India: Way forward under Prime Minister Modi

- 23 May 2019

- India

Prime Minister Modi’s General Election win puts to rest long-standing political uncertainty for markets. After a strong rally this week, profit-taking will likely be the driving theme for local markets in the face of growing economic uncertainty

| ~300 |

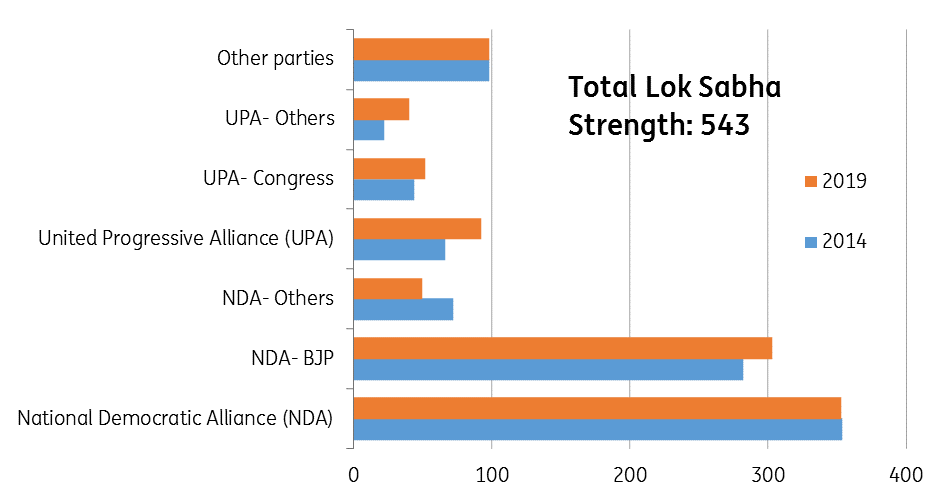

Parliamentary seats for BJP out of 543A landslide win |

| Higher than expected | |

Surprisingly strong voter mandate for Modi

Prime Minister Narendra Modi’s Bharatiya Janata Party (BJP) swept back to power, stronger than before. The vote counting yesterday kicked off with a strong, 300-seat lead for the BJP in the 543 seat Lok Sabha (lower house of parliament). The final tally due any time now, is expected to put the BJP ahead with over 300 seats, surpassing the 282-seat majority in the 2014 election and absolutely on course to form the government single-handedly. The result contrasts with the pre-election polls predicting the BJP's return with a significantly thinner margin.

The BJP retained its stronghold in the states – Gujarat, Madhya Pradesh, Rajasthan, Karnataka, and Chhattisgarh – despite its poor showing in assembly elections there. It gained some ground against dominant local parties in some other states – Assam, though failed to make in-roads in the southern states -- Kerala and Tamil Nadu. The BJP’s main rival, the Congress Party, improved on its 2014 performance slightly but is nowhere close to being a threat to the incumbents.

As things stand, close to the final results, the BJP-led National Democratic Alliance (NDA) looks set to win about 350 seats, the Congress-led United Progressive Alliance about 90, and other parties taking the remaining parliamentary seats.

Yet another landslide victory for BJP

Best of election-related market rally is behind

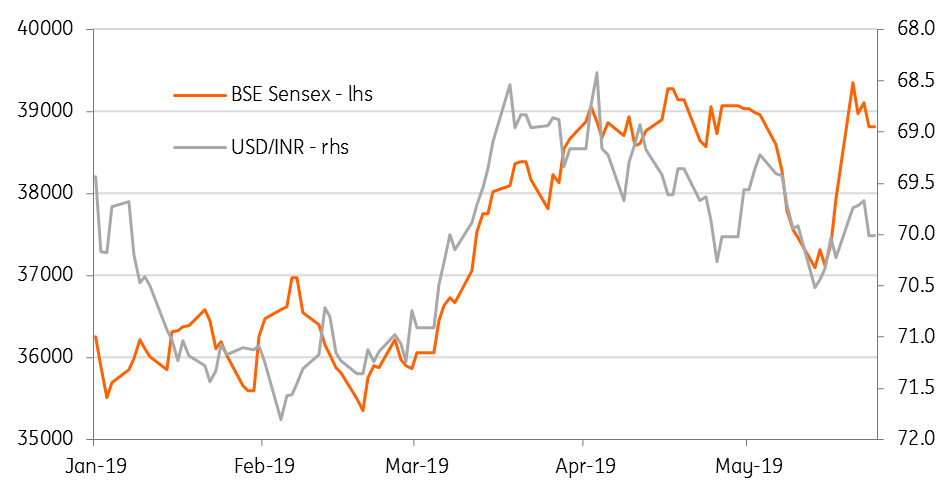

The odds of Prime Minister Modi winning the elections with an absolute majority cheered markets most of this week. We believe markets had factored in Modi’s win but not yet another landslide surge back to power.

The BJP’s strong lead right at the start of vote counting came as an added boost for markets in the early hours of trading yesterday. However, as the initial euphoria died down, the profit-taking ensued and most gains were pared off towards the end of the trading session. Pretty much the same can be expected about trading today.

We believe the best of the election rally is behind us, and the economy will be back to re-assert its influence on the markets - mainly negatively amid the prevailing risk-off sentiment globally.

Markets likely to be back in profit-taking mode

Near-term economic reality remains grim

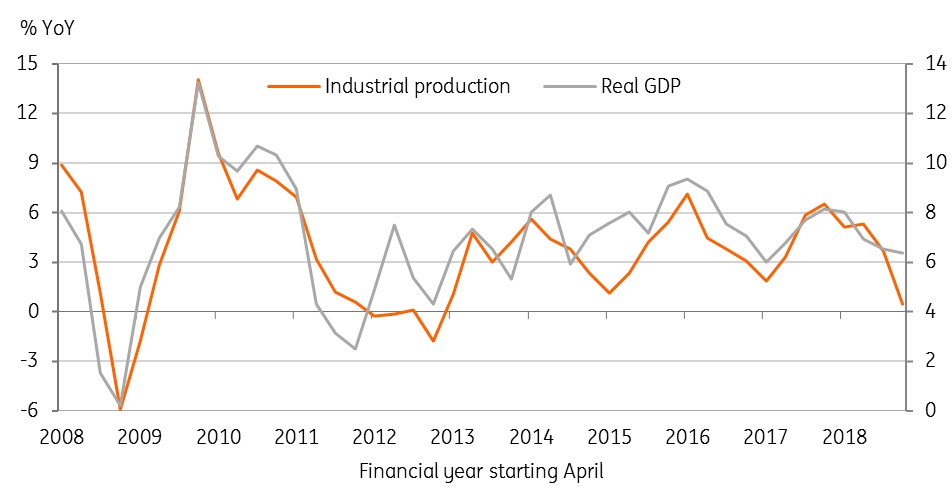

The forthcoming activity data should reinforce that despite its relatively small export base, the Indian economy isn’t fully shielded from the potential global slump stemming from the trade war.

Just as in other Asian countries, the economic slowdown here has accelerated in the final quarter of the financial year 2018-19 (ended in March), for which GDP data arrives next week (31 May). If true, our forecast of a slowdown of growth to 6.0% from 6.6% in the previous quarter will make it the slowest quarterly growth in two years. We continue to expect GDP growth staying at this level in the current quarter before the pre-election boost to government spending boosts the economy.

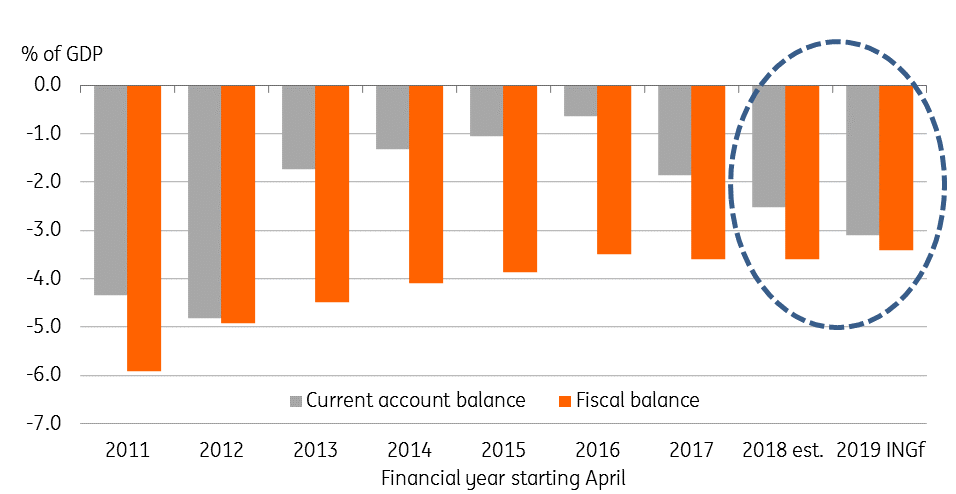

But with growing global headwinds from weak exports and higher oil prices, sustaining growth at or above 7% will be a challenge in the current financial year (ING forecast 6.8% average for the year). Adding to the cyclical economic woes are the structural bottlenecks of persistent twin deficits (the current account and budget deficit) weighing on investor sentiment.

While the cyclical growth slowdown validates the Reserve Bank of India's two rate cuts this year, we believe the risk of potentially higher inflation will keep the central bank from easing again at the next meeting in early June. With this, we consider the RBI easing cycle over for now.

Weak manufacturing, weak GDP

What to expect in Modi’s second term

The return of the Modi government assures investors of economic policy continuity in the foreseeable future. Moreover, the strong mandate reinforces voters’ confidence in the current policies. That said, this is also a chance for the government to mend discontent instilled in people by the harsh policy steps of demonetization, and alleviate concerns about the prevailing high level of unemployment.

We think the government’s focus will continue on sustaining the “Make in India” them of boosting growth. Further structural reforms towards curbing the currently wide budget and current account deficits and consolidating the beleaguered public sector banks will likely gain prominence. This is important for attracting more foreign investment, especially now that the intensified US-China trade war might accelerate supply chain re-location away from the "conflict zone". Capitalizing this fully will require further labour market reforms, easier land acquisition policies for companies and reduced red-tape.

Such a reform thrust ought to enable the Indian economy to achieve a 7-8% pace of growth. But with the likelihood that the global economic environment will continue to be marred by more and higher barriers to trade, such measures will probably only allow for GDP growth around 7%, while keeping consumer price inflation in check around 4%.

The twin-deficit - a key structural headwind to economy

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more

Included in the following bundle

What’s happening in Australia and around the world?

- This bundle contains 8 Articles