Hungary’s bond issuance needs under control

- 17 April 2023

- Hungary

Fiscal policy is a manageable risk this year. Gross borrowing needs remain high due to the high volume of bond redemptions. However, net issuance of HGBs is the lowest since 2019. AKK has secured 24% of planned issuance and is slightly behind the region. In contrast, FX and retail issuance improves the picture. The share of foreign holders is increasing

Fiscal policy: Improvement in the second half of the year

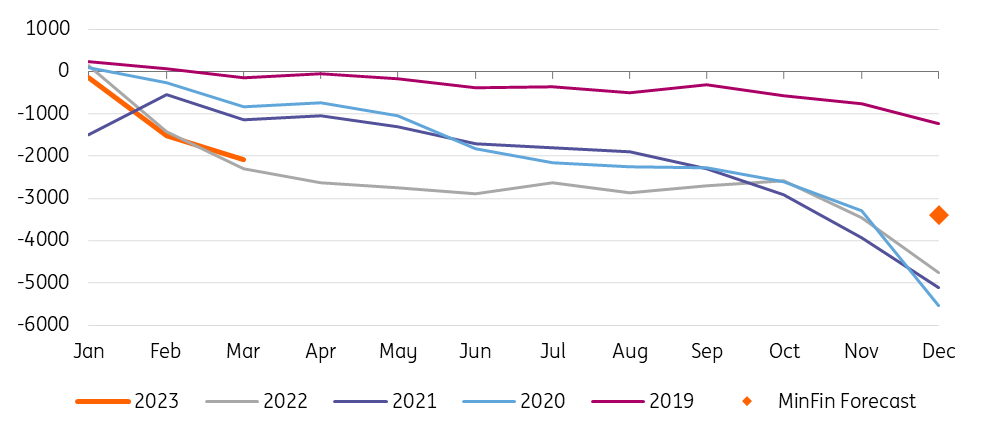

The first three months of this year generated a deficit of HUF2,090bn, equivalent to roughly 61% of the full-year target. The deficit accumulation used to be frontloaded, which makes this year's picture bleaker as the Hungarian economy probably hit bottom in the mini-crisis at the beginning of 2023. This makes revenue generation more challenging, although high inflation does compensate for this somewhat. Moreover, as the Ministry of Finance pointed out, expenditures increased by 12% year-on-year during the first three months of this year. This is a result of the budget being used to compensate energy suppliers during the heating season, and the heating season was more costly than last year’s. On top of this, the significant increase in pensions, complemented by the extra pension payments, was an added burden to the budget during the first quarter. With the heating season over, we see some improvement in the budget situation in the coming months. The government has maintained a freeze on public investment activity as well, which could also help to meet this year’s deficit target of HUF3,400bn.

On the EU side, our base case scenario is that the government will settle the dispute and money will start flowing during the second half of this year. With that in mind, we think the deficit target will be met. The Ministry of Finance has underscored this as well; that the government will make every necessary step to meet this year’s deficit target.

State budget development and 2023 forecast (HUFbn)

High gross borrowing needs but lowest net issuance since 2019

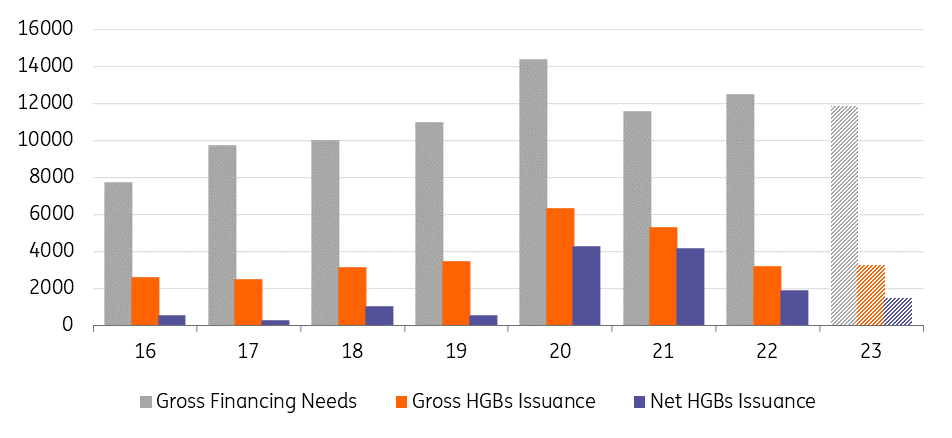

Hungary’s Debt Management Agency (AKK) projects gross borrowing needs of HUF11,869bn (63.5% of GDP) for this year, which is 4.9% less than last year, assuming that the planned state budget deficit is met. Although the projected state budget deficit is 28.5% lower year-on-year, borrowing needs are kept elevated mainly by the high redemptions this year, which is significantly higher compared to the previous two years. Thus, we expect gross issuance of Hungarian government bonds (HGBs) to reach HUF3,262bn, 2.5% higher than in the previous year but still significantly lower than in 2020 and 2021. On the other hand, due to high redemptions, we estimate net issuance of HGBs of only HUF1,479bn, the lowest since 2019. On the FX side, this year's redemptions amount to EUR2bn of which EUR1.6bn is Eurobond repayment, EUR0.1bn domestic bond repayment and EUR0.3bn repayment of loans from supranational institutions. FX needs should be covered through EUR5.0bn Eurobond issuance with a preference for USD-denominated bonds, EUR2.2bn through loans from supranational institutions (EIB, CEB, AIIB, etc.) and other sources.

Total financing needs and HGBs issuance (HUFbn)

Slower issuance compared to CEE peers but still a comfortable picture

AKK, like its regional peers, took advantage of strong market demand at the beginning of the year to frontload supply in the local market. Year-to-date, we estimate AKK has secured 24.3% of its planned HGBs issuance (including switches). That's not a bad result in mid-April but it is at the same time the lowest number in the CEE region by our calculations. On the other hand, AKK has been very active in FX issuance, where it basically already met this year's plan (103.8% including switches) in March. In addition, the debt management agency is again very active on the retail bond side. According to our calculations, it has already covered 40.8% of the plan for this year, which is the main source of funding for this year. If the risk of a higher state budget deficit materialises, we assume that the additional needs would be covered through the issuance of retail bonds.

| 24% |

Issued HGBs vs ING estimate for this year |

Looking ahead, we can expect AKK to continue its strong retail bond supply. For the second quarter, the agency plans to issue HUF710bn of HGBs, roughly the same as in the first quarter. In addition, AKK has issued a relatively high volume of T-bills maturing in the second half of the year, pushing HGB issuance more into the second half of the year depending on the state budget developments. In addition, it can be assumed that there should be better funding conditions in the markets later, supporting AKK's issuance strategy.

Financing needs for 2023 (HUFbn)

FX issuance plan met, pre-financing in second half of year is possible

On the FX issuance side, since this year's plan has already been filled, AKK is not obliged to issue any more Eurobonds. As with many CEE peers, the strong front-loading of Eurobond issuance needs for the year should act as a postive techinal tailwind in the near term for dollar bond performance. In this respect, Hungary is in a slightly more comfortable position than Romania (which likely needs one more Eurobond issuance to meet its FX financing plan), while not quite as strong as Poland (which is already well ahead of schedule). On the other hand, the head of the agency does not rule out more issuance in the second half of the year as a pre-financing for next year. We assume that in this case, the AKK would prefer a euro-denominated issue, while for both Hungary and the region as a whole, interest has picked up in recent years in more unconventional international bond issuance (such as green bonds, and those denominated in Chinese yuan or Japanese yen). At the same time, developments in the EU story and Hungary's access to EU money will also play a big role.

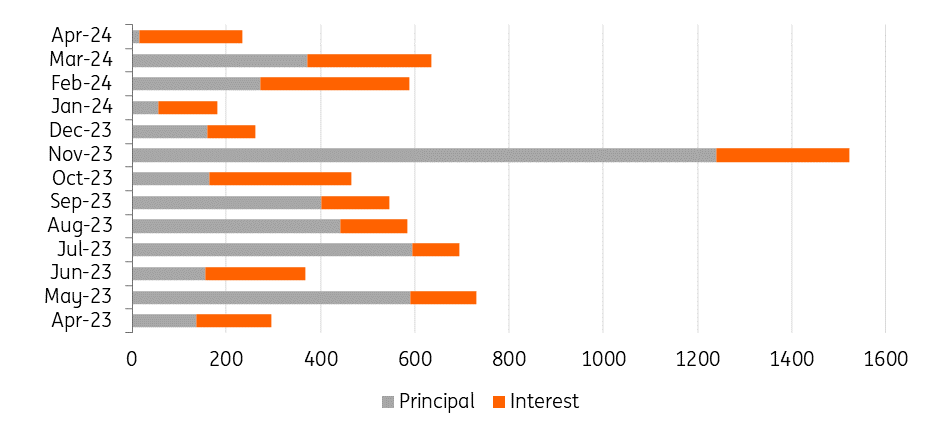

HGBs maturity calendar (HUFbn)

Technicals: Highest share of foreign holders in the CEE region

After dodging an outright downgrade last year, this time S&P changed Hungary’s credit rating from “BBB” to “BBB-“ with a stable outlook in early 2023. Markets do not seem to be bothered by either S&P’s downgrade or Fitch’s change in outlook from stable to negative while keeping the "BBB" rating in January. Moody's decided to skip its review yet again, keeping Hungary at "Baa2" with a stable outlook. The market's behaviour perhaps reflects a perception that rating agencies are looking in the rear-view mirror too much and uncertainties are blurring the big picture, while current valuations for Hungary's dollar bond spreads are at similar levels to Romania, already implying a "BBB-" rating. The factors that have the highest weight in rating decisions have remained the same: the fate of the EU deal and economic policies. Regarding the former, we remain optimistic about a final deal being struck between the EU and the government. Peaking CPI, a rebound in growth and improving external balances alongside EU funds flow might lead to a pivot in rating reviews as the end of the year approaches.

In the GBI-EM space, HGBs have already seen some changes and more can probably be expected in the rest of the year. HGB 1.50/23 was removed in January and we expect 6.00/23 to be removed in April due to the short maturity. In terms of HGBs inclusion, only three eligible bonds are not included at the moment (9.50/26, 4.50/32, 4.00/51). Given the current even composition in all maturity buckets, we only see a chance for a 9.50/26 to be added this year to replace the 1.50/26 in the 3-5y bucket.

In terms of bondholders, the first quarter of this year reversed a long-term trend of declining foreign holdings in relative terms. During January, the share of foreign HGB holders jumped from 21.3% to 27.6% and in April it exceeded 28%, returning to the levels seen in the first half of 2020 and at the same time, the highest in the CEE region at the moment, overtaking the Czech Republic as the leader.

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more