Hungary: Election uncertainty as net bond supply falls

- 26 February

- FX Hungary

Hungary faces elevated fiscal uncertainty ahead of the April elections as the deficit rises to 5.5% of GDP. Borrowing needs ease slightly, but record redemptions drive a sharp fall in net HGB issuance, with bonds regaining dominance and retail declining. For FX issuance, diversification remains the name of the game, with reliance on EU money

Fiscal policy: rising deficit and elevated risk ahead of April elections

In November, the government announced an increase in the public finance deficit to 5% of GDP in 2025 and 2026. Last year ended at 4.9%, and we expect this year to be at 5.5% of GDP. In cash terms, the deficit should end up similar to the government's estimate. However, given the general election in April and the unclear direction of fiscal policy afterwards, there is a greater degree of uncertainty than usual regarding fiscal and issuance plans.

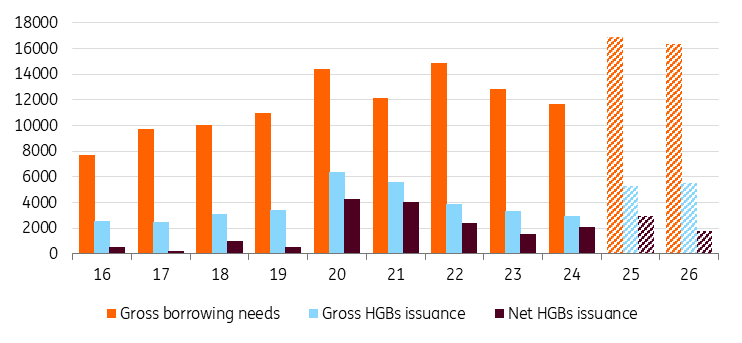

Gross financing needs and HGB issuance (HUFbn)

Local issuance: HGBs regain dominance as Hungary’s borrowing needs moderate

After the increase in budget targets at the end of last year, we saw a significant increase in gross borrowing needs and HGB issuance at the same time. Last year, gross needs probably reached new historical highs. This year should see a slight decrease from HUF16891bn to HUF16391bn (-3% year-on-year, 17.9% of GDP). Gross HGB issuance should be roughly stable from HUF5266bn to HUF5496bn (+4.4%), but net issuance should fall significantly from HUF2945bn to HUF1783bn (-39.5%) given the historically large maturity of HGBs this year.

The debt agency indicates a continued focus on the belly of the curve, and the average maturity of current debt of 5.1y should not change much this year. At the same time, we observe a continuing trend of HGBs returning as the main funding source, while the share of retail issuance continues to decline.

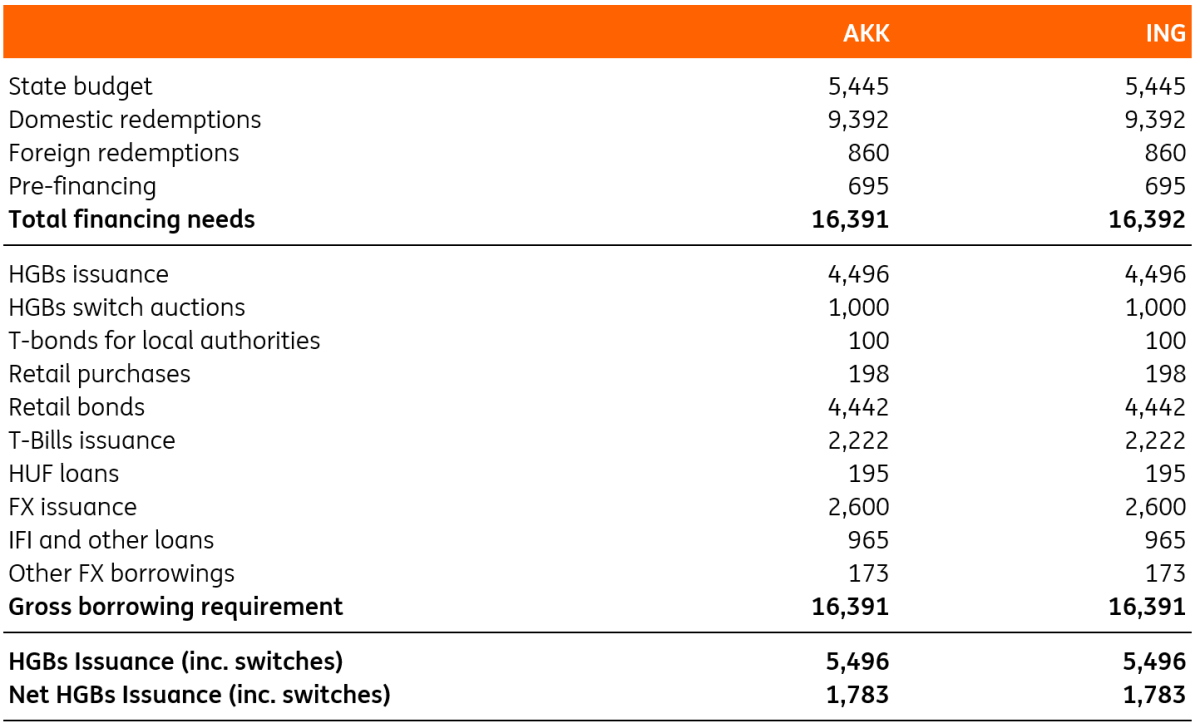

Financing needs for 2026 (HUFbn)

FX issuance: diversification remains the name of the game

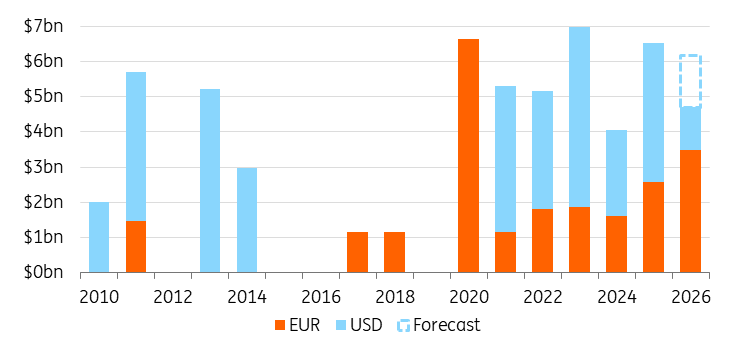

In 2025, Hungary’s FX bond issuance was revised higher, with a $4bn dollar deal added on top of the €2.5bn issued at the start of the year.

Fiscal policy is budgeted to remain steady, with a deficit of 5% of GDP planned, and in turn, €5.2bn in conventional (USD and EUR) international bond issuance is pencilled in for the full year. The debt agency has again been quick off the mark with €3bn issued in January, including a green bond, before a $1.2bn tap that completes over 75% of the plan for the full year. We expect there is scope for further USD issuance, with around $1.5bn of the initial plan remaining, although timing here is complicated by April’s elections, given the AKK’s preference usually to front-load Eurobond issuance in the first half of the year.

Hungary EUR & USD international sovereign bond issuance (USD equivalent)

Outside traditional Eurobond financing, Hungary is set to continue its strategy of diversification. The financing plan includes a €0.5bn issuance in the Asian market, €1bn in Euro Commercial Paper, and €2.5bn in foreign currency loans – largely from the EU's new security loan program (SAFE).

In turn, we think risks skew slightly to the upside in terms of the potential for more Eurobond issuance than expected, given the overall fiscal uncertainty, as well as reliance on disbursements from the EU for part of the FX financing requirements. The government recently introduced more flexibility in its medium-term target for the share of FX within government debt, which now has a tolerance range of +/- 3pp around the 30% level.

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more

Authors

Included in the following bundle

CEE Issuance Outlook 2026: Diversify, pre-fund, switch, repeat

- This bundle contains 8 Articles