Hungarian industry struggles, but retail sales improve at the end of 2023

The industrial sector again disappointed at the end of the fourth quarter, while retail sales improved across the board. Looking ahead, we expect this momentum to remain broadly intact in the near future

The Hungarian Central Statistical Office (HCSO) released the December figures for the industrial and retail sectors. Industry delivered yet another dismal performance with the third consecutive month-on-month (MoM) contraction. At the same time, retail sales have improved in all major categories, helped by a rise in consumer confidence and positive real wage growth.

Export sectors disappoint yet again

| -8.7% |

Industrial production (YoY, wda)ING estimate: -8.6% / Previous: -5.3% |

| Worse than expected | |

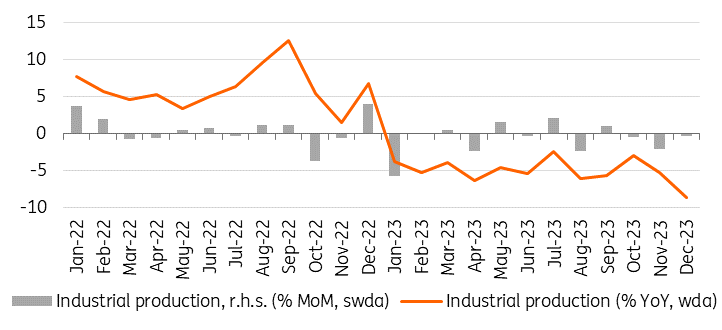

Industrial production in December was well below expectations, as output was 8.7% lower than a year earlier on a calendar-adjusted basis. If we look at the raw figure, the drop is even more surprising with a 13.7% year-on-year (YoY) decrease in production, but this is due to two less working days in December 2023 than in December 2022. However, the monthly dynamics suggest that industry was still struggling at the end of the fourth quarter, as output fell by 0.3% MoM.

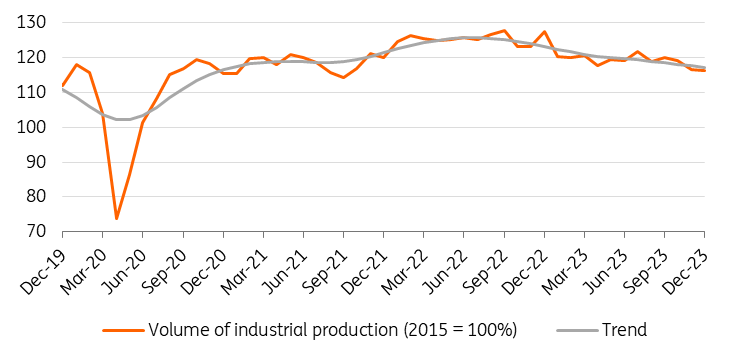

This was the third consecutive month in which output contracted on a month-on-month basis, casting some doubt on the extent of the economic recovery. It seems that even though the economy moved out of technical recession, industry is unable to take the lead in the economic recovery, in contrast with what history shows. The sector is still on a downward trend and total production has fallen back to the post-Covid crisis levels recorded at the end of 2020 and the beginning of 2021.

Volume of industrial production

Detailed data have yet to be published, but the preliminary release by the HCSO contained some surprises, similar to the November release. For the second time in 2023, the two most influential sectors (electrical equipment and automotives) were not highlighted as positive contributors.

Instead, the statement indicated that output grew in only three sub-sectors, with the highest rate in the manufacture of coke and refined petroleum products. This suggests that the other two sectors are likely to be underweighted in terms of contributions to overall output. In our view, as both sectors (manufacture of electrical equipment and automotive) are heavily reliant on export sales, we suspect that December was characterised by subdued external demand.

Performance of Hungarian industry

This was the second data in a row, which increases the chances that the process we have been predicting for months has begun: the effects of the weak global industrial performance may have arrived in Hungary and, as a result, the output of export-orientated sectors may have started to weaken. Meanwhile, industrial sectors producing for the domestic market are unable to amass new orders and ramp up production in the absence of domestic demand, as consumption and investment dynamics still remain subdued.

Regarding external demand, the outlook does not look rosy if we take a look at the state of the Chinese economy or look to Western Europe. Germany is Hungary’s biggest trading partner by far, therefore the downward trend of the German industrial production is not a good sign for the Hungarian counterpart.

In addition to weakening external demand, which is having a negative impact on new export orders, the crisis in the Red Sea region is also weighing on the situation. Several shipping companies have already suspended shipments on the Red Sea routes due to the ongoing Houthi attacks. The result of trade diversion is reduced transport capacity, longer transit times by sea and a dramatic increase in shipping costs.

The impact of the Red Sea conflict on supply chains is already being felt as Suzuki halted production of the Vitara and S-Cross models at its Esztergom, Hungary plant between 15 and 22 January. The shutdown was caused by delays in the delivery of Japanese engines. So, the outlook for January looks even more bleak.

What else hinges on the Red Sea conflict?

Up until now the increase in shipping costs has had the greatest impact on spot buyers, particularly those using a just-in-time (JIT) inventory management strategy. As the majority of large-scale traffic is done under longer-term contracts, the increase in spot rates hasn't yet affected all types of cargo.

These longer-term contracts are usually signed in April or May, but this year it will probably be closer to May. This means that if we don't see any de-escalation until April or May, then we will see an increasing proportion of contracts being rolled up significantly, resulting in double or triple the cost of shipping for the following year.

This is a major factor that poses an upside risk to inflation not only in Hungary but globally. However, even if we were to see a tripling of contract rates, we are unlikely to see a reversal of the inflation dynamic in 2021. The reason is that at that time we had such a constellation of supply and demand imbalances that paved the way for significant inflationary pressures, which is not the case in 2024.

In 2023 the volume of industrial production was 5.5% lower compared to 2022, with the sector ending the year with a disappointing performance. In this regard, the volume of production in the fourth quarter of last year contracted by around 2.2% quarter-on-quarter (QoQ), which means that industry was a drag on growth late in 2023.

Retail sales performed well in the fourth quarter

| -0.2% |

Volume of retail sales (YoY, wda)ING estimate: -1.2% / Previous: -5.4% |

| Better than expected | |

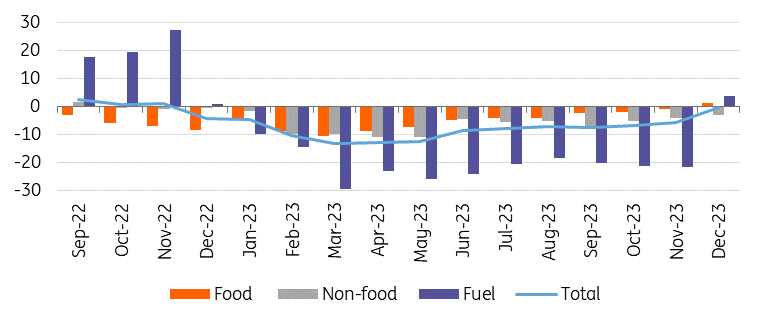

Retail sales delivered a positive surprise in December, as the volume of retail sales rose by 1.4% on a monthly basis and adjusted for seasonal and working-day effects, the highest increase since March 2022. This has contributed to a significant improvement in the year-on-year index, with retail sales now only 0.2% lower than a year earlier.

Breakdown of retail sales (% YoY, wda)

Looking at the details, the volume of food sales rose by 0.3% MoM in December, therefore the year-on-year index ended 2023 with a positive figure of 1.3%. This year-on-year improvement is mainly explained by the fact that food disinflation has been particularly strong. Food prices disinflated from 44.8% YoY in December 2022 to 4.8% YoY in December 2023, which contributed to the slow and gradual improvement in food retailing.

What’s even more, volume of non-food retailing increased by 0.4% MoM, which is the third consecutive monthly increase, bringing the year-on-year index up to -3%. In our view, Christmas sales clearly have played a role in this, as we can highlight typical year-end shopping patterns. The sale of cosmetics articles jumped by 4.2% MoM, while the computer equipment and other sub-category saw a 3% MoM increase in purchases.

Finally, there was also an impressive 4% MoM increase in fuel sales, which was the largest increase since March 2022. In our view, the reason for this large increase can be attributed to customers anticipating the upcoming significant excise duty increase from January 2024. As the fuel price cap was lifted in December 2022, this is the first data, where the base is not kept artificially high, therefore the year-on-year index improved to 3.8%.

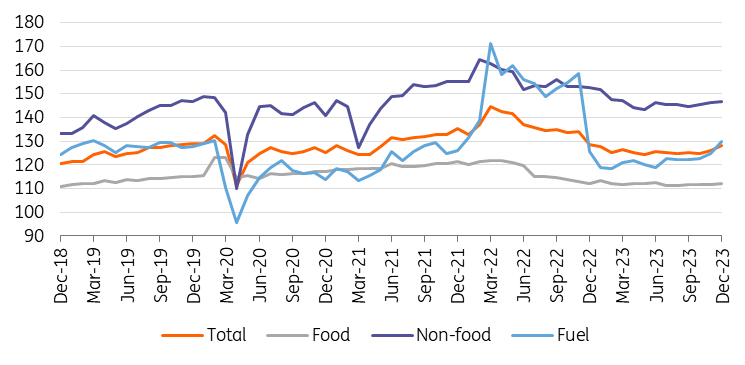

Retail sales volume in detail (2015 = 100%)

Overall, we have seen a gradual improvement across all major segments of the retail sales report, which is a good sign in terms of economic recovery. However, we would highlight that these two good reports came at the end of 2023, with Black Friday and Christmas sales potentially improving the numbers more than we would have otherwise seen.

Nevertheless, we continue to expect a gradual improvement in consumption dynamics throughout 2024, fuelled by positive real wage growth. In this regard, gradually increasing consumer confidence is one of the pillars of the economic recovery, which we expect to increase as we are getting deeper into 2024.

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. Read more

Download

Download article