Impact of China’s drought is small compared to its real estate crisis

- 25 August 2022

- Energy China

With so much talk of China's drought this year, we look at whether China will use more coal in the future having had such a bad experience with hydro, and what the main concern for the economy is

Nature dictates hydroelectric power supply

Heatwaves and little rainfall in some parts of China have caused drought in the southwestern Chinese province of Sichuan, which greatly relies on hydroelectric power. Sichuan also generates excess electricity and usually sends this to the east side of China, including Shanghai and Hangzhou.

Some factories in western China have been affected with limited to no power supply, shopping malls have little air-con and lighting, and some apartments have been left without a working lift. But the situation this year is much better than it was back in September 2021, when some local governments pushed for the limited use of coal fire power. We have yet to see factory suspension in key cities, which is a relief to the government as the economy is already weak. The damage caused by the drought's power supply shortage is around 1% of GDP so far. We are yet to see how the drought will affect agriculture.

Coal power is an immediate remedy, though not a perfect solution

The temporary solution is to use more coal power to supplement existing power generation capacity. This is also the reason why not many cities are rationing power. This, of course, is not a good solution as coal generates more CO2. But right now, with temperatures so high, residents need to use their air conditioners.

Another step China has taken over the past few years is embracing the use of cloud seeding, which involves adding small particles of silver iodide to clouds to spur rainfall. The success rate depends on certain weather conditions, for example, clouds need to be thick to generate enough rain after cloud seeding is performed. According to China's weather forecast, there is a chance in the coming days that the government can perform cloud seeding.

Will China rely more on coal?

The question then is whether China will rely more on coal power in the long-term if hydroelectricity is not as stable.

Instability tends to be a major characteristic of renewable energy, and China's commitment to becoming carbon neutral by 2060 is not going to change. In fact, it could now be accelerated with the drought encouraging China to push forward the technology of generating and using renewable energy.

The process of transiting from traditional energy to renewable energy is a challenge, if it were not we wouldn't have to wait until 2050-60 for the world to achieve carbon neutrality. But this challenge could provide us with opportunities.

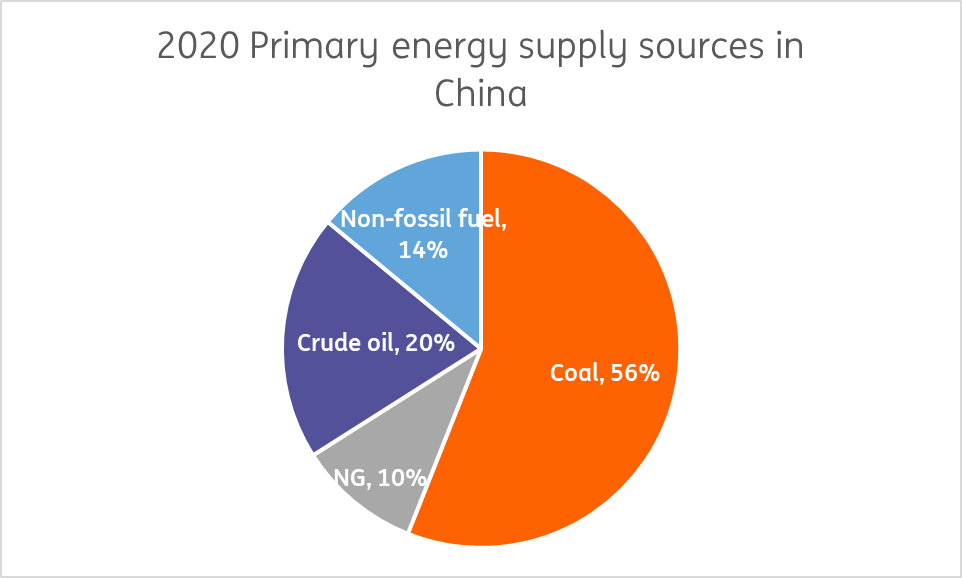

China's primary energy source in 2020

We need to go further than the installation of more solar panels

To find the opportunities we must identify the problems. Critically, achieving carbon neutrality requires more than installing more renewable energy generators, it also relies on being able to store renewable energy long enough without much loss over time. In May 2022, the Chinese government noticed this was a big opportunity to move toward using more renewable energy, as it discovered that around 12% of the power generated by wind in Inner Mongolia and 10% of solar power in Qinghai was wasted because of an issue with the electricity grid.

Foreign companies and Chinese companies will invest in this technology, but there is a risk that the technology race between China and the US may make climate change cooperation, in particular in research and development, more difficult.

For the Chinese economy, construction activities are key to growth

The most worrisome aspect of the Chinese economy is the deleveraging reform on residential property developers. Interest rate cuts only lift home buying sentiment a bit. Potential home buyers are watching to see whether uncompleted homes can be finished quickly and to a good quality. This takes time – at least a couple of quarters. Between now and then, even though there are supportive policies in place – a lower down payment ratio, lower mortgage rates, and lifting the second-home buying restrictions – it will only become attractive when there are projects that are 100% complete and managed by high-quality management companies, which are usually subsidiaries of property developers. Only after home buying activities pick up will more residential properties kick off construction.

The government can speed up infrastructure, and indeed it has. But the gap left by residential construction activities is getting bigger as more sites are holding off construction.

On 24 August, the central government offered another stimulus package, worth around 1% of GDP – similar to the economic damage caused by the drought so far. From the tone of the statement, it seems that the key point is not just the additional stimulus but the urgent tone directed toward local governments to act swiftly and efficiently. This is an important message to all local government officials as we approach the 20th National Congress of the Chinese Communist Party in October. Local government officials will have to be hands-on to create growth and jobs.

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more