Japan: Ready to bounce back

- 30 November 2018

- Japan

Economic growth in Japan contracted in the third quarter, hit by extensive damage from typhoon Jebi. But the doors are now open for a fourth-quarter bounce back as the post-typhoon clean-up spurs economic activity

Jebi wreaks havoc on 3Q18 GDP figures

Typhoon Jebi made landfall over Shikoku and then the Kansai region of South Eastern Japan on 4 September, before tracking North West in the direction of Taiwan and Far East Russia. Jebi was estimated by one source as being the most powerful storm on the surface of the planet so far in 2018. It was the most intense tropical cyclone to hit Japan since Typhoon Yancy in 1993.

At peak intensity, Jebi was a Category 5 super Typhoon, with sustained wind speeds of 195km/h, and gusts of 280km/h.

Extensive capital losses and infrastructure damage caused a September slump

Damage from the typhoon was extensive. Flooding and winds wreaked havoc with infrastructure. Roads airports, bridges and ports were wrecked. Private residential property damage was extensive. Hundreds of cars were picked up and tossed to destruction by the winds. Not surprisingly, many businesses suffered capital losses, and many others were shut as staff were unable to reach them. Total insured losses for the economy have been estimated at between JPY340 and JPY620 billion (up to about 0.1% of GDP). But according to some estimates, uninsured agricultural damage may have been up to ten times as large, with other uninsured losses probably of a similar magnitude.

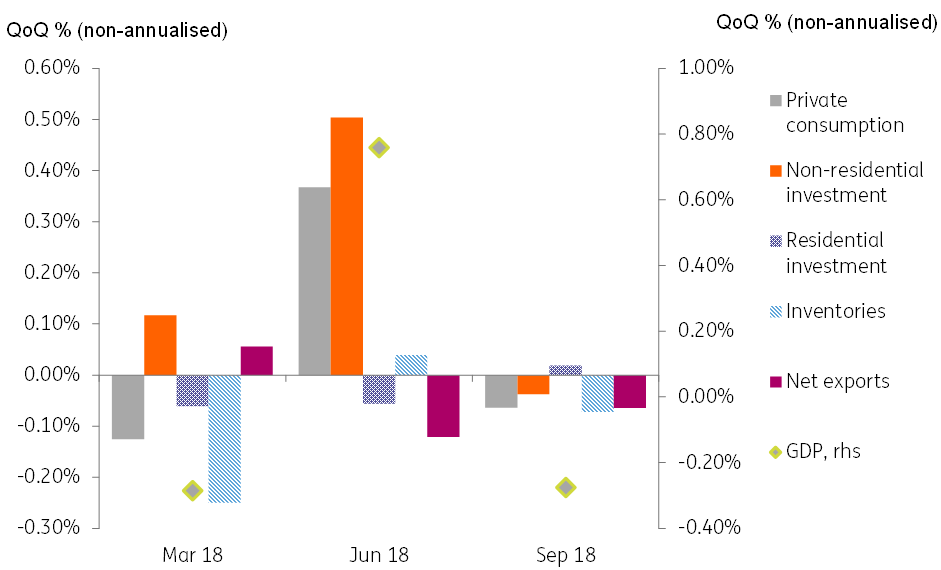

GDP contracted 0.3% QoQ in 3Q18

Our forecasts for third quarter GDP prior to Jebi had been quite strong, at about 2.2% (quarter-on-quarter annualised). Initial indications were that the economy had weathered the Typhoon well. But data released just prior to the GDP figures showed this was not the case. Private household spending dropped very sharply. Business investment was also badly hit, as were exports (though so too were imports). Nonetheless, we still thought there would be some offset in terms of an unintended inventory build as activity that should have happened didn’t. The official GDP figures released suggested oddly that this did not happen – possibly inventories were damaged / lost in the Typhoon. The net result was a 0.3% quarterly GDP contraction or -1.1% QoQ in seasonally adjusted annualised terms.

But Japan will bounce back, with stronger growth in 4Q18 and 1Q19…

The common pattern with a natural disaster hitting an economy is real time economic disruption, followed in subsequent quarters by a bounce back, as clean-up spurs activity that would not ordinarily have happened, bolstered also by replacement of damaged capital and infrastructure. The net result on GDP is often (though not always, depending on the extent of infrastructure damage) positive. We imagine that this will be the case this time round too, and have nudged up our 4Q18 and 1Q19 GDP estimates, in response providing a little lift to the 2019 annual growth estimate, which now stands at a healthy 1.7%.

GDP gets wrecked by Typhoon Jebi

Inflation spikes should also be limited by oil price declines

Near-term inflation in Japan could also be affected, in particular, agricultural damage should push up headline inflation rates as fresh food prices in Japan and across the Asia region spike higher. But against this, we also have to factor in the much sharper falls in oil prices that have coincided with this event, and which will mitigate against some of this food price increase. In the very short-term, this may limit the quarterly impact on headline inflation rates. And core rates are likely to remain subdued at close to their current 0.4% year-on-year rate.

The BoJ will find it harder to make any near-term progress towards a taper

None of the above makes it easier for the Bank of Japan to further its attempt to follow the ECB and begin a taper of its own with respect to asset purchasing and bond yield targeting. 10Y JGB yields are back smack on their 0.1% target, and there is no sense that further taper progress is possible near-term. This is not helped, of course, by the macro and political difficulties being faced in the eurozone right now, which limit progress that can be made there, and which therefore deprives the BoJ of a screen for its own intentions.

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more

Included in the following bundle

Good MornING Asia - 3 December 2018

- This bundle contains 4 Articles