Indonesia to miss boost from commodity boom as Jokowi’s term winds down

- 9 January 2023

- Indonesia

Indonesia benefited from the commodity boom in 2022 but may not be able to bank on this next year

Indonesia: At a glance

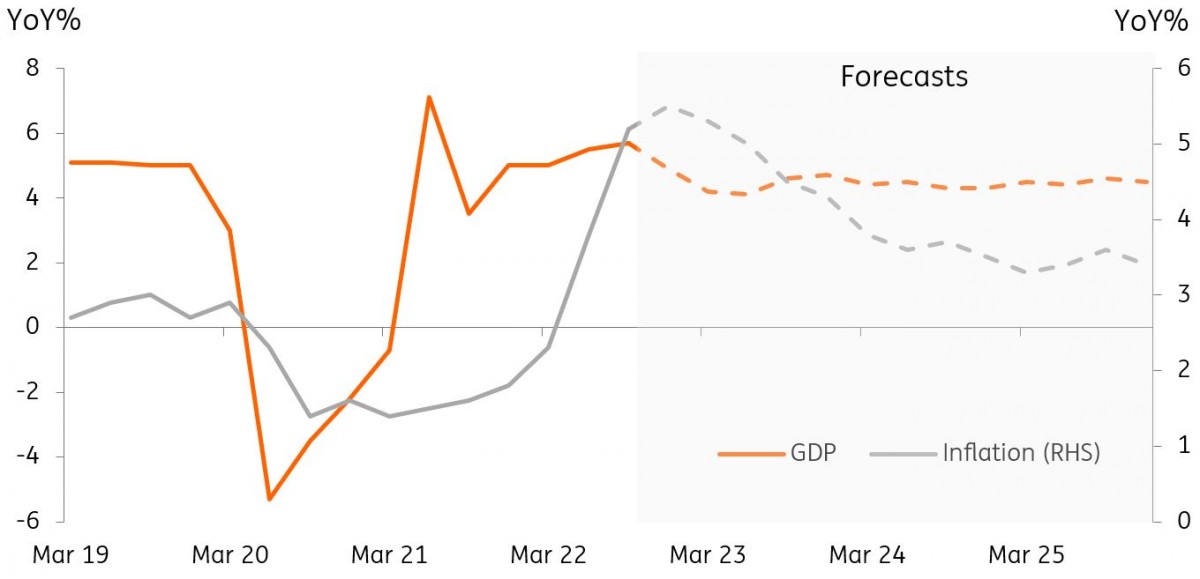

Growth in 2022 will likely average 5.3% year-on-year but momentum is slowing as the commodity boom fades and inflation accelerates. Forecasts by Bank Indonesia (BI) indicate GDP growth should settle between 4.7-5.5% YoY next year.

Household spending was one solid factor behind the growth engine due in part to relatively well-behaved domestic inflation in the first half of the year. Relatively less pronounced price pressures allowed BI the space to delay rate adjustments until the second half of 2022, which also supported growth. By the second half of the year, price pressures finally caught up with Indonesia as headline inflation breached the central bank’s upper bound target of 4%.

Indonesia’s trade sector has also seen momentum fade as commodity prices have normalised after surging due to the war in Ukraine. This development will also be worth watching in the coming months.

Growth and inflation outlook

3 Calls for 2023

Slowing trade momentum to keep FX pressured

Indonesia was one of the few countries that benefited from the commodity price boom in 2022, translating to record trade surpluses. This resulted in the current account also reverting to positive territory, which in turn provided robust support to the Indonesian rupiah (IDR). The relative stability of the IDR helped limit price pressures early in 2022 which in turn allowed the central bank to postpone rate hikes to the latter half of 2022. With commodity prices moderating and expected to slide further, we could see Indonesia’s trade surplus diminish or even move into deficit territory in 2023. The loss of this previous support suggests that the IDR will likely remain pressured for much of next year, especially if financial outflows continue. A weaker IDR in 2023 could also translate to additional rate hikes by the central bank early next year.

Tinkering with central bank charter a positive or a negative?

The Covid-19 pandemic’s impact on fiscal balances led to some central banks resorting to quasi-budget financing in addition to quantitative easing. Bank Indonesia (BI) was one of the more active central banks in terms of providing support to fiscal counterparts with BI purchasing government bonds in the primary market. This temporary scheme was termed a “burden-sharing arrangement” and was permitted via Presidential decree. BI Governor Perry Warjiyo promised to wind down such operations after the pandemic, but Indonesia’s lawmakers passed fresh legislation to make the quasi-central bank financing a permanent fixture for BI.

The use of “burden sharing” during Covid-19 raised eyebrows when first implemented but was justified given the fallout from the pandemic. The passage into law could call into question central bank independence, which in turn could cause some anxiety in the bond markets and the currency.

Jokowi’s last full year in office ahead of early 2024 election

President Joko Widodo enters his last full year in office next year as he is not eligible to take up a third term as President. Indonesia holds presidential elections in February 2024. Jokowi appears to have made a veiled endorsement for his successor by suggesting that Indonesians vote for a candidate with “white hair” and “wrinkles”. Opinion polls currently have three front runners: Central Java Governor Ganjar Pranowo, former Jakarta governor Anies Baswedan and former defence minister Prabowo Subianto.

It will be interesting to see how Jokowi spends the last 14 months of his term as he could still pass key legislation given his control over the house of representatives. Key legislative bills include the New Capital City (NCC) law and a new penal code. In particular, the NCC could positively impact growth potential as amendments could bring in a fresh round of investment given the capital-intensive requirements to move the capital from Jakarta to East Kalimantan.

Jokowi, on the other hand, may become more involved in the campaign by explicitly endorsing one of the three front runners - a move which could distract him from passing amendments to existing laws or drafting fresh legislation.

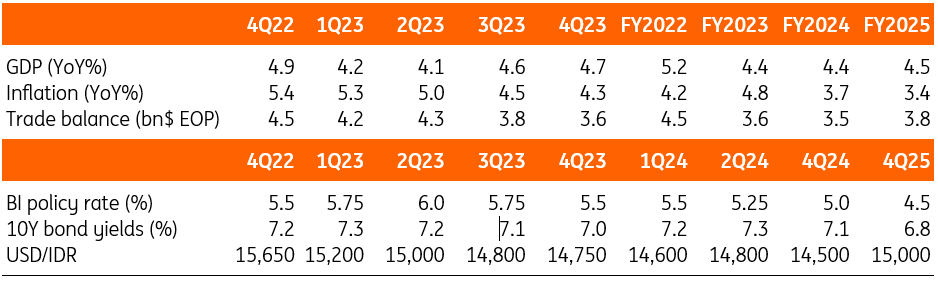

Indonesia summary forecast table

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more

Included in the following bundle

Asia Outlook 2023: Darkest before the dawn

- This bundle contains 11 Articles