The Italian economy looks set to stagnate over the winter

- 3 November 2023

- Italy

Softening growth and rising debt servicing costs are re-awakening debt sustainability concerns, which call for a swift return to primary surpluses. How big these will have to be will also depend on whether the government will manage to effectively implement the Recovery and Resilience Plan

Italian GDP stagnated in the third quarter as monetary tightening finally bites

The Italian economy is no exception. After a relatively quick post-Covid rebound, accommodated by the coexistence of expansionary monetary and fiscal policies, the economy has been cooling down since the second quarter of 2023, mainly on the back of softening domestic demand. After contracting by 0.6% quarter-on-quarter in the second quarter, Italian GDP was flat in the third – just about avoiding a technical recession.

With a notable delay since the start of the tightening cycle, the cumulated effect of past interest rate hikes has finally started showing up in credit data. In August, loans to non-financial corporations contracted by 7.9% year-on-year and loans to households for house purchases just expanded by 0.6% YoY. According to the latest Bank of Italy bank lending survey, loan demand is also expected to remain weak over the fourth quarter.

Not the best environment for investments; consumption looking better

High interest rates, credit contraction and an increasingly uncertain geopolitical backdrop are a bad mix for investments. The ongoing phasing-out of very generous tax incentives (the so-called “super bonus”) should continue to act as a drag on the residential sector in the fourth quarter of 2023, whilst the non-residential component could potentially benefit from the recent payment of the third tranche of the Recovery and Resilience Facility, worth some €18.5bn, partially compensating.

Consumption, which had been a key growth driver during the re-opening wave, is likely holding up better, helped by a resilient labour market. In August, revamped employment and falling unemployment brought the unemployment rate down to 7.3%, a level not seen since January 2009. Hiring intentions in recent business surveys continue to suggest that risks of a swift turnaround in employment remain low. Resilient employment and a progressive renewal of expired wage contracts at higher rates (hourly wage growth has stabilised at 3% YoY in the June-August period) should help support disposable income through the next winter, paving the way to a gradual recovery in consumption over 2024, and allowing for a gradual recovery of the savings ratio to pre-Covid levels (c.8%). Within the projected winter stagnation, private consumption should not be a drag on growth.

Disinflation should help, more likely in 2024

The prospective growth profile will also be affected by developments on the inflation front, at least in 2024. The October CPI release marked a sharp fall in headline inflation to 1.8% (from 5.3% in September), thanks to a favourable base effect on energy products. Even though a return above 2.0% through the winter seems inevitable, the disinflationary wave should resume over 2024, creating a better growth environment via an improvement in households’ purchasing power but also supporting a recovery in consumer confidence.

All in all, we expect the Italian economy to stagnate in the fourth quarter of this year and the first quarter of 2024, but see room for a gradual acceleration starting in the second quarter of next year. As 2023 will leave 2024 with a poor statistical carryover, it will be hard for average 2024 GDP growth to do better than 0.5% YoY.

Debt sustainability concerns re-awakened by a normalising environment…

Softer growth and the rising cost of debt are resurrecting debt sustainability concerns, given the sheer size of the Italian public debt. The recent widening in the BTP-Bund spread (now hovering just below the 200bp level in the 10y tenor) has accompanied the genesis of the draft budgetary plan (DBP) recently submitted by the Italian government to the EU Commission. To be clear, the DBP, while projecting a deficit decline delayed with respect to the original plan (deficit at 5.3% in 2023 and 4.3% in 2014), is not a disruptive one.

The profile of deficit data is being affected by the impact of the new accounting rules adopted by Eurostat for tax credits, which tend to penalise 2023 with respect to 2024 (when part of the incentives will be phased out). In this context, the 1.1% correction in the structural budget foreseen for 2024 in the DBP, at face value a substantial one, should be treated with some caution. The tax credit accounting factor also shows up in public debt dynamics with a small delay, i.e. when the tax credit is actually cashed in.

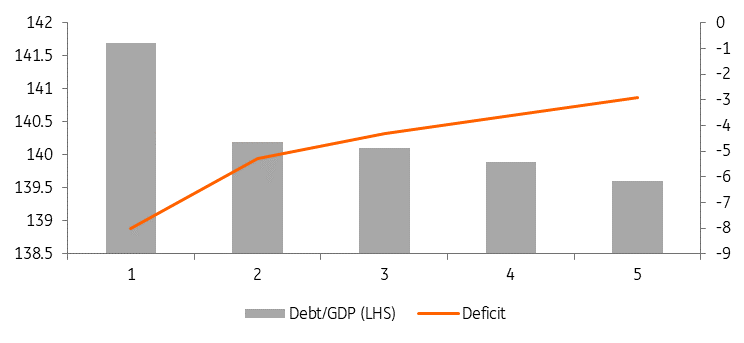

The combined effect of slow adjustment, accounting rules and slowing inflation translates into an unpleasantly flat debt profile in the DBP, with the debt/GDP ratio down a whisker from 140.2% in 2023 to 139.6% in 2026. A flat profile with upside risks attached, given the underlying assumptions of 1.2% GDP growth in 2024 and optimistic expectations of (undefined) privatisations worth 1% of GDP over the 2024-2026 time span.

The uncomfortable flat debt

GDP profile of Italy's Draft Budgetay Plan

Calls for a return to sustained primary surpluses of around 1.5% of GDP

Looking beyond 2026, when the bulk of the tax credit noise should disappear from public finance data, a declining debt dynamic will almost inevitably call for a sustained return to solid sustained primary surpluses. In fact, in 2025, the Italian debt/GDP ratio dynamic will likely cease benefitting from the current positive 'snowball effect' (i.e. a negative difference between the average cost of debt and nominal GDP growth) driven by the solid post-Covid economic rebound and by the inflation surprise accentuated by the war in Ukraine. As expiring debt is refinanced at higher interest rates and inflation cools down, the snowball effect looks set to turn negative, as it has historically been when low growth-normal inflation environments prevailed.

How big should primary surpluses be to secure debt stabilisation under reasonable macro assumptions? To find out, we ran a simulation with our base case growth and rates forecasts, which foresee a temporary acceleration in GDP growth towards the 1% level in 2025 and 2026 (the last two years of the implementation of the National Recovery and Resilience plan) and assuming a subsequent stabilisation of growth at 0.6% and inflation at 2%. What we get is that a primary surplus of c.1.5% of GDP would be required to stabilise the debt/GDP in a normalised interest rates environment. While seemingly ambitious, this is a level that Italy has been able to sustain for prolonged periods in the past.

Growth enhancing reforms and investments are key

As debt stabilisation would unlikely be deemed acceptable by any prospective fiscal rule (be it the old SGP or an amended version of the EU Commission proposal) a bigger effort would be required to secure a declining debt/GDP profile, the alternative being managing to sustainably increase the growth potential of the economy. The Italian government has a powerful tool to this end: the Recovery and Resilience Plan and its mix of reforms and investments. Its thorough implementation will likely become the single most important mission for the rest of the legislature, also for debt sustainability reasons.

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more

Included in the following bundle

ING Monthly: Too early for optimism

- This bundle contains 12 Articles