ING Survey: When the pandemic gets personal

- 10 December 2020

Governments across the world have spent much of 2020 concerned about balancing the health threat from the Covid-19 pandemic with the economic damage lockdowns can cause. It is the same for households – a third say health trumps finances and a third say the opposite when it comes to what worries them most

Health vs Finance

As early as May 2020, the United Nations warned that a scourge from the pandemic would be its impact on mental health. It foresaw not just a crisis among people distressed by the health aspects of the virus and the consequences of physical isolation, but also by the economic turmoil from having lost or being at risk of losing their income and livelihoods.

The fallout from this global stress storm will be long-term, and Europeans are clearly concerned about their health. When the latest ING International Survey asked 12,802 people in 13 European countries whether health or finance concerned them most, 37% said health.

But as the UN suggested, personal finance was very close behind. Thirty-five percent of respondents said they were more worried about their finances than their health. When you consider the 17% who said that both concerned them equally, it was pretty much a draw.

It is not hard to understand why. The euro area's unemployment rate has climbed steadily since the pandemic hit in March to more than 8%, with predictions that it will rise more by the end of the year. The International Monetary Fund, meanwhile, predicts that the euro area's overall economy will contract by more than 10% this year (ditto Britain's). The latter alone is a major threat to livelihoods.

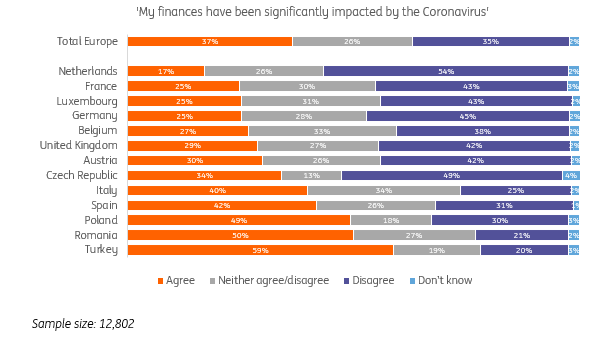

The ING survey found that it was not just a case of worry. More than a third (37%) of Europeans reckoned their personal finances have been significantly impacted by the pandemic and around a third (32%) of respondents specifically said that their income had been reduced during the pandemic.

Conversely, 53% said there had been no change to their income and 12% had even reported an increase.

There are a number of reasons for this disparity. One is that the virus has hit different countries differently (see Box), partly as a result of factors such as the largesse of governments. Another is that the pandemic is not egalitarian: it has had greater financial impact on poorer people.

When responses were broken down by income level, twice as many of the poorest reported significantly suffering financially than not, presumably, in part because the lower-paid have few buffers and tend to work in sectors that have been closed in lockdowns such as hospitality and shops.

Roughly half of people with less than €1,000 in net monthly household income (or currency equivalent) said they had been significantly impacted by the pandemic; by contrast, only a quarter (26%) of those bringing in €7,000 or more said so.

For richer or poorer

Just as with infections and deaths, Covid-19 has hit different European counties unevenly when it comes to personal finances; in general, people in the poorer countries are more likely to report a significant impact from the pandemic. *The region's four G7 countries -- Germany, France, Britain and Italy -- had an average of 27% of people saying they had been significantly hit financially (Italy being the worst at 40%). *By contrast, Turkey, Romania and Poland all registered at least 50% (with Turkey the worst at 59%). *The least-impacted country was the Netherlands, where only 17% or respondents reported a financial hit.

"The economic impact of the coronavirus was relatively mild in the Netherlands compared to the rest of Europe. The combination of the sizable Dutch income support measures and the speed of implementation may also be behind the relatively small number of people in the Netherlands who say their finances have been significantly impacted by coronavirus. The Dutch also structurally have a strong social safety net – including relatively high public spending on unemployment benefits and incapacity -, and theoretically therefore, a smaller number of people who would agree with their finances being “significantly” impacted by coronavirus than in other countries." - Marcel Klok, Senior macro-economist for the Netherlands.

It is at this point that the psychological concepts of Optimism Bias and its opposite, Pessimism Bias, appear to have kicked in. These are cognitive situations in which people believe that something negative/positive will not happen to them and, consequently, have positive/negative views about the future, respectively.

In a nutshell, people who said they had been significantly impacted by the pandemic were far more likely than others to say that the economic situation in their country would get worse before it gets better.

Hit at Home

This pessimism -- or maybe it is just a logical reaction -- is also clearly seen in the attitudes of people towards their housing situation. If you have been hit financially by the pandemic, the chances are you have a) gone into debt, b) are not happy with where you live and c) plan to move.

Of the respondents to the ING survey who said they either had had to go into overdraft and/or borrow more money, or compromise on their standard of living to pay their mortgage or rent (20% of Europeans), three in five (60%) said their finances had been significantly impacted by the Covid-19 crisis.

Gloomy Europeans

Consumer sentiment in the European Union has been battered by the Covid-19 pandemic, an overall attitudinal drag that is bound to have been reflected in the ING survey responses. For all but the first few months of 2020, the European Commission's consumer confidence indicator has been deep in negative territory, well below the-long term average (which itself is negative).

In April this year, the indicator sank to minus 22%. It has only been as low as this on a couple of occasions in the past 25 years -- during the global financial crisis of 2007-08 and the eurozone debt emergency that peaked between 2010 and 2012. The pandemic is on a par with these as a financial disrupter.

Meanwhile, the people who have been struggling financially because of the pandemic may have also been pushed into making life-changing decisions about where they live.

First, around half (48%) of those looking to move in the next six months say their finances have been significantly impacted by Covid. This is nearly twice the number who have not had financial problems and say this (27%). Second, people who have had pandemic-related financial problems are far more likely to be planning a move in the next two years than people who have not had difficulties.

Unhappiness with current housing is not, of course, all down to the pandemic and pandemic-related financial stress. As has been reported here previously, the survey found that people who are currently working are more likely to say they are planning to move within the next two years than those who are not. So, the aspiration to move may be motivated by a voluntary desire to find new opportunities and not just forced by negative financial considerations.

The pandemic has clearly wrought financial as well as physical harm on millions of people, driving many to change their behaviour. Roughly a fifth (17%) say their finances are worrying them more than their health and a third (35%) say both their health and finances worry them equally.

The 37% of Europeans who say their finances have been significantly impacted by Covid are also more likely to be unhappy with their housing situation and looking to move. Highlighting the possibility of more disruption for many.

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more