Is credit now impervious to the Middle East conflict?

- 29 April

- Credit

Credit has fully reversed the widening triggered by the Middle East conflict, despite ongoing uncertainty. In a more severe scenario, we could see more weakness and a larger dispersion between sectors. Our main concern, however, is the potential for this to light a fire under private credit

Spreads have retraced fully despite lingering uncertainty

One could argue that the reaction in credit has been somewhat muted to the conflict in the Middle East. There was some widening in the initial weeks, but this was not a significant sell-off, with only 10-15bp widening across the EUR Investment Grade. Since the announcement of a ceasefire, spreads have retraced fully and are actually sitting tighter than before the conflict in many sectors, despite uncertainty still very much at the forefront.

The more notable rise in swap rates over the past two months has resulted in additional demand for credit, as yields have increased. At this moment, the additional yield on offer within credit is some 50-60bp extra compared to before the conflict.

Meanwhile, primary markets weren’t exactly closed either. There was some slowdown, but overall many deals were still completed, particularly on the corporate side. It did come with a touch more new issue premium (NIP) being demanded from investors, as the average NIPs moved up from 0-5bp to 5-10bp.

The modest widening and subsequent retracement were rather uniform across the different sectors. Some sectors are seeing a touch of underperformance (and or a lag in retracement) but it is marginal, in the likes of autos, some consumers and real estate.

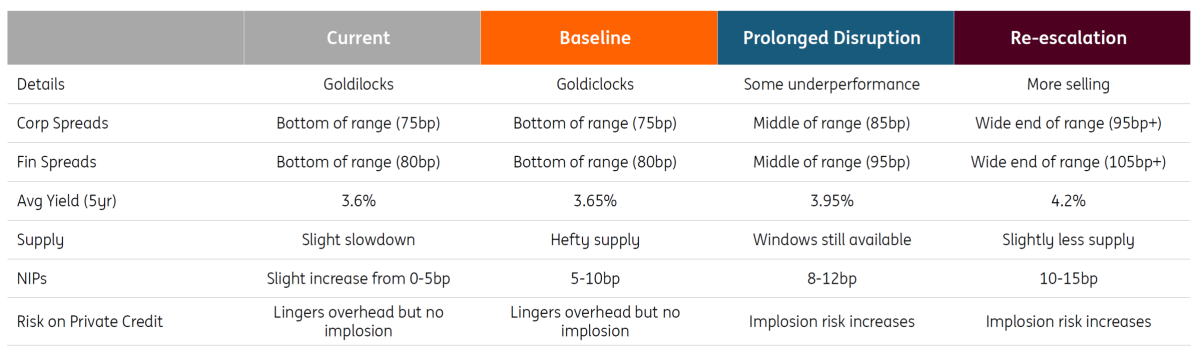

Three scenarios for credit

What happens to credit under the three scenarios?

Within our report 'Three scenarios for energy, central banks, rates and FX markets', the potential outcomes of the conflict are outlined. The base case scenario is for talks to drag on, but a deal will ultimately be reached, with a one-off rate hike in June from the European Central Bank. In this scenario, it's somewhat par for the course for credit. Spreads will remain on the tight side, with very strong demand and busy primary markets – the "just right" goldilocks fairytale scenario continues unless/until we see further deterioration in private credit markets.

In a more severe scenario of either a prolonged disruption or even a re-escalation, it may lead to inflation/stagflation and further rate hikes, pushing swap rates higher and ultimately more inverted in the second half of the year. This will put pressure on credit markets, but the additional yield will keep things contained. But more dispersion between sectors is expected.

Could this light a fire under private credit?

The biggest concern for credit in a more severe scenario is that it could lead to triggering a larger deterioration in private credit, an already growing concern. With higher energy prices, higher rates and a weaker economy, more questions are being asked of the underlying businesses, of which a very large concentration is tech, AI, software, SaaS and healthcare.

Higher funding costs, AI surprises and geopolitical stresses (as well as some questionable rating practices) may lead to a jump in defaults and further redemptions from private credit funds. This leaves insurers, US regional banks and, to a lesser extent, European banks as the most exposed. But ultimately, risk would need to be repriced wider. Read more on our thoughts on private credit in our report 'Private credit: Is the Goldilocks period over for credit?'

In this more severe scenario, we should see more dispersion between sectors

With higher energy prices and larger supply chain disruptions, sectors such as autos, retail, household goods and consumer goods will be most impacted. Additionally, the transport/logistics sectors will come under pressure as energy prices rise, in particular the likes of the shipping and airline sectors.

Thus far, many of the industrial sectors have been trading in line with market moves, in some cases even outperforming slightly. In a severe scenario, many industrials will be under pressure from the weakening of economic data, alongside some growing competition with China, as European production slows. The likes of chemicals, paper/packaging, mining, steel, cement, and so on are energy-intensive and tend to lack the ability to pass through costs.

With rate hikes and higher swap rates, the real estate sector may see some underperformance. We are already seeing weakness in logistics real estate.

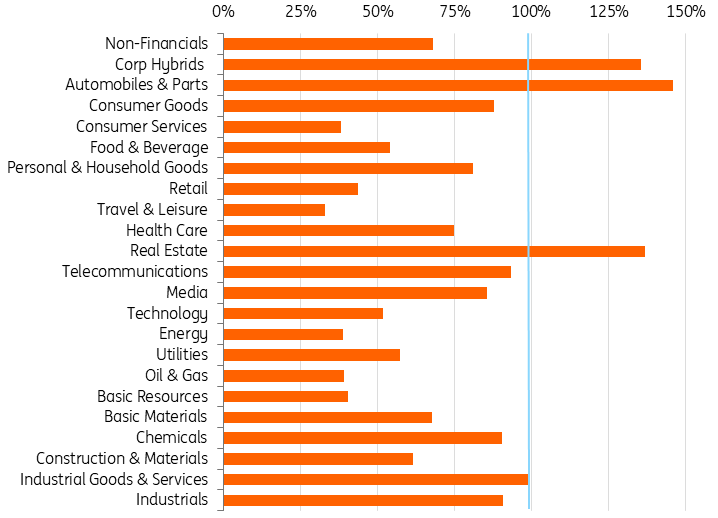

% of widening in 2026 versus widening in 2022

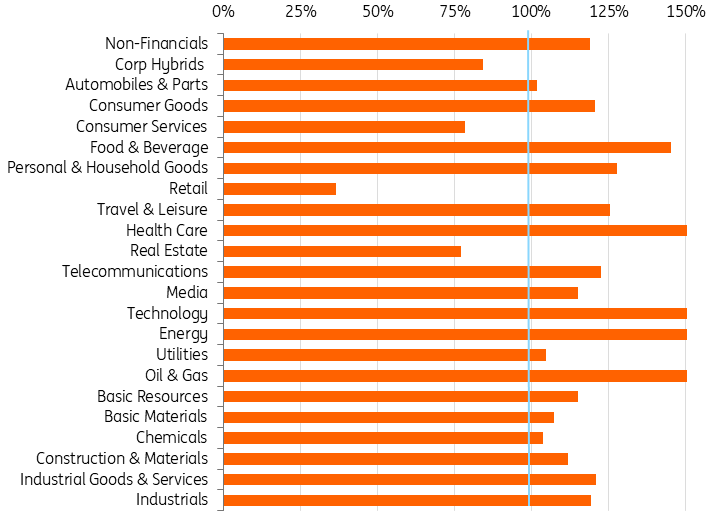

Recent retracement from the 2026 wides

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more