ING Survey: Pandemic or not, Europeans want to move home

- 10 December 2020

The Covid-19 pandemic has brought with it massive changes to people's behaviour and attitudes, shifts based on societal uncertainties that may be with us for decades. How—and where—we live is no exception

Moving aspirations live

There has been plenty of attention focused on how the virus has forced families to avoid being in close contact with friends and loved ones, on how it has forced even technophobes online, and on how it has tested societies over issues as anomalous as whether or not to wear a face mask.

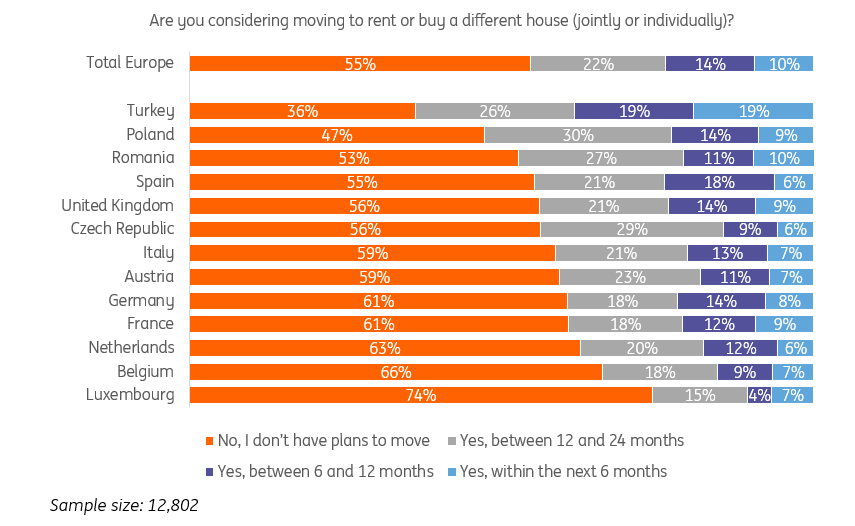

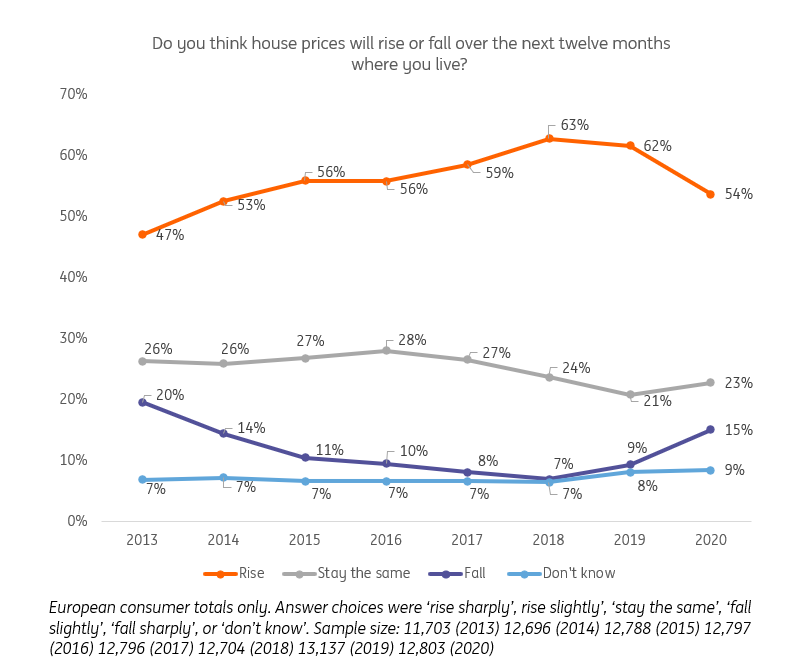

But one unheralded change, unearthed in the latest ING International Survey, is that a large number of Europeans (45%) are thinking of moving home. This is accompanied by an increase -- almost unprecedented in recent years -- in those who believe house prices will fall, or at least stop rising for a while (54% say house prices will rise in the next 12 months v 63% who said the same in 2018).

The survey of 12,802 people across 13 European countries asked a series of questions regarding respondents' happiness with their housing situation and what plans they may have for changing it.

Just under half said they were looking to move within the next 24 months, with about a fifth of this group (22%) wanting to do so with the next six months. Given that there are around 113 million households in Germany, Britain, France and Italy alone, this lays the ground for a major transformation.

It is not clear exactly how much the pandemic has played into this desire, but it is logical to assume some impact. Lockdowns, for example, have forced people to stay at home, thus highlighting any shortcomings there. Economic hardship -- the International Monetary Fund predicts a more than 10% economic contraction in the eurozone this year -- may also be driving people to look for cheaper places to live.

And the coronavirus has prompted a huge shift towards working from home for those who can do so.

The survey found that those currently working are more likely to say they are planning to move within the next two years than those who are not (52% working v 44% non-working). This most likely reflects income and, therefore, opportunity.

But it could also be seen as a sign of the new paradigm in which people are not required as before to live near their place of work -- either because they work from home or in newly established remote hubs.

Underlining this, Yolande Barnes, chair of University College London's Bartlett Real Estate Institute, lists as one of the top potential impacts of the pandemic on housing: "More continued home-working that changes demand for both workspace and the configuration of homes".

Who wants to move?

Among the people the ING survey found most likely to be considering moving home:

• Younger people (many seeking a move within the next six months) (on average 35% of those under 34 say they aren’t planning on moving v 61% of those aged 45-54);

• People currently working (52% of those working v 44% not working);

• Renters, and people living with flatmates (48% of renters and 45% of those with flatmates say they aren’t planning on moving v 66% who own without a mortgage);

• Turks and Poles (more than 50% planning to move; younger populations) vs people in the Benelux countries, Germany and France (less than 40%; generally older).

Cheaper housing?

Another major factor in Europeans wanting to move is a growing belief that housing may be getting cheaper.

To be clear, most Europeans, according to the survey, still expect to see house prices where they live rise in the next 12 months. Some 54% said so. But this was a significant fall from previous years. Last year, the percentage expecting a rise was 62%.

The percentage of those expecting house prices to fall is now higher (at 15%) than at any time since 2014 when the eurozone was just emerging from its sovereign debt crisis almost everywhere except Greece. Nearly one-in-four (23%) people, meanwhile, reckon prices will stay flat.

The evidence for house prices falling or staying flat is not strong. Eurostat second-quarter figures, released in October, showed that house prices in the European Union rose 5.2% year-on-year. It was a smaller increase than the first quarter year-on-year number (5.6%), but solid growth nonetheless -- and among the highest rates in the past decade.

The people now expecting house prices to fall or level off may simply be looking ahead and expecting the pandemic to get worse and the economy along with it, taking prices down. Consumer sentiment in Europe remains in negative territory, after all, amid a second wave of the virus.

But it also could be that people are conflating prices with affordability. Last year, for example, house prices across the whole of Britain rose 2.2% (London is a major aberration), but the Office of National Statistics reported that the ratio of earnings to house prices dropped -- meaning that people were better placed to buy than in the previous year.

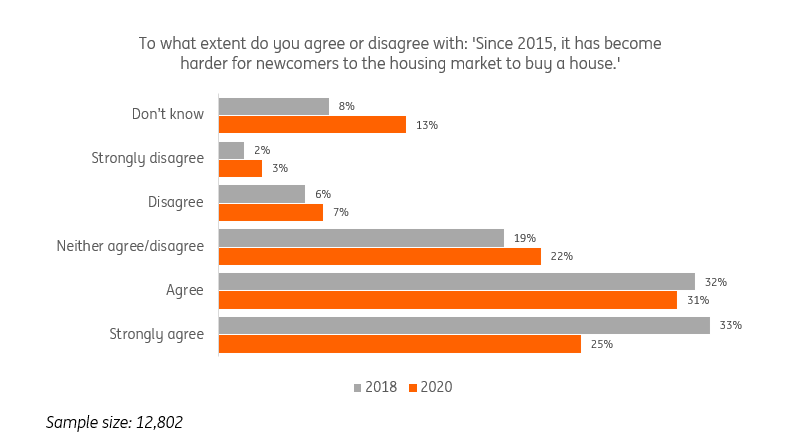

Significantly, compared to two years ago, the ING survey shows that fewer people appear to believe that it is getting harder for newcomers, or first-time buyers, to purchase their own home.

Some of this may be the result of pandemic-related factors, such as tax breaks (Britain, for example, has eased its stamp duty on some home-buying and selling, while Germany has indicated it will not raise any taxes). Or it may be that the cheaper mortgages now available simply make buying easier (see box).

Mortgage momentum

A series of crises -- the financial implosion of 2007-08, the eurozone's sovereign debt meltdown, the current pandemic -- has kept official interest rates at historic lows. The European Central Bank's refinancing rate, for example, is just 0.05% while the Bank of England's benchmark rate for sterling is barely higher at 0.1%. This has meant that monthly payments (if not the purchase price) for homes are cheap, even for existing holders who have mortgages that track the benchmarks. At the end of 2019, tracker rates in Germany were 1.28%, in Italy 1.44% and in Spain 1.44%. In Britain, tracker rates of less than 1.6% are available, albeit with a time limit. An issue for the future will be what happens when the base rates underlying these bargains eventually rise.

Indeed, this is all part of a recent curve: the percentage of people in our surveys saying it is easy for them to pay their rents or mortgages has slightly risen since 2017 (44% find it easy in 2020 v 34% in 2018) despite the recent economic hardships.

This may be one reason why the number of people agreeing with the statement "Since 2015, it has become harder for newcomers to the housing market to buy a house" has dropped to 56% of respondents in the new survey from 66% in our 2018 survey.

It is worth noting again, though, that these are trends, not majority views. Just as more than half of respondents continue to expect house prices to rise over the next year, so a similar bloc expects it to continue to get harder for first-time buyers, not easier.

It will all, presumably, depend on how the Covid-19 pandemic plays out and how it hits personal finances as well as macroeconomic conditions.

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more