3 calls for Asia as inflation begins to fall

- 7 July 2022

We believe that inflation will dip in the second half of this year across Asia, helped by declining food prices. There will be a catch-up period for those central banks which have tried to 'buy' growth with low interest rates

Bank of Japan will stick to its yield curve control policy

There has been a lot of speculation that the Bank of Japan (BoJ) might amend its yield curve control policy in the coming months. Most of this speculation stems from outside of Japan. Within Japan, fewer forecasters seem to think any change is likely. Yield curve control sees the BoJ in the market daily to buy unlimited 10Y Japanese government bonds (JGBs) at 0.25% as required. And yet there have still been some days when the yield has topped the 0.25% upper target (the central target range is zero).

Combined with some extreme weakness of the Japanese yen, which has helped import global inflation into Japan, this has encouraged thoughts that the BoJ might widen the band to 0.5%. However, the bank expanded its open market operation purchases from 10Y JGBs to 7Y JGBs, which signals that the BoJ will keep the current target though to the year-end, though there may be some change to this next year when BoJ governor Haruhiko Kuroda is due to step down.

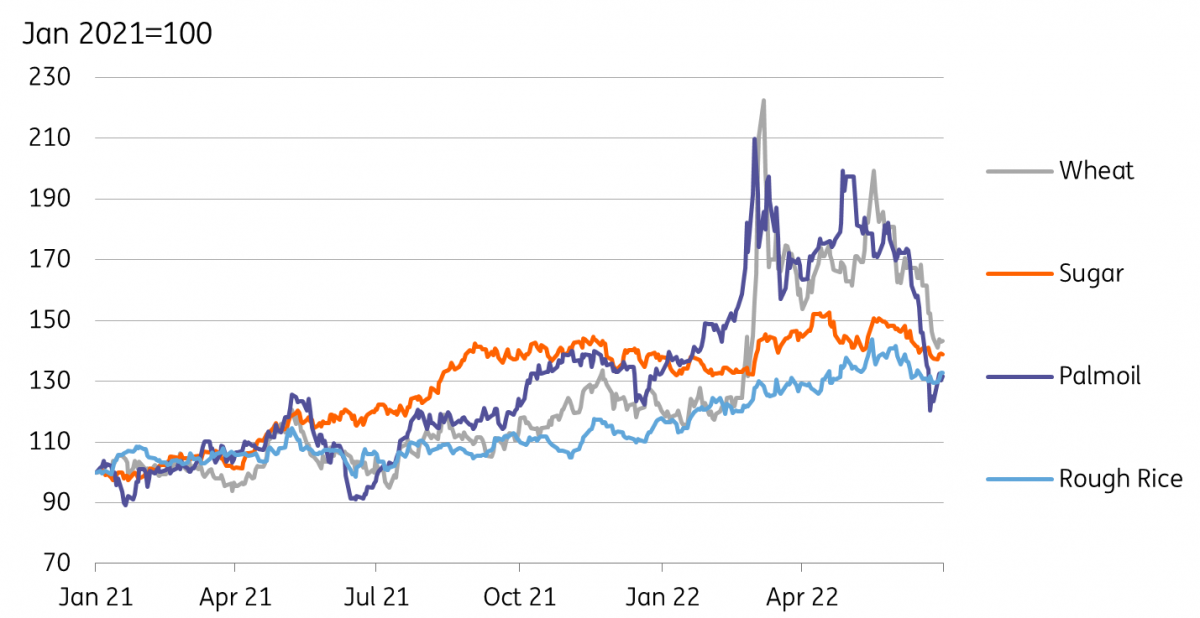

Inflation rates across Asia could already be coming down

The last month has seen agricultural prices from wheat, sugar, rice and palm oil, among others, tumbling from recent highs. Food prices play an extremely important role in overall inflation in Asia. Those central banks that have already hiked rates aggressively to reduce the gap between inflation and policy rates may even be in a position to reduce them slightly, or at least the market will be able to anticipate some loosening earlier in 2023 than anticipated.

The central bank laggards will have to play catch up

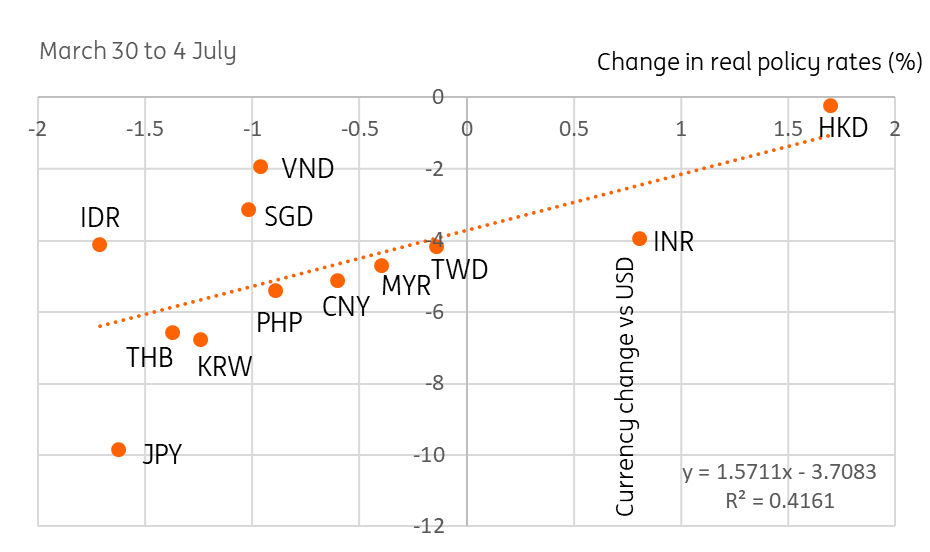

One thing that's become apparent in recent months is that no economy in Asia ex-China is immune to global inflationary pressures. And even where inflation remains relatively muted, in absolute terms, it is testing central bank tolerances. A couple of central banks in Asia have made no, or only token, responses to higher inflation, and as a result their real policy interest rates have fallen, and their currencies have depreciated. This will drag in more inflation, which is ultimately a false economy. They will end up having to do more over the second half of the year than those that have been bolder.

Asian FX and change in real rates

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more

Included in the following bundle

ING Monthly: Europe’s recovery is cancelled

- This bundle contains 14 Articles