GBP: Out of control

- 30 November 2018

- FX United Kingdom

The UK is barely four months away from leaving the EU, but the nature of the departure, let alone the future relationship with Europe remains highly uncertain. In the options market, GBP is now trading a bit like EM currencies. We can’t see this environment changing before 29 March 2019. however, there would be no saving GBP under a no deal scenario

GBP has been on a wild and mostly declining ride since the Brexit vote in June 2016. It’s not fair to say that nothing has been achieved since then. We do, after all, now have a 585 page Withdrawal Agreement. However, the nature of the UK’s departure from the EU and its future trading relationship with that bloc remains highly uncertain.

One thing our team does agree on is that things will get worse before they get better. Barring a second referendum reversing the Brexit vote, the term ‘better’ is still economically worse than our prior relationship with the EU. In terms of GBP forecasts, we think EUR/GBP could still have another run at the 0.91/0.92 area by the end of this year as PM May struggles to get her Withdrawal Agreement through parliament at the first attempt. There is now speculation of a second vote as late as February 2019.

GBP is trading on an option volatility associated with the EM world (%)

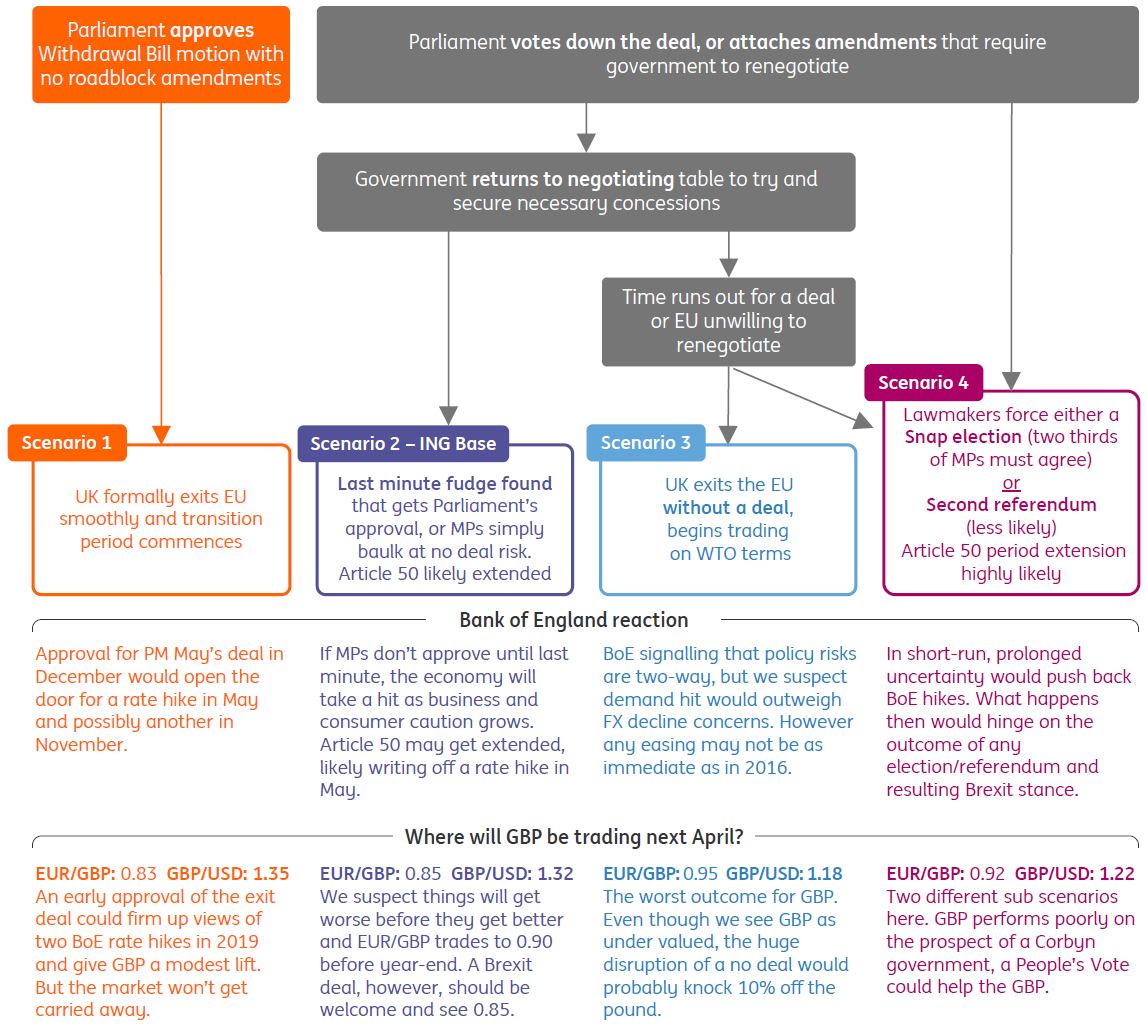

As the high volatility of GBP attests, transparency is especially poor right now. In the graphic below, we show a variety of Brexit scenarios and their impact on GBP. In fact, we feel constrained by limiting the number of scenarios to four!

There are not too many positive GBP scenarios. While some certainty over an orderly Brexit would be welcomed by markets, the move to fully price two BoE rate hikes in 2019 may only be worth 2-3% GBP upside. This is because we see very little progress on the UK’s ultimate relationship with the EU next year. It will probably take a year for the UK Parliament to work out what it really wants. And perhaps more importantly recent EU unity on the subject could easily evaporate as vested interests come to the fore - think Spain on Gibraltar, northern Europe on fisheries policy.

Some illustrative Brexit scenarios

Away from our low-confidence baseline view that EUR/GBP ends next year around the 0.85 area and Cable at 1.41, the alternative scenarios appear pretty GBP negative.

As we noted recently, a change in the UK leadership could quickly insert a 3-4% risk premium into GBP. Either a more pro-Brexit Conservative leader or a general election and the chance of a socialist Labour government would see GBP weaken.

No one wants a No Deal Brexit and our team attach only a 25% to it happening. In its unlikely event, we doubt any of the fair value measures would be able to offer GBP much support. Frankly, we guess at around a 10% fall in GBP under such a scenario.

On the subject of fair value, our EUR/GBP BEER model worked well around the time of Brexit (we had felt that EUR/GBP was stretched at 0.91/0.92 at that time and would not trade to parity). That model again sees EUR/GBP as very expensive now. However, a No Deal Brexit could well temporarily blow away what is, after all, a medium-term fundamental fair value model.

For the short term, we prefer to use a Financial Fair Value (FFV) model, which identifies how much EUR/GBP is trading away from variables like interest rate spreads and risk indices – which normally do a good job of explaining EUR/GBP price action.

Currently GBP is trading at a 1% risk premium. That risk premium had been 4% as recently as August, when the first wave of Brexiteers resigned from May’s cabinet. And we do recall 6%+ risk premia around the time of the Scottish referendum in 2014. In short, GBP has room to go lower.

Expect the UK macro story to continue to play second fiddle to the Brexit story. For reference, we happen to see UK GDP in a 1.3-2.0% range through 2019 (on a QoQ annualised basis). CPI should peak around 2.5% this year and soften to 1.8% by end-2019.

The BoE would prefer to be hiking twice per year in a normal environment. However, Brexit will determine the pace of any further tightening and, at this stage, we see one hike next May (taking Bank Rate to 1.00%) and then two further hikes in 2020.

This report is part of our 2019 FX outlook published November 2018

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more