How demographics will reshape the German housing market

- 29 April

- Real estate Germany

Demographic change will not trigger a nationwide fire sale in residential property. But it is likely to leave Germany with a more fragmented housing market, where shortages and vacancies increasingly exist side-by-side

Germany’s demographic problem is well documented. An ageing society, falling birth rates and a shrinking workforce will weigh on growth and prosperity in the years ahead. According to the German Statistical Office, Germany’s population is expected to decline by around 2.5 million people by 2040, while the working-age population could shrink by more than 5 million, or 10%. The housing market will feel the impact too. But fewer people does not automatically mean less housing demand.

The key reason is shrinking household size. Over the past 25 years, the number of one and two-person households has risen by around 20%, while larger households have become less common. As a result, the number of households has continued to grow despite weak population dynamics, increasing from around 37 million in 2000 to more than 41 million in 2025.

According to the German Statistical Office, this trend looks set to continue. Over the next 15 years, one and two-person households are expected to increase by another 1.2 million, while larger households will decline by around 750,000. In total, the number of households is likely to remain broadly stable and may even rise slightly. As a result, demographic change is unlikely to reduce housing demand in quantitative terms. What it will change is the type of housing needed – and where it is needed.

All the wrong homes in all the wrong places

Germany’s housing problem is increasingly not about the total number of homes. It is about mismatches. Households are getting smaller, while living space per person continues to rise. Demand is shifting in size, quality and location. Housing may still exist, but increasingly not in the way people need or in the places where demand is strongest.

Germany is therefore not heading towards a broad housing surplus, but a more fragmented housing market in which shortages and vacancies exist side-by-side.

The regional divide is already visible

Too little housing here, too little demand there. That split is already visible. Overcrowding remains mainly an urban phenomenon: around 17% of city households live in homes that are too small, compared with just 5% in rural areas.

At the same time, under-occupation is especially widespread outside cities. Every second rural household effectively has more space than it needs. This is particularly common among older homeowners who continue to live in homes that have become too large for them. Combined with low mobility and weaker local economies, this increasingly creates vacancy risks in ageing regions.

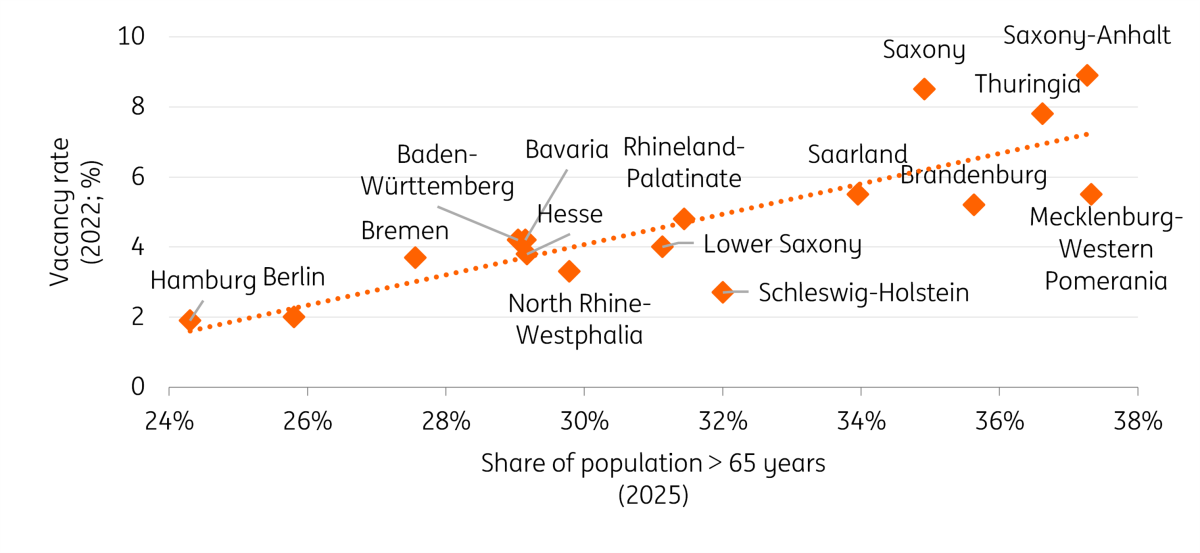

The regional divide is also reflected across German federal states. While states such as Mecklenburg-Western Pomerania and Saxony-Anhalt have ageing populations and vacancy rates of between 5% and 9%, younger city states such as Hamburg and Berlin have vacancy rates below 2%. In other words, younger regions are struggling with housing shortages, while older regions are facing weakening demand.

Vacancy rate and share of the population aged 65 and over

A healthy vacancy rate is typically seen as between 2% and 4%. In Germany, only a few states fall within that range. In the rest, the market is either overheated or structurally weak. That leaves Germany with two very different housing problems: too little housing in areas with high demand, and too little demand in areas with existing housing.

Two paths to 2040

Looking ahead, we see two possible scenarios for the German housing market as demographic change continues. The more optimistic one is that rising prices and worsening affordability in cities push more households to relocate to rural areas. That could reduce pressure in urban markets while absorbing some vacancies elsewhere. For some households, moving out of the city may become the only realistic route to homeownership.

One argument pointing in this direction is that population growth in cities has been driven mainly by international migration in recent years, while domestic migration balances have already turned negative.

The more likely scenario, however, is a different one. For many households, location is still the key selling point. In our consumer survey, the share of renters under 65 who said they could afford to buy a home – just not in their preferred neighbourhood, city or region – rose from 6% in 2023 to 9% in 2025.

If that trend continues, younger households will remain concentrated in cities, while ageing and structurally weaker regions will see vacancies rise further. The result would be falling prices in some rural markets and even tighter housing shortages in urban areas.

No fire sale, but more fragmentation

By 2040, Germany may no longer have one housing market, but many: shortages in some places, vacancies in others. Demographic change will not create a nationwide glut of homes, but it will widen the gap between where people want to live and the available housing.

For the housing market, the real demographic risk is not depopulation. It is the growing mismatch between where people want to live, what they can afford, and what is available. Germany is not heading towards one housing crisis. It is heading towards many, simultaneously.

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more