How Covid-19 has impacted Eurozone bank lending and deposits

- 29 June 2020

Since lockdowns started in March, Eurozone banks have lent an additional €165bn to businesses and households, which in turn saw their deposits rise by €400bn. France and Spain have seen the biggest spikes, but Germany and the Netherlands, not so much. Now, as lockdowns ease and economic activity picks up, attention now turns towards the issue of solvency

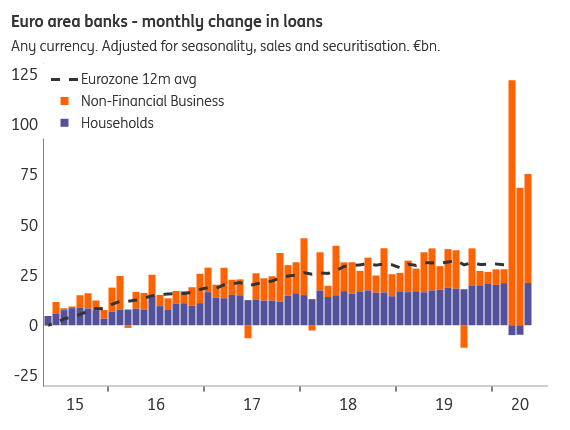

Eurozone businesses borrow heavily at banks...

In May, Eurozone banks lent another €75bn to Eurozone households and businesses in net terms (after deducting repayments), according to the latest ECB monetary data. This compares to a pre-corona trend of about €30bn a month. After a pause in March and April, household borrowing moved back to its pre-corona trend in May. Businesses borrowed massively, €120bn net in March alone, falling to a still respectable €54bn in May. Lending during the lockdown was spurred by government guarantee schemes that were quickly put in place.

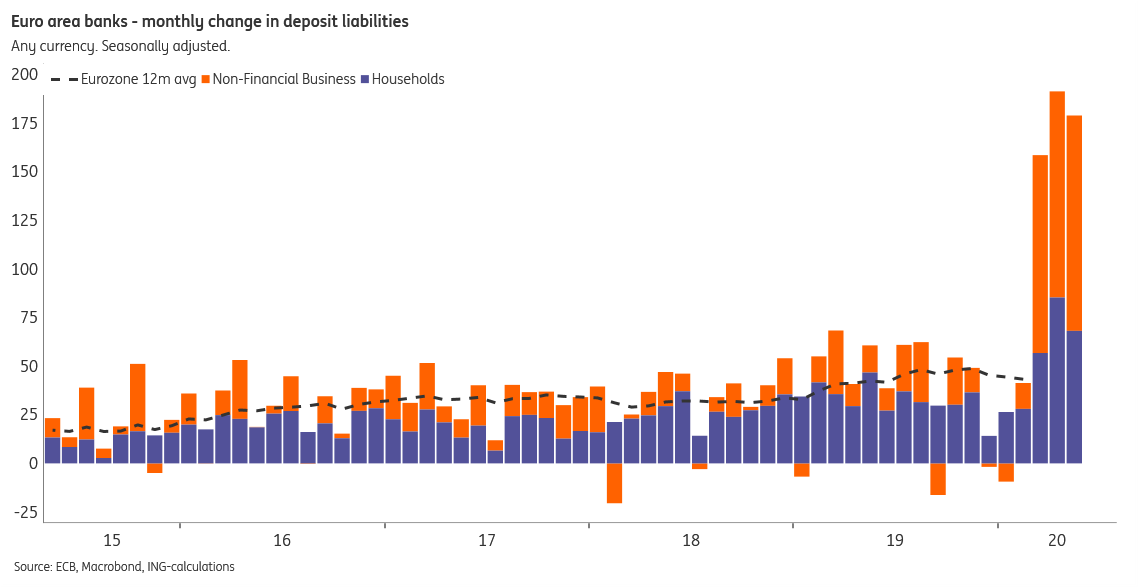

...driving around half of an ever bigger jump in deposits

From a monetary perspective, increased bank lending has to result in higher bank deposits -- just not necessarily by the same party or at the same bank.

Businesses draw liquidity from bank loans, but also from government support and tax deferrals. Part of this liquidity is hoarded on deposit. But part of it is transferred to households, in the form of wage payments. Households also receive direct government support. Their deposits also grew as they reduced their spending.

Before the crisis, Eurozone bank deposits increased by about €45bn per month but since March, this has jumped to well over €150bn/month. In cumulative terms, businesses and households deposits had increased by €400bn more than "normal", by the end of May. And while money in the bank may sound good, these funds mostly reflect liquidity hoarding, activities not undertaken and products not purchased.

But there is also a more positive way to look at these deposit stats. The main aim of governments, going into lockdown, was to avoid a liquidity squeeze for businesses and households. All measures, ranging from tax deferrals to government loan guarantee schemes, unemployment scheme extensions, income support and direct grants, were a means to this end. From a top-down perspective, the massive increase in deposits show that government support measures had substantial effects. At the Eurozone level, just under 50% of the deposit increase can be traced back to bank lending (in turn made possible by government guarantees); the remainder comes from other sources. It is safe to assume that direct government liquidity support is the main driver there.

France and Spain have seen the biggest spikes

The Eurozone loan and deposit totals hide important differences between sectors, big and small companies, employees and the self-employed. Whether government support managed to reach all intended recipients cannot be deduced from these top-down data.

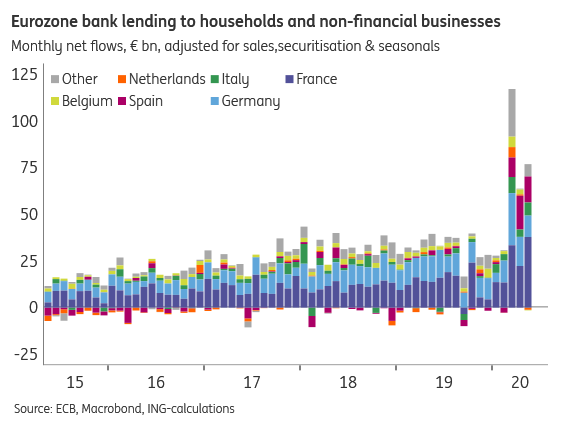

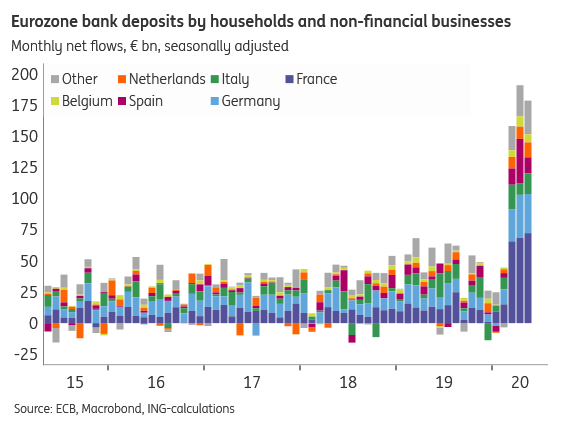

France and Spain saw big spikes in bank lending and deposits, but in contrast, Germany and the Netherlands net bank lending did not increase by much

The data does shed light on the distribution of bank lending and deposits over the Eurozone. Most bank lending took place in France -- in fact, France drove half of the Eurozone total in May. This is slightly less surprising when realising that already pre-corona, French bank lending was a strong contributor to the Eurozone total.

Spain also saw strong bank lending boost, coming from virtually zero net bank lending growth pre-corona. On the other hand, Germany and the Netherland's net bank lending did not increase by much, compared to their respective pre-corona trends.

A similar picture emerges for bank deposits -- though here too it becomes apparent that businesses and households have other sources of liquidity to draw on other than bank loans alone.

From liquidity to solvency

As lockdown measures ease, economic activity will slowly pick up. In the banking system, we will likely see a deceleration of lending and deposit growth in the months ahead.

While some businesses may decide to reduce their borrowing, we don't expect loans and deposits to drop back to their pre-corona levels soon.

Neither banks, nor borrowers, nor governments have an interest in reducing liquidity too quickly. But with the urgent issue of liquidity addressed, and absent a "second wave", attention will now slowly turn towards the less urgent but more important issue of solvency.

While banks were able to help provide liquidity, they do not have instruments available to repair their clients' solvency. The only upside for policymakers is that where liquidity needed to be provided in a matter of days or weeks at most, the time horizon for addressing solvency is a bit longer.

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more