Indonesia sees robust growth amid external challenges

- 28 September 2023

- Indonesia

Indonesia’s growth engine is motoring along but can it continue amid so many global headwinds? We take a look

Steady as she goes

Indonesia's growth performance has been a model of consistency despite global headwinds. Outside Covid 19 in 2020 and the base effect-induced bounce in 2021, Indonesia has managed to post a steady pace of roughly 5% year-on-year growth dating as far back as 2016.

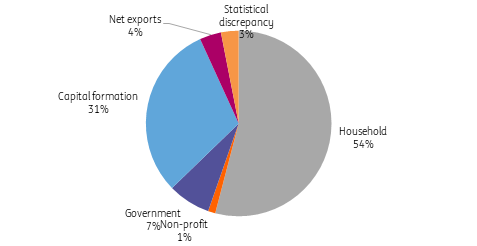

Growth remains heavily reliant on household consumption (54% of GDP) although Indonesia’s growth momentum has received a lift from capital formation and from exports during select periods. In 2022, Indonesia enjoyed a banner year for trade with the export sector benefiting from a sharp uptick in global energy prices.

For 2023, with coal prices moderating, Indonesia has relied more heavily on domestic household consumption which saw a modest rebound due to softening inflation in the first half of the year. And despite a challenging external environment and an upcoming general election in the first quarter of 2024, we expect growth to motor along at the steady pace of 5% YoY with economic growth delivered by still solid household spending and robust capital formation.

Household consumption still main driver for growth

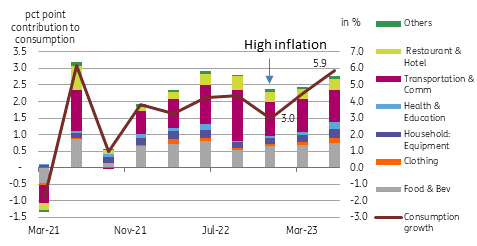

Household spending takes on the heavy lifting in 2023

Domestic consumption posted slower growth at the end of 2022 with households cutting back on expenditures amid above-target inflation. However, with inflation moving back within target by mid-2023, we’ve seen household spending recover and up by 5.9% YoY as early as the second quarter of 2023.

Quicker spending was reported across almost all subsectors outside transport with a notable pickup for food & beverage (3.8% YoY), clothing (7.0% YoY), household equipment (3.8%), health & education (5.1%), restaurants (6.7% YoY) and other services (3.7% YoY).

We can expect household spending to remain robust in the near term for as long as inflation remains well-behaved and within the central bank’s inflation target.

Household spending hit a snag during high inflation episode

Inflation back within target but food price spike bears watching

We have seen how sensitive household spending has been to bouts of high inflation. As mentioned earlier, inflation has moved back within Bank Indonesia’s target of 2-4% YoY with the latest inflation report showing headline inflation down to 3.3% YoY and core inflation at 2.6% YoY.

The recent uptick in global food inflation, however, could nudge headline inflation higher, closer to the upper end of the BI's target. Food inflation is on the uptrend, rising to 3.5% YoY and driven partly by surging rice prices (13.8% YoY) due to high global prices for the staple. The El Nino episode hit rice production in the region, forcing domestic rice prices to touch levels last seen in 2012.

So far, despite the sharp uptick in food inflation, headline inflation remains within target. However, a sustained acceleration in food and energy prices could eventually sap some momentum from the all-important household spending.

Recent food price spike is worth monitoring

Bank Indonesia hopes to support growth via lending programmes

BI raised its policy rates aggressively to support the Indonesian rupiah in a bid to deal with above-target inflation back in 2022. Overall bank lending is slowing due to BI’s tightening cycle. In terms of the sectoral breakdown, the top three sectors in terms of lending are financial & insurance activities, wholesale & retail trade and mining & quarrying.

In order to sustain its support for growth, however, BI opted to implement loan programmes designed to help stimulate lending to pre-identified key sectors.

BI announced incentives to lower the minimum reserve requirement for banks that lend to four “priority sectors”. These sectors include 1) the mineral and mining industries (including manufacturing activities related to mineral mining), 2) non-mineral industries (including manufacturing activities related to non-mineral mining), the housing sector and the tourism sector. Furthermore, additional incentives will be granted to banks that lend to all four priority sectors as well as satisfy the criteria for macroprudential inclusive financing ratios and green financing as required by the central bank.

With BI’s incentive programme for lending, we could see more funds channelled to manufacturing, other services and the housing sector which would be supportive of the growth outlook despite elevated borrowing costs.

As bank lending slows, BI counters with incentive programmes

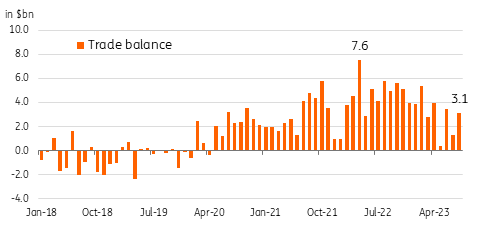

Export sector remains challenged in 2023

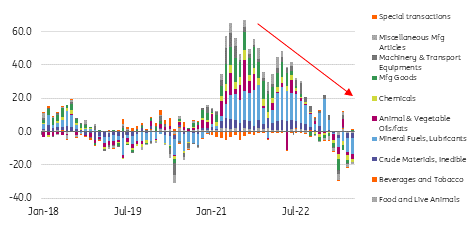

One sector, however, that has not contributed to growth momentum this year is the trade sector. Exports, which had been a key source of economic expansion in 2022, have reversed into contraction. After a banner year supported by elevated energy prices, the export sector has struggled in 2023 and has not been able to provide the same kind of lift compared to last year.

Exports of mineral fuels (coal) and animal & vegetable oils (palm oil) have been the heaviest drags on the export sector with only exports of steel & iron plus road vehicles reporting better outbound shipments year to date. We can expect the export sector to remain subdued in the near term or until we see a substantial rebound in global demand. Until then, this sector will likely be a drag on the growth outlook in terms of its negative contribution to net exports and to the industrial sector.

Export boom fades quickly in 2023

Rupiah likely pressured for rest of year, BI to track Fed moves

The IDR is currently the only Asian currency to be up for the year, currently stronger by 0.8% versus the dollar. However, the currency has been pressured of late after support delivered by the trade surplus faded substantially throughout 2023.

With less support from the trade surplus at a time when the Federal Reserve has stayed relatively hawkish, the rupiah has come under pressure, with the currency retreating by roughly 1.6% in September. With global demand for exports likely soft for the rest of the year and into 2024, we do not expect a quick turnaround for the IDR with the central bank likely very active in the foreign exchange market to prevent a more pronounced depreciation.

Given BI’s priority of retaining support for the IDR, we expect the central bank to keep rates untouched for as long as the Fed is on hold. However, should the Fed decide to hike rates again in the next few months, we feel that BI will have no choice but to follow suit with Governor Perry Warjiyo possibly matching any Fed increase to maintain what is an already uncomfortably tight interest rate differential (25bp).

Key support for IDR has waned this year

The 2024 election is fast approaching

Indonesia will conduct general elections on 14 February 2024. Incumbent President Jokowi is not allowed to seek a third term. There are three main candidates to replace Jokowi, all of whom have ties to the current president.

Prabowo Subianto, who ran against Jokowi in 2014 and 2019, is the country’s current defence minister. Prabowo has vowed a platform that promises continuity and recently received the backing of two additional parties, solidifying his support, with four parties (46% of parliament) now supporting his bid for the presidency. Recent opinion polling shows him leading or in second place for the presidency.

Ganjar Pranowo is the governor of Central Java, a position previously held by Jokowi prior to his election to the presidency. He is backed by PDI-P, Indonesia’s largest party which is the same political party that backed Jokowi. Although Jokowi has yet to endorse a particular candidate, the PDI-P believes Jokowi would support Ganjar’s bid. Recent opinion polling shows him leading or in second place for the presidency.

Lastly, Anies Baswedan is a former governor of Central Java who was also the campaign spokesperson for Jokowi’s 2019 election bid. He also served as Jokowi’s Minister of Education and Culture indicating his close ties to the president. Anies, however, has fared less favourably in recent polling, consistently polling third behind Prabowo and Ganjar.

With barely four months to go before the February 2024 election, the top three candidates have yet to select their running mates or announce official campaign platforms. As such, we could still be in for changes in poll results in the run-up to the election but all three candidates appear to be presenting themselves as continuity candidates given President Jokowi’s still-solid approval rating.

Challenges remain but steady 5%+ growth seen this year and next

The global landscape presents substantial headwinds to Indonesia’s growth momentum. Soft demand and moderating prices for palm and coal have forced exports into a deep contraction for the year. With exports fading, the trade surplus has in turn also receded, resulting in the loss of a key support for the IDR in 2023.

Meanwhile, anxiety over Fed policy has forced up global bond yields, exerting additional pressure on the currency, which is down almost 1.6% for September. A weaker currency could exacerbate imported inflation pressures which in turn could dent household consumption should headline inflation accelerate past BI’s inflation target.

Lastly, a potential Fed rate hike could prompt BI to hike its own policy rates, which could sap even more momentum from flagging bank lending.

Despite these challenges, however, we believe that Indonesia will manage to post full-year growth of 5.1% YoY. Growth momentum will be safeguarded as household spending remains robust despite a projected pickup in prices. We believe a potential acceleration in price pressures due to rising food and energy prices could be offset by subsidies to key sectors which could blunt the impact of faster inflation on household spending.

Meanwhile, capital formation is also projected to remain in expansion mode even if BI hikes policy rates to track a Fed increase. We believe the BI will lean heavily on incentives for lending to key select sectors to ensure growth remains on track or at the very least is not heavily impacted by tightening liquidity conditions.

Lastly, we could also expect economic activity to accelerate in the months leading up to the general elections scheduled for February 2024. Thus we expect growth to settle at 5.1% for 2023 and 5% for 2024 with Indonesia able to sustain its steady pace of expansion despite substantial external headwinds.

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more