expanded to the whole nation on 16 April.

Compared to what has been undertaken in Europe and some US states, Japan’s “states of emergency” lack teeth due to the extensive civil rights built into the constitution. Business closures and other restrictions are typically voluntary. Indeed, for full-time workers, the rate of home working has been estimated to have been as low as 15%.

With the April measures looking disappointing, our expectation at the time was that Japan would suffer a bad outbreak that would cause far more damage to the economy than has in fact been the case. Against our expectations, the national state of emergency did work, and cases dropped right back to low double digits through the summer.

Exactly why Japan had such early success with the virus is still a matter of much debate which we don’t have space for here. Whatever it was though, Japan experienced a second wave from July to early August which saw cases spiking up to a daily high of 1998 cases. There was no second state of emergency, but a heightened request of firms and individuals to limit social interaction.

Japan's pandemic

Again, these limited moves seemed to work, and case numbers dropped. But whatever aspect of this request was doing the most good, recently seems to have stopped being effective, and Japan is now facing heightened daily case numbers once more, with daily cases now back up to 2500 and rising sharply.

So while the numbers still look very favourable compared to the US and Europe, for one of Asia’s more northerly and seasonal countries, Japan will have to be lucky again to avoid a more negative Covid-19 scenario, and we should have now learned that it doesn’t take long to go from 2500 to 25,000 cases per day when Covid-19 gets started.

GDP Outlook

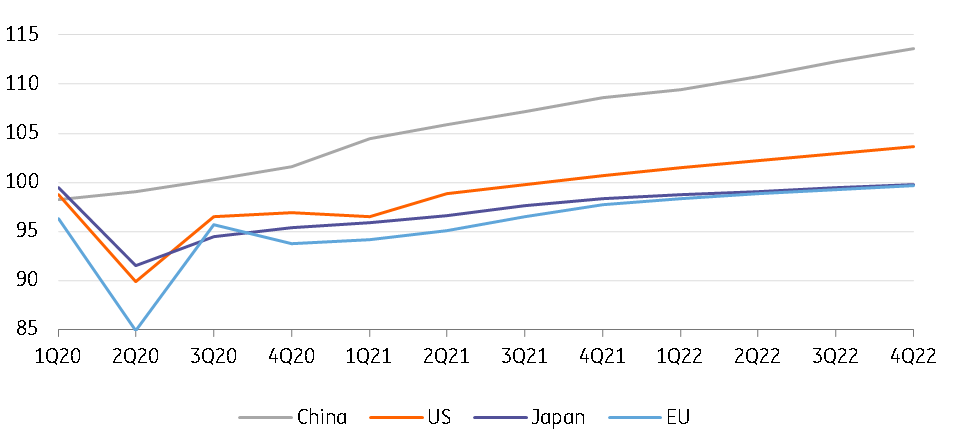

Our full-year forecast for 2020 is -5.4%. But let’s be clear, there is no merit in the decimal places here, and not even that much distinction between this and say -3% or -7%. The fact is, Covid-19 dealt a massive blow to Japan’s GDP, as it did everywhere else. The real question is, how well will Japan recover in 2021 and 2022?

Our full-year forecast for 2020 is -5.4%. But let’s be clear, there is no merit in the decimal places here

On the assumption that Japan avoids a bad second wave, which right now is looking optimistic, we see scope for growth to be faster than 2% in both 2021 and 2022.

Admittedly, this doesn’t bring Japanese GDP back to pre-Covid levels until the end of 2022, but that is no worse than most of its G-7 peers (a bit slower than the US).

GDP recovery in "levels" (4Q19 = 100) - ING forecasts from 4Q20 onwards

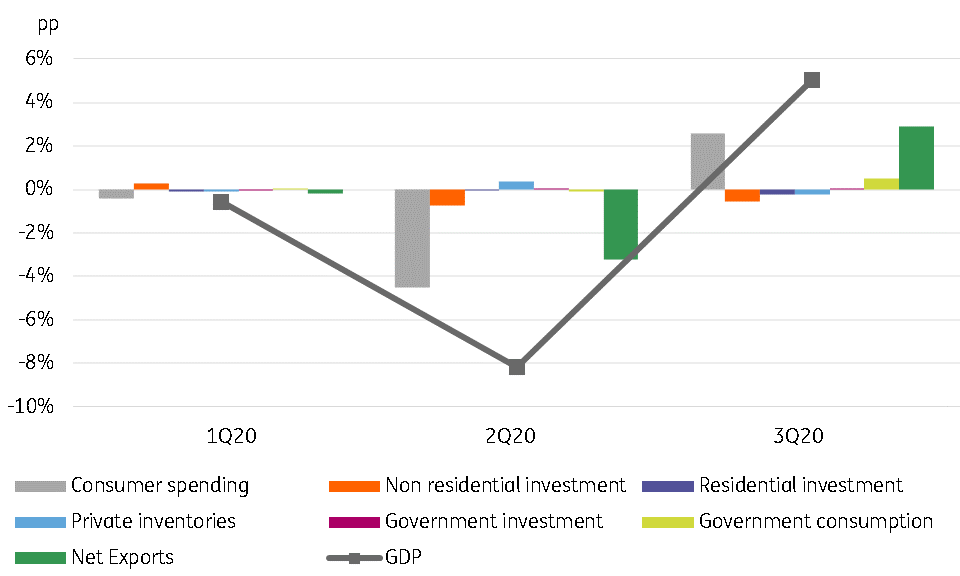

GDP growth in 3Q20 came in a little above consensus expectations, but following the 7.9% quarter-on-quarter contraction in 2Q20, a 5% bounce was roughly in line with the wild guesses from forecasters. There is not much “science” in forecasts when facing this degree of volatility.

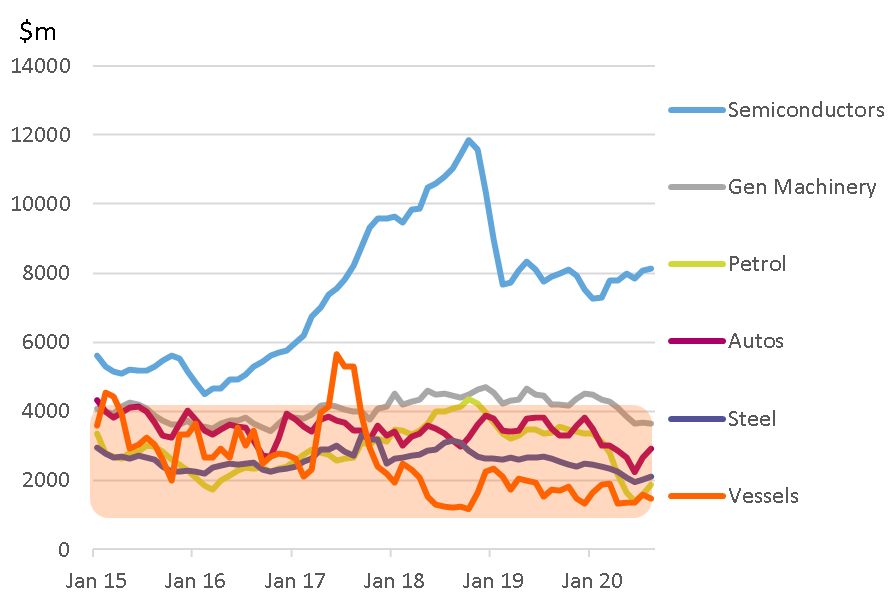

The vast bulk of the 3Q bounce came from net exports. Export growth in Japan in 3Q20 was up 7% year on year. That isn’t much, but it’s not bad compared to some other regional peers, and it does look as if Japan is benefitting from the semiconductor and technology upcycle that is driving some other parts of North Asia.

Looking at the breakdown of the contribution to export growth, electrical machinery tops the table, albeit with a relatively modest 0.3pp contribution. But nonetheless, it is a turnaround from the 0.4pp drag it exerted on total export growth at the end of 2019.

That electronics upcycle is a combination of China’s push for technological self-reliance, which in the short-term is lifting substitutes to US electronics to which it no longer has access, 5-G rollout, and the IT upgrades that are a part of the new normal way of working from home.

Even so, the big boost to the third-quarter came mainly from weak imports, not rising exports, and that isn’t indicative of either continued strong export growth, or a pick-up in domestic demand. It is very unlikely that we will see such a strong contribution from net exports in 4Q20, and we anticipate GDP growth slowing back to only 0.9% QoQ then.

GDP growth by expenditure component

Household spending provided the bulk of the remainder of 3Q20 growth in GDP, but there was very little contribution from business investment spending or residential construction.

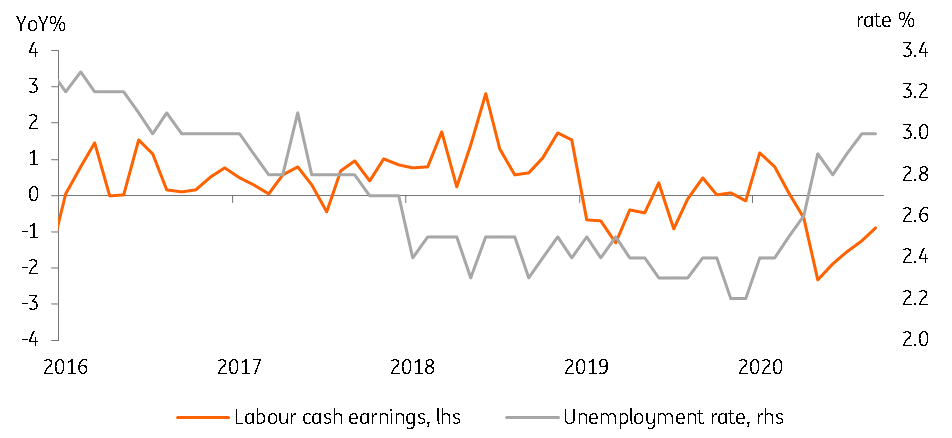

Consumer spending and labour cash earnings were supported during the national emergency by government policies, and are currently only 0.9% lower than a year ago and improving slowly. The unemployment rate in Japan remains at 3.0% - a four year high, but low in absolute terms (though probably masks a lot of underemployment).

Labour cash earnings and unemployment rate

Crystal ball-gazing

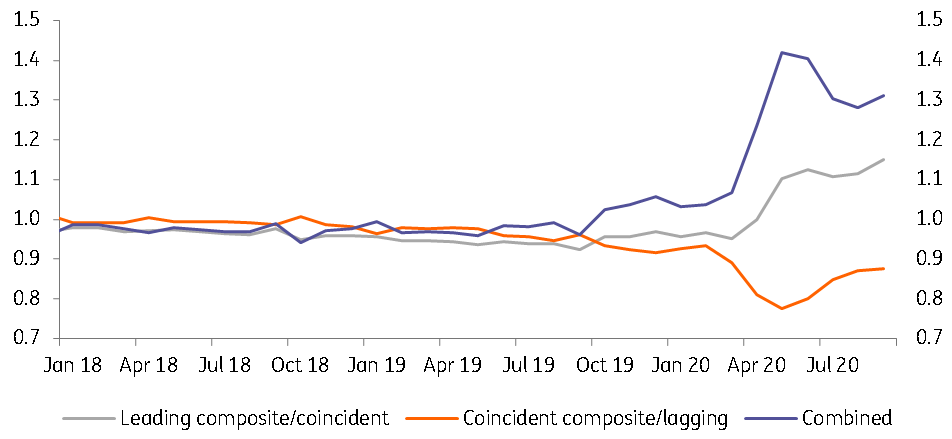

There isn’t much “lead” in the leading indicator for Japan. but one way to squeeze a little more juice out of this data is to consider the ratio of the leading to coincident indicators.

That’s a bit like looking at the second derivative of forward to coincident indicators. We can further create a combined index looking at the ratio of these two other series for a further squeeze of information. And when we do that, the data continues to point, perhaps unsurprisingly, to further recovery, but at a more moderate pace. The big bounce has happened.

What comes next will be more sedate – in line with our 0.9%QoQ GDP forecast in 4Q20.

Leading diffusion indices ratios

Inflation - nowhere to be found

The last time consumer price inflation in Japan was consistently above 2% for any other reason than a surge in global crude oil prices, or the temporary effects of consumption tax hikes, was back in the early 1990s, almost 30 years ago.

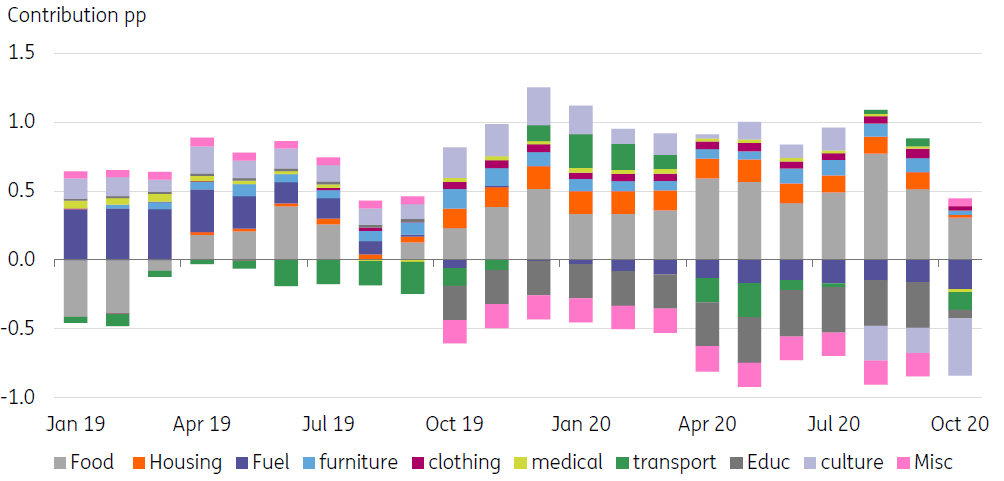

So the fact that inflation still languishes close to zero than to the target rate of 2% comes as no surprise, and this is not particularly alarming during this unprecedented global economic slowdown. Since 1995, Japanese headline inflation has averaged just 0.2%, and in September, the inflation rate was exactly zero.

Contribution to inflation (percentage points)

This feeble inflation outcome arises despite a succession of fiscal stimulus plans over recent decades offering to “kickstart the economy”, and “boost inflation”, in the process, taking the debt-to-GDP ratio to over 250% for no discernible long-run impact on growth or inflation. It also comes against the backdrop of the longest spell of negative interest rates and quantitative easing in the world. It is safe to say, that if the growth and inflation “problem” in Japan had anything to do with the monetary stance, this should now have been fixed. It clearly isn’t.

If the growth and inflation “problem” in Japan had anything to do with the monetary stance, this should now have been fixed. It clearly isn’t.

Inflation will continue to fluctuate between zero or slightly negative rates and about 1%. Some of the recent drag on inflation is due to cuts of administered prices such as childcare and early years education. That was part of last year’s consumption tax offset and should revert to roughly a zero impact by the end of the year. Food is the main contributor to inflation each year and is typically the effect of a combination of currency shifts (weaker yen makes imported food more expensive) and weather-induced spikes and troughs.

Strip out food, and core inflation is much lower (ex-food inflation, and ex-food and energy inflation were both -0.3% in September). This isn’t going to change.

Monetary policy response - there hasn't really been one

This pandemic has been interesting in confirming what we have long suspected, the impotence of the Bank of Japan to provide any meaningful policy support.

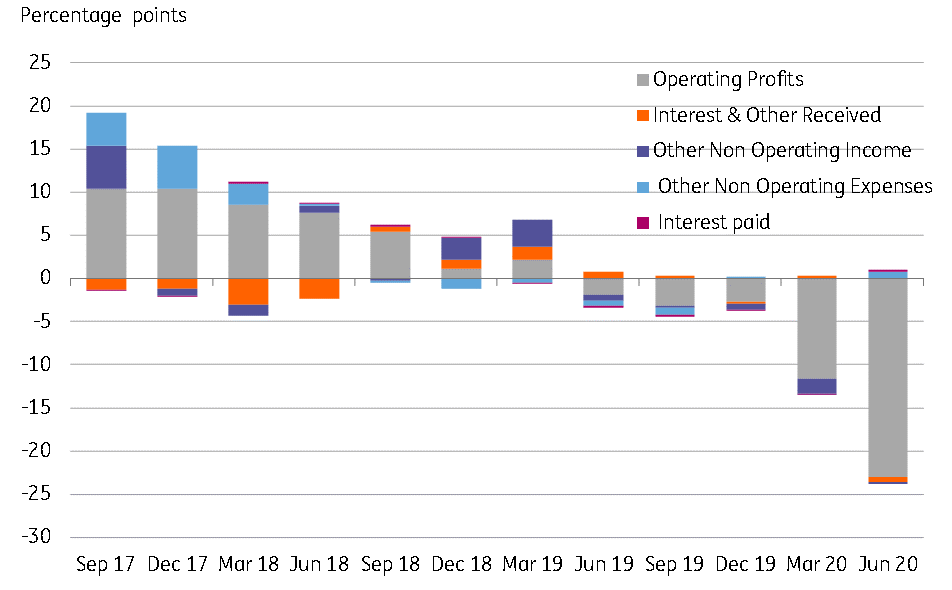

A chart of Japan’s business profits shows neither interest paid or received playing much of any role in the profit cycle. It’s the real economy that matters and operating profits.

The origin of profits - it's not from monetary policy

The central bank’s policy stance remains more or less the same as it started the year.

The BoJ’s policy interest rate target remains -0.1% and the 10-year Japanese government bond (JGB) target remains at zero, and there have been no official changes to the targeted purchase amounts of JGBs, REITS or anything else. Having said that, the BoJ has stepped up the actual pace of its asset purchases, as is demonstrated by the growth in base money (assets are purchased with “created” cash, which is then returned by asset sellers to the liability side of the current account of the BoJ as deposits).

Exactly what purpose this accelerated asset purchasing is aiming to achieve isn’t clear, but it could be an attempt to keep JGB yields closer to zero after a period where they had turned modestly positive.

Rather than monetary policy, the BoJ’s main policy drive currently seems to be to create more stability in the banking sector

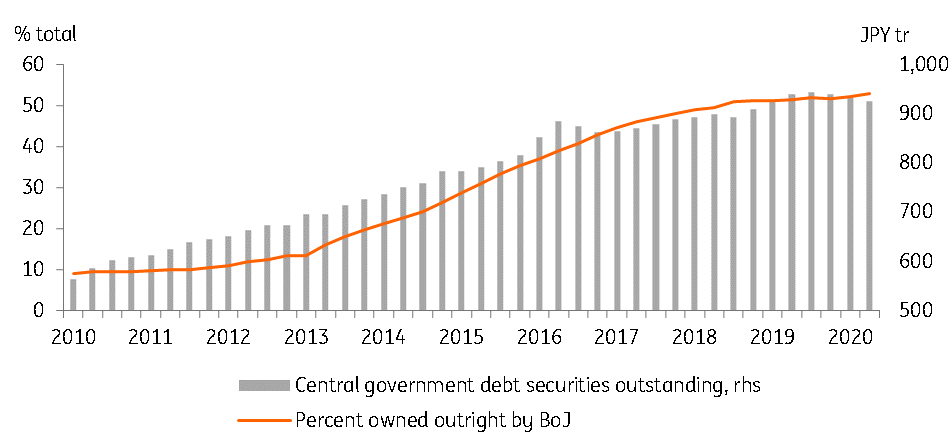

The Bank of Japan now outright owns more than 50% of the stock of central government debt. On the plus side, the government’s aggressive fiscal stimulus plans mean that there should be plenty of JGBs to go round over the coming years, and the fact that 10-year JGB yields remain fairly steady at just over 0.01% suggests that this isn’t causing any problems. Like everything else in this pandemic, new rules are being made as well as old ones being broken.

Rather than monetary policy, the BoJ’s main policy drive currently seems to be to create more stability in the banking sector. The main push seems to be to encourage a consolidation of banks in much the same way as they did with the “convoy system” approach to banking following the asset bubble collapse of the 1990s. With bank margins very thin, some reduction in bank fixed costs may not be a bad idea, but it is not ground-breaking, and we don’t think it will have more than a marginal impact.

BoJ Japanese government bond ownership

Bank lending is not the problem

The weakness we noted in business investment is not evident from examining bank lending figures, which shot up in growth terms due to Covid-19 support measures. This, however, is mainly driven by emergency cash-flow support. A clearer picture will emerge when October machine orders are released on 12 December.

Tankan measures of lending conditions show a modest tightening for large and medium-sized firms. But smaller companies show fewer signs of a lending squeeze - a sign that the BoJ’s numerous Covid-liquidity response measures are working. Lending conditions are considerably better than they were during the global financial crisis, for example.

Despite no particular shift in policy stance, we expect some further JPY strength this year. This, we feel, is more a function of the unwinding of previous USD strength – partly resulting from the US-China trade war. We anticipate the USD/JPY rate reaching 100 by the end of 2021.

Fiscal policy - lots of it

Where other countries have responded to the end of conventional monetary policy by shifting the burden of support to fiscal policy, Japan never had any monetary policy room to manoeuvre to start with and had to resort almost entirely to fiscal support.

The current Covid-19 support measures have been claimed to have a 40% GDP equivalence. But this includes a lot of double-counting of pre-existing measures, plus allocations for soft loans that in many cases will never be disbursed. Our rough guess though, of how much “genuine” or “on-budget” money has been committed to support economic recovery is of the order of about 12% of GDP, which is still a very substantial amount.

Japan’s budget deficit for the calendar year (CY) 2020 is officially estimated at 11.4% of GDP by Japan’s ministry of finance, and Covid-19 has taken the government debt ratio to 251.9%. Japan has clearly taken the view that when the public debt is so large, there is little point worrying about an extra 10% or so of government debt. They have a point, and while interest rates on that debt remain substantially less than nominal GDP growth, this remains a sustainable position.

Our rough guess though, of how much “genuine” or “on-budget” money has been committed to support economic recovery is of the order of about 12% of GDP, which is still a very substantial amount

The chart below shows the yield on newly issued 10-year Japanese government bonds versus the nominal GDP growth rate. Ideally, we would show this as the average yield on outstanding debt. But the longer JGB yields remain at approximately zero, the less important this distinction becomes. Moreover, at a zero yield, it doesn’t really matter how large the debt or deficit is – there is no debt service cost. Indeed, Japan’s problem is not its debt stock or deficit, it is what happens if it ever manages to achieve its inflation targets, growth recovers, and bond yields rise. At that point, the debt arithmetic could become tricky very quickly.

There is no indication of what the 2021 budget will look like. But we anticipate that the deficit will remain substantial since an abrupt cut in public spending could generate its own technical recession. Consequently, government spending is only likely to decrease by the extent that GDP recovers and may well err on the side of generosity, meaning that the 2021 budget deficit will likely remain above 5%.

No debt service problems as long as BoJ fails to resurrect inflation

The "death" of Japan's labour force has been greatly exaggerated

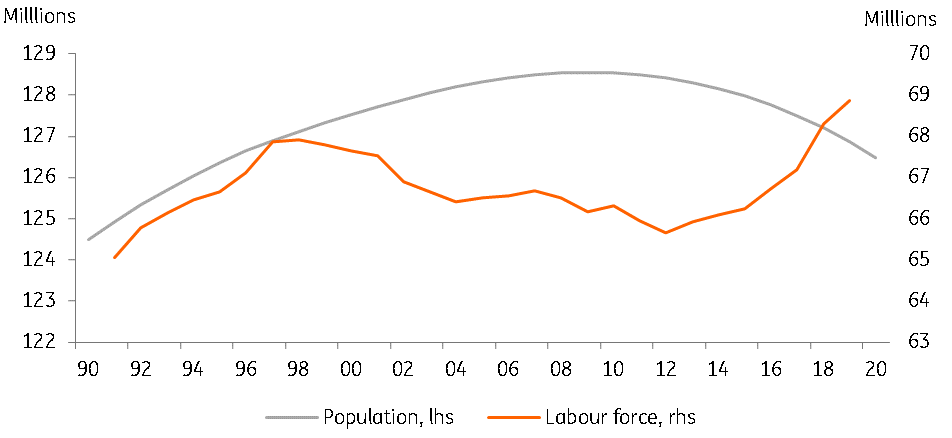

Japan’s ageing population has been a subject of economists' gloomy forecasts on Japan for decades, long before the population actually started to decrease, which it began to do after 2009 when the population peaked at 128.6m.

A growing age-dependency ratio has stressed Japan’s economy, but it has not ruined it. Instead, we have seen it respond to a falling ratio of prime-aged workers to the elderly in a number of ways.

The population of working age is not the same as the labour force, which the following chart demonstrates. Shortly after the population peak, Japan’s labour force began to grow. From its 2012 trough, it has grown by more than three million, even as the population total has shrunk by more than two million.

Japan's labour force and population

Two main reasons for the labour force increase

There two reasons for this labour force increase probably owe something to the structural reforms undertaken under former PM Abe.

The first and dominant change is the growth in female labour force participation. This has grown by about 2.5 million since 2010, mainly due to women previously reporting their main economic activity as homemakers. Factors enabling this to happen include measures to ease childcare burdens. But they may also be reflected in the second statistic, which is an increase in Japan’s foreign population.

At slightly more than 1% of the total, Japan has a very small foreign-born population, but it has grown by around one million to more than three million since 2010

At slightly more than 1% of the total, Japan has a very small foreign-born population, but it has grown by around one million to more than three million since 2010. Inhabitants of Chinese origin make up the bulk of the total, but the greatest growth in Japan’s foreign-born population in the last ten years has come from Vietnam, which has grown from almost nothing to more than 400,000 over this time frame, accompanied also by some growth in population from the Philippines.

Whilst there has been some criticism that Japan’s immigrant population doesn’t bring in high levels of skill, it may be enabling the local population to re-enter the workforce, by helping with home keeping and childcare. That’s not a bad outcome.

2020 Tokyo Olympics in 2021?

A decision on the “whether”, “when” and “how” to hold the postponed 2020 Tokyo Olympics will likely be taken in December. Assuming it is held next year, it is likely to be very different from previous games. Athletes will fly in and then quickly leave once their event is completed. There will be limited numbers of spectators.

Most of the GDP relevant expenditure surrounding the Olympic games has already taken place, in the form of the sporting infrastructure

We have not made any allowance for Olympics in our forecasts. We may not have to do anything. Olympics and other major sporting events such as World cup football and cricket tend to be more about shifting expenditure rather than boosting it. More holiday gets taken to enable spectators to attend events, and this can boost spending on related services and travel, but tends to come at the expense of regular expenditure and production.

Most of the GDP relevant expenditure surrounding the Olympic games has already taken place, in the form of the sporting infrastructure – stadiums, athletes villages etc. that have been constructed. That cost is officially logged at JPY 1.3tr ($12.6bn), though news reports refer to a government audit putting the amount at more than twice that. Even before the pandemic, the Japanese government had put in place measures to soften the blow to growth post-Olympics construction. That turned out not to be their biggest problem.

In 2021, any Olympics, regardless of the form are unlikely to be a big macroeconomic, or market-relevant event, though it may well be viewed as an important psychological milestone to the normalisation of the economy.

Japan's new green pledge - not just hot air

Although we saw virtually no “green’ content to Japan’s immediate Covid-19 fiscal response, it has recently joined South Korea and China in announcing a net-zero commitment. In Japan’s case, this is a commitment to net-zero greenhouse gas emissions by 2050.

Japan is a heavy emitter of green-house gases by global standards (2.7% of the global total), and it will have its work cut out to achieve this new goal. PM, Yoshihide Suga, has made some encouragingly refreshing remarks in which he notes that reaching this target will generate growth, not constrain it. That is probably correct, though this is not to say that achieving these goals will be easy or victim free.

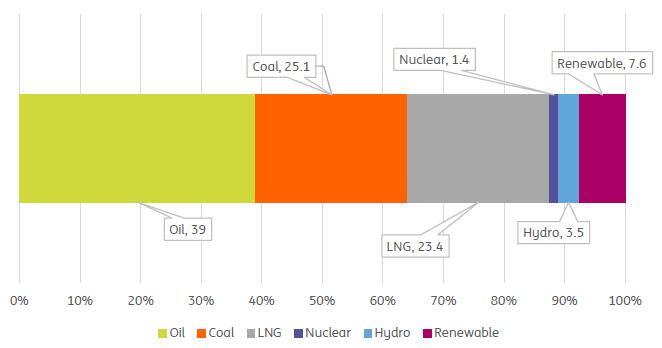

Japan is the world’s number five greenhouse gas emitter, thanks to a heavy reliance on fossil fuels for electricity generation. Coal, oil and natural gas accounted for nearly 90% of Japan’s primary fuel scources as recently as 2017.

Primary energy mix Japan (2017)

Replacing a large proportion of Japan's electricity generation with renewables is harder for Japan then comparable developed economies due to its geographical quirks (largely mountains and forests), and offshore wind is also tricky because of typhoons and tsunamis. Nuclear energy will inevitably be a part of the decarbonising solution, though that brings other concerns that Japan knows only too well.

And even if electricity production is totally decarbonised, that leaves the remainder of primary fuel consumption (75%) to adjust (vehicles, industrial, residential). This will not be easy and it will be expensive.

Replacing a large proportion of Japan's electricity generation with renewables is harder for Japan then comparable developed economies due to its geographical quirks

But there is some low-hanging fruit. For one of the world’s largest vehicle producers, Japan’s e-vehicle fleet is tiny (3% according to the IEA, other sources have it as low as 1%). Investment in charging stations seems an obvious first step, steep tax increases on petroleum and diesel, priority lanes for e-vehicles, parking reductions, tax offsets. This might be an effort, but it isn't technically hard and has been done very successfully elsewhere (e.g. Norway)

A radical overhaul of carbon pricing will also be a clear requirement to encourage industry to take the steps needed to transform and to enable the financial industry to support investment in projects supporting the energy transition. There are currently three carbon pricing measures in Japan, one national and two regional. These don’t appear to be up to the task of achieving decarbonisation, with the national carbon tax of $5/tCO2 one of the lowest in the world.

Despite one of the biggest financial industries in the world, Japan ranks 32nd behind Singapore in terms of the depth and quality of its green finance according to one 2020 study. There is clearly considerable market space in this area for incomers with long term space for considerable growth given the enormous sums that will have to be committed to achieving the 2050 pledge, and earlier milestones.

Longer-term outlook for Japan is actually not looking too bad

The near term economic outlook for Japan is unpredictable and will be almost totally driven by the evolution of the pandemic. It has already been lucky twice, but a third time?

Policy measures should set the scene for an eventual recovery, and this will clearly be aided by vaccine roll-out, whenever that comes. In the meantime, the huge amounts of fiscal stimulus money committed, whatever number you believe, provide the insurance that once the pandemic lifts, there will still be an economy left to recover. The Bank of Japan is of marginal relevance here, as has been the case for a long time.

The longer-term outlook for Japan is actually not looking too bad. The worst fears of economists about Japan's ageing population have not materialised, thanks to more female participation, and longer working lives for the elderly. And the new commitment to net-zero emissions could provide Japan with just the high return investment projects it has lacked since the overinvestment of the 1980s, so long as there is sufficient financing to support it.

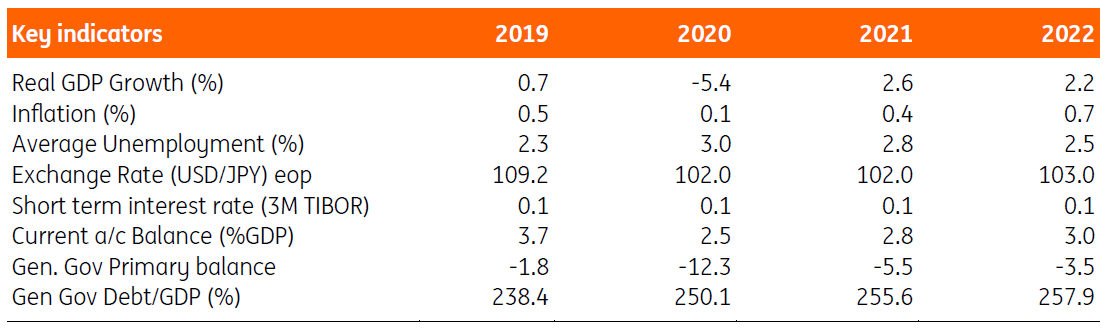

Forecast summary

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more

Included in the following bundle

Good MornING Asia - 1 December 2020

- This bundle contains 3 Articles