India heads into a deeper economic slump as Covid-19 crisis worsens

- 29 June 2020

- India

The accelerating spread of Covid-19 and insufficient fiscal policy stimulus prompts another downgrade to our forecast of India's GDP growth in the current fiscal year to -5.2% from -2.1% earlier

| -5.2% |

ING forecast of India's GDP growth in FY20Cut from -2.1% |

Worsening Covid-19 crisis

It’s now five months since India reported its first Covid-19 case in late January and the pandemic continues to worsen in this country. The total number of infections crossed the half-million mark over the past weekend, with daily new infections continuing to scale new heights; at about 20k confirmed cases currently. The country is now the fourth worst-affected in the world after the US, Brazil, and Russia.

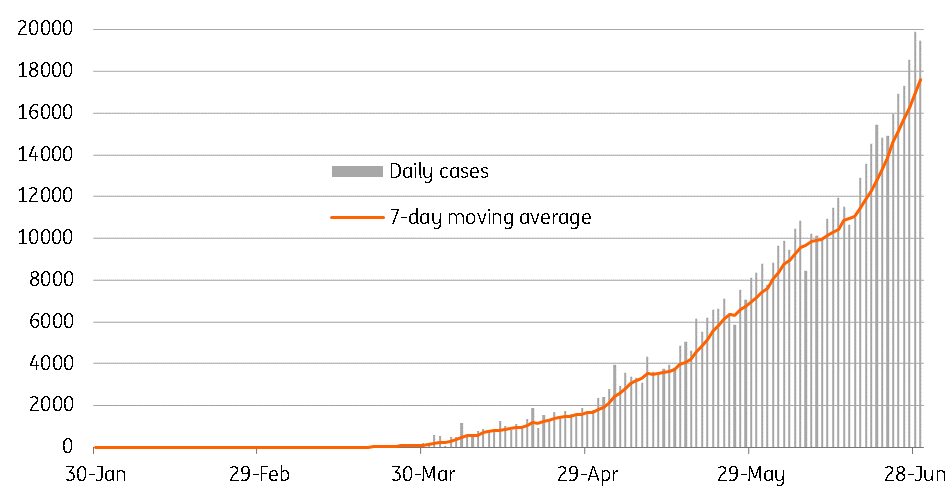

The seven-day average daily infections are currently running at 17.6k. This number has than doubled in less than a month. So has the total number of infections. There are about 16.5k deaths so far, while 58% of cases are reportedly recovered. All these figures remain debatable though, given the country’s poor healthcare infrastructure and weak testing, tracing and isolation efforts. Even so, at such a rate of contamination, it is probably only a matter of time before India moves up into third place globally for total official recorded cases, ahead of Russia.

Daily Covid-19 infections near 20k currently

Wasted lockdowns

India was among the first countries in Asia to begin a nationwide lockdown on 25 March when officially recorded cases touched 500. But lockdown implementation was chaotic; announced just hours before it started, and dragging on with four extensions from the initial three-week phase until end-June.

Despite reportedly being one of the strictest in the world, India’s lockdown has failed to break the infection chain. Undermining it was the migrant crisis – workers from largely unorganised sectors in big cities moving back to their native states, many of whom reportedly died during the journey whilst survivors carried the disease back to their home towns and villages. Large slum dwellings in cities like Mumbai became fresh breeding grounds for the virus. This is why we think the actual spread could be far worse than the reported statistics.

We believe fragmented lockdown efforts in the containment zones will be the main approach going forward as authorities are likely to resist another nationwide lockdown considering its far-reaching consequences for the broader economy.

Worst economic slump in decades

We finished a review of our forecast of India’s GDP growth in light of the accelerating spread of Covid-19, and available high-frequency economic activity data. Just like the pandemic itself, the economic fallout looks to be the worst in Asia. Nearly a whole quarter of economic inactivity in 2Q20 will mean a significant dent to GDP growth.

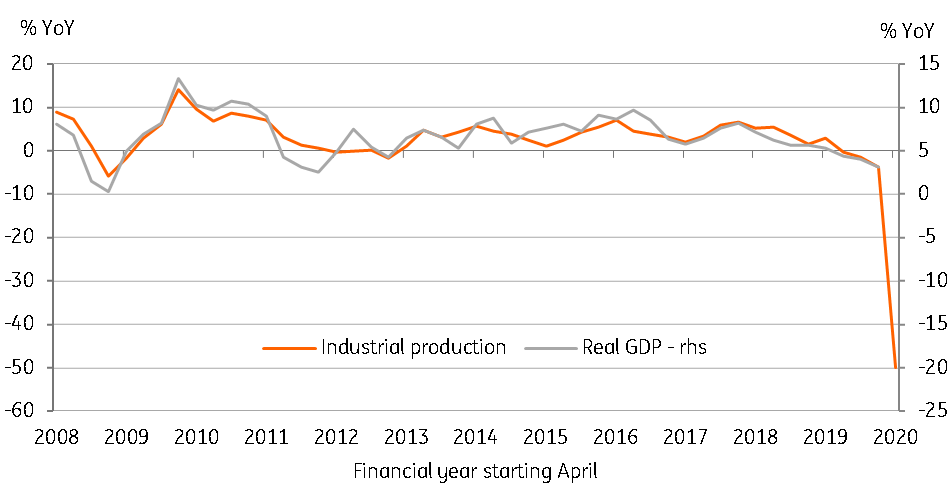

The activity data has been rather scant. The Indian statistics authority recently had to suspend releases of some economic indicators like industrial production and CPI inflation on the grounds of distortion from the lockdowns. However, the authority’s quick estimate of a 55% year-on-year fall in industrial production in April, together with a record low manufacturing PMI for May (30.8 in May), and crashing exports (-37% YoY in May after -60% in April) give a hint at the damage. So, too, does an estimate by a local think tank of over 20% unemployment.

The five most Covid-19-affected Indian states (Maharashtra, Delhi, Tamil Nadu, Gujarat and Uttar Pradesh) make up 43% of India’s GDP. Recovery here will hinge on the return of a large number of migrant workers, though not all of them are likely to be reabsorbed back into disrupted supply chains, while weak demand continues to hinder activity.

Meanwhile, high unemployment should depress spending and prices, though there are no signs of consumer price inflation abating just yet. On the contrary, resurgent food inflation resulting from supply disruption and panic buying, and high fuel prices due to recent hikes in excise duty, are pressuring inflation, keeping it near the top end of the central bank’s 2-6% policy goal.

We cut our GDP view to show a steeper contraction in 2Q20, by -11.7% against -7.6% previously. Absent a vigorous macro policy thrust, continued negative growth remains a baseline for the rest of the fiscal year (ending in March 2021). Our revised growth forecast for the current fiscal year stands at -5.2%, down from -2.1% earlier and making it the worst year for the Indian economy in five decades. There is no change to our inflation forecast for the year from 4.3%.

Where is growth heading?

Insufficient policy support

Tight public finances limit the availability of fiscal support. In May, the government unveiled a big-bang in the form of an INR 20 trillion (10% GDP equivalent) stimulus package. However, the real fiscal thrust in this was meagre, about 2.6% of GDP. The rest was fluff, including structural reforms in critical sectors. That’s helpful over the longer-term, but doesn’t provide much immediate help for the economy. Moreover, whatever little real spending was announced might not even come through given the latest reports of the government looking to rationalise its spending, as worsening public finances invite the wrath of rating agencies. Moody’s and Fitch Ratings have just downgraded the outlook on their Baa3/BBB- sovereign ratings to Negative from Stable. S&P might soon follow suit.

The Reserve Bank of India, the central bank, has been responding to the urgency of the situation though. In addition to liquidity boosting measures, the RBI has cut the policy rate by a total of 115 basis point so far this year, taking the repurchase rate to an all-time low of 4.0% and the reverse repo rate to the lowest since the 2009 global financial crisis, at 3.35%. Even as these moves have pushed real interest rates deeper into negative turf, we think the RBI easing cycle has further to go. We anticipate one more 25bp cut to the main policy rates in the third quarter.

Against such an economic and policy backdrop, the Indian rupee should continue to be one of the worst-performing emerging market currencies throughout the rest of the year. At 75.6 against the US dollar currently, the INR has depreciated 5.6% year-to-date. We continue to see further weakness to 77.4 by end-3Q20.

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more

Included in the following bundle

Good MornING Asia - 30 June 2020

- This bundle contains 4 Articles