Czech Republic: The end of fiscal consolidation

- 26 February

- FX Czech Republic

Fiscal policy has remained just slightly looser after the election; the deficit is expected to sit at 2.2% of GDP this year, with upside risks. Borrowing needs are rising, driving more CZGB issuance, with the Ministry of Finance focused on long maturities and higher secondary-market activity. FX issuance remains negligible and under local law only

Fiscal policy: Only a slight relaxation after the change in government

The Czech public finance deficit ended last year at 2.0% of GDP and is expected to be 2.2% this year, according to the Ministry of Finance estimates, although the state budget is only at the beginning of the legislative process. While the elections brought a change of government, we have seen only a slight loosening of fiscal policy and pessimistic market expectations have not been fulfilled. The main test, however, will be next year's budget, when the new government will have full control over fiscal policy and the changes discussed in the legislative process. In our forecast, the state budget cash deficit this year is broadly in line with the Ministry of Finance’s projections – but due to arms contracts and unclear EU flow, we see an upside risk of a 2.2% public finance deficit (ESA methodology).

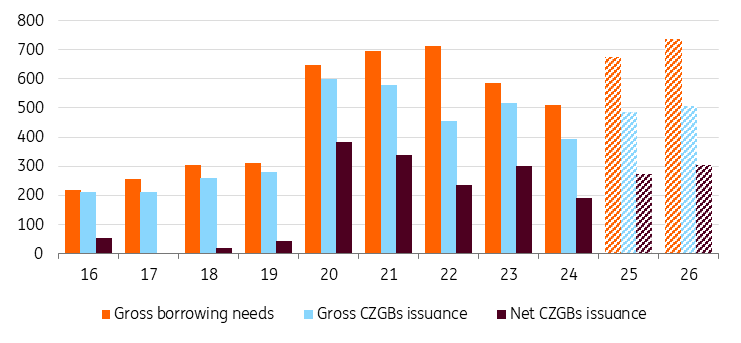

Gross financing needs and CZGB issuance (CZKbn)

Local issuance: Higher needs mean higher activity on the secondary market

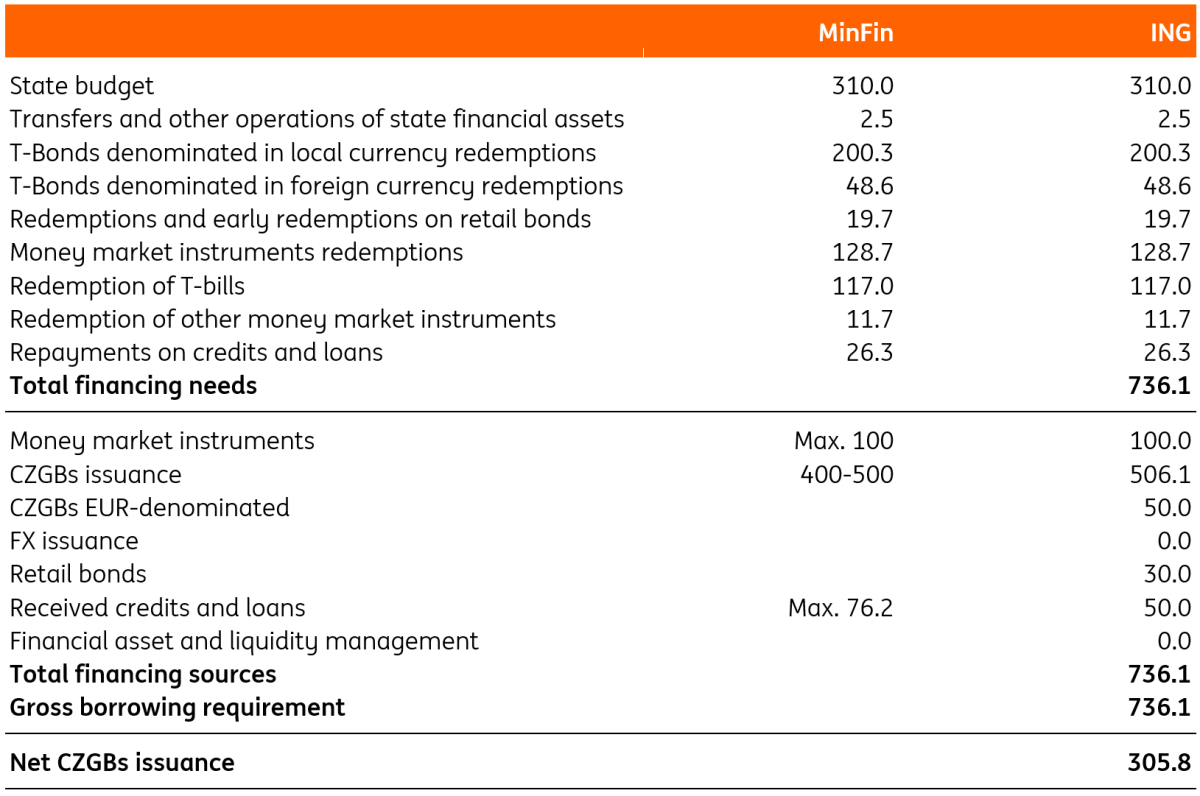

While the state budget cash deficit this year should be higher than last year, MinFin managed to pre-finance a large part of this year's redemptions at the end of last year and push this year's gross borrowing needs lower. In our forecast, we expect an increase from CZK673.5bn last year to CZK736.1bn this year (+9.3% year-on-year, 8.2% of GDP). MinFin guides for gross CZGB issuance in the range of CZK400-500bn for this year while we expect an increase from CZK486.2bn to CZK506.1bn (+4.1%), with net issuance increasing to 305.8bn (+12.4%). MinFin also relies heavily on T-bill issuance, which we estimate at CZK 100bn. In addition, around €2bn of EUR‑denominated CZGBs issued under local law will be refinanced this year. MinFin could also draw up to CZK76.2bn in loans from supranational institutions (EIB).

MinFin continues to focus on issuance at the long end of the curve with an average issuance maturity of 11.8y last year. The average debt maturity remains at 6.2y and no major changes to this strategy are expected. The risk towards higher issuance of CZGBs is the possibility of pre-financing next year through switches in the secondary market, where MinFin increased activity recently.

Financing needs for 2026 (CZKbn)

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more

Authors

Included in the following bundle

CEE Issuance Outlook 2026: Diversify, pre-fund, switch, repeat

- This bundle contains 8 Articles