Indonesia: Recovery delayed but not derailed

- 24 March 2021

- Indonesia

Indonesia was counting on a quick bounceback in 2021 but any recovery may take a bit longer

Climbing out from recession

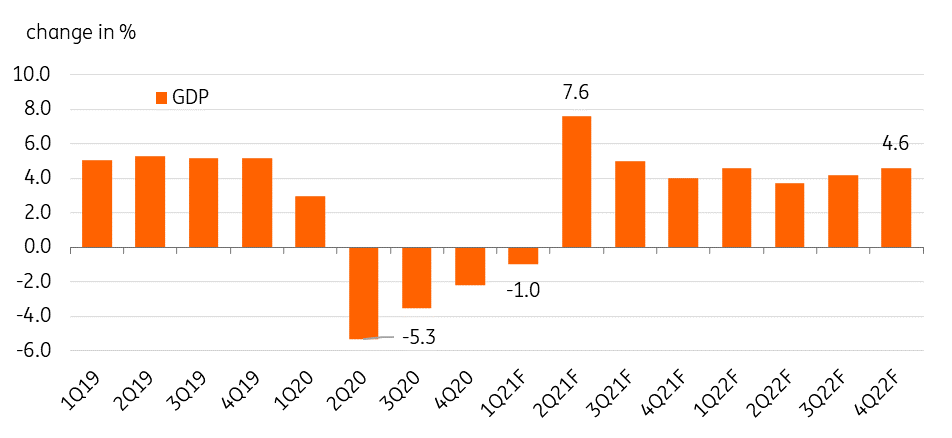

Indonesia’s economy contracted 2.1% in 2020, with the domestic market hit hard by Covid-19 related partial lockdown measures and weaker global demand for its export base. The authorities began the year hopeful for a 4.5 % to 5.5% GDP expansion delivered by improving consumer confidence and supported by another hefty dose of fiscal spending. However, a string of natural calamities (flooding, earthquakes and volcanic eruptions) and a sharp pickup in Covid-19 daily infections early in the year forced the authorities to trim their expectations for growth to 4.3% to 5.3% while also upsizing the fiscal stimulus budget to IDR553 tr from the original IDR372 tr. Due to these early setbacks and despite base effects, we continue to forecast a contraction in 1Q GDP with the strong bounce back in growth contingent on clamping down on Covid-19 spread and the much-touted vaccination programme.

Indonesia actual GDP growth and forecast

Economic momentum remains soft

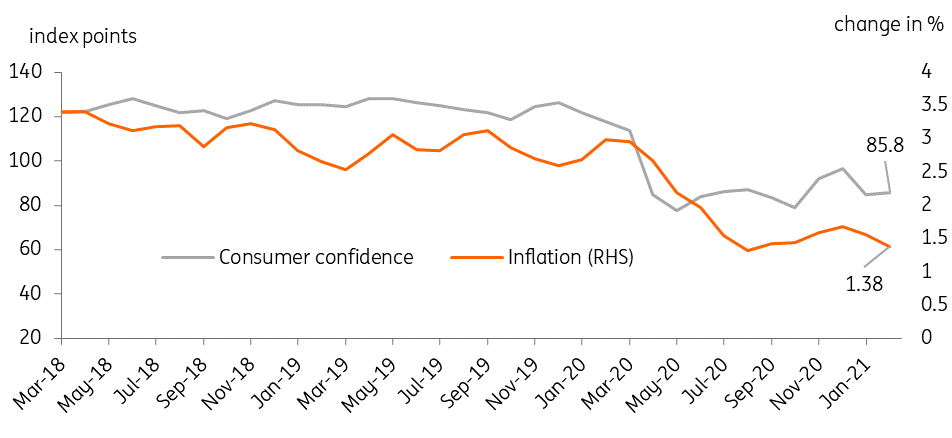

With the economy in contraction for 3 quarters and counting, consumer confidence has only barely improved from the depths of the pandemic. Due to relatively high levels of daily infections, partial lockdown measures have been reinstated in both Bali and Java for 4 weeks, weighing further on already weak sentiment and economic activity. As a result, inflation has remained below Bank Indonesia’s (BI) target range of 2-4% which allowed the central bank to lower borrowing costs to 3.5% in February. However, despite several rate cuts, bank lending has fallen sharply, yet another sign that the economy is still struggling.

Weak consumer confidence manifests in soft demand side pressures on inflation

Hopeful signs

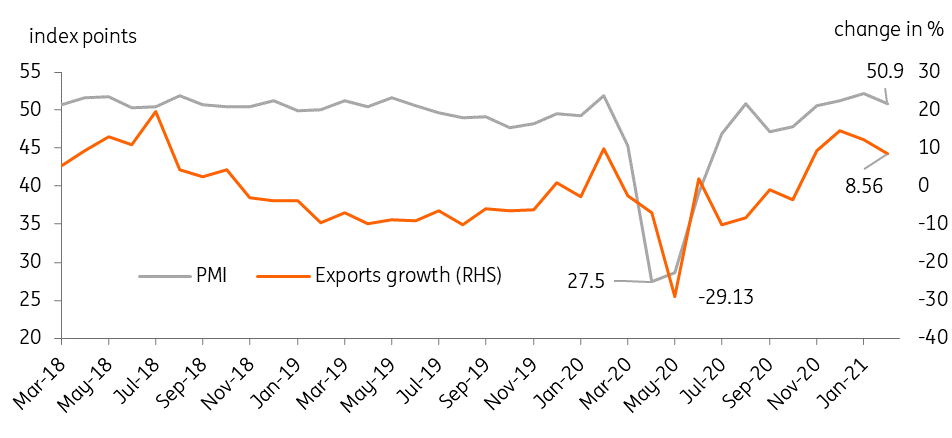

Despite the setbacks faced early in the year and a likely contraction in GDP in 1Q, we do note some promising signs that the economy may be finally turning the corner. Manufacturing activity has picked up in the past few months, tied in some part to gains enjoyed by the export sector. Outbound shipments of raw materials to China have helped carry the export sector to growth since November 2020 and if global growth is not derailed by third waves of the pandemic and picks up in the coming months, exports will likely continue this trend. Likewise, imports fell for 19 months in a row before finally returning to growth in February 2021. One key driver for this turnaround was the more than 17% gain in capital imports, with firms and the government bringing in heavy machinery and electrical equipment. Should imports of capital machinery sustain this influx we may see investment outlays improve in 2021 to help bolster overall GDP.

Indonesia's manufacturing sector improves as exports rebound

Jabbing their way to confidence

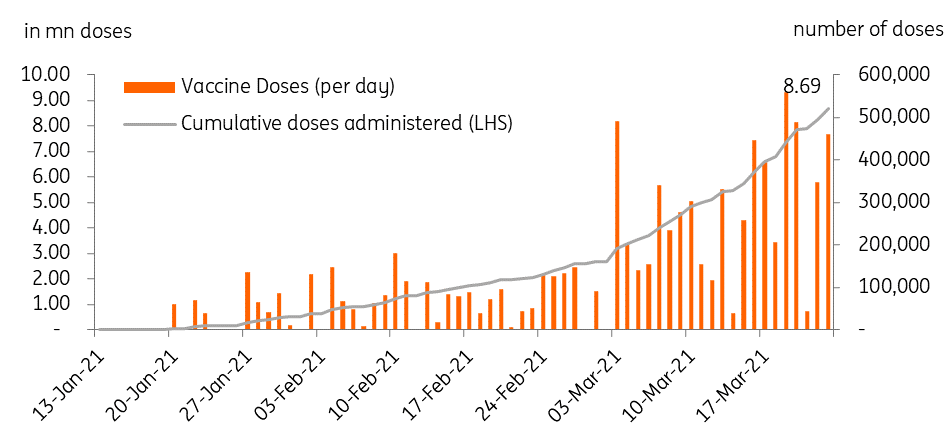

Indonesia has the highest number of Covid-19 infections in the region and new daily infections spiked at the start of 2021. Indonesia has refrained from enacting heavy-handed full lockdown measures throughout the pandemic, instead opting for partial lockdown restrictions in a bid to keep the economy open. Government officials are now betting on a relatively aggressive vaccination programme that targets inoculating roughly 180 million people over the next 15 months.

The vaccination drive kicked off on 14 January with President Jokowi vaccinated on live television in a bid to increase awareness and confidence in the process. As of 23 March, roughly 8.7 million vaccine doses have been dispensed, with the authorities hoping to quicken the pace of inoculation to build back consumer confidence and open the economy further. Consumer confidence has improved from the lows experienced in 2020 but remains well below pre-pandemic averages. A sustained vaccination effort and falling Covid-19 daily infections should help eventually bolster sentiment and in turn revitalize household spending, which comprises the bulk of economic activity in Indonesia.

Indonesia banking on vaccine rollouts to bolster confidence and the economy

Recovery delayed but not derailed

The authorities started 2021 hopeful for a quick economic recovery, banking on its vaccination programme and another round of fiscal spending to jump-start growth. A series of setbacks have forced government officials to pare their expectations, trimming official growth targets and doubling down on the size of the fiscal package.

Meanwhile, recent global developments have shifted the financial market sands with global bond yields rising sharply, a move which threatens IDR stability and limits the ability of Bank Indonesia to cut policy rates further. A short month after cutting policy rates in February, BI may have run out of space to ease further with Indonesian bond yields tracking the rise seen in global market. Yields for the 10-year Indonesian bonds have generally underperformed the region, surging by as much as 92 bps with the bond sell-off leaving IDR susceptible as foreign investors head for the exits. IDR has weakened 2.7% since 18 February, which may have forced BI Governor Warjiyo to pause at his last meeting. Warjiyo remains confident financial flows will stabilize once sentiment improves and expects IDR to appreciate “in-line with fundamentals”.

Despite these setbacks, we believe that the economic bounceback will still happen but with a delay of several months. Early signs have been encouraging, with Covid-19 daily infections trending lower while the government implements its vaccination efforts. On the economic front, manufacturing activity has picked up thanks in large part to a pickup in exports while imports finally reverted to gains. If BI can stave off pressures on the currency and maintain financial stability while the vaccination rollout continues, we will review our current 3.9% GDP forecast for the year.

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more

Included in the following bundle

Good MornING Asia - 25 March 2021

- This bundle contains 2 Articles