FX: As the Fed tightens, the dollar rally has some way to run

- 4 February 2022

- FX

The dollar is near its cyclical highs as the Fed prepares to embark on a tightening cycle. Has all the good news been priced into the dollar and how will central bank balance sheet adjustments hit FX markets? We continue to think that the Fed terminal rate is prone to being re-priced higher over the coming months and that the dollar rally has some further to run

Dollar's rally hits the hard yards

We have seen some commentators recently suggesting that the start of the Fed tightening cycle is normally associated with a top in the dollar. The rationale seems to be along the lines of ‘buy the rumour, sell the fact’. Or in other words that FX markets – largely driven by the expectations channel – have all the good news of tighter policy already priced into the dollar by the time the Fed's hiking cycle begins.

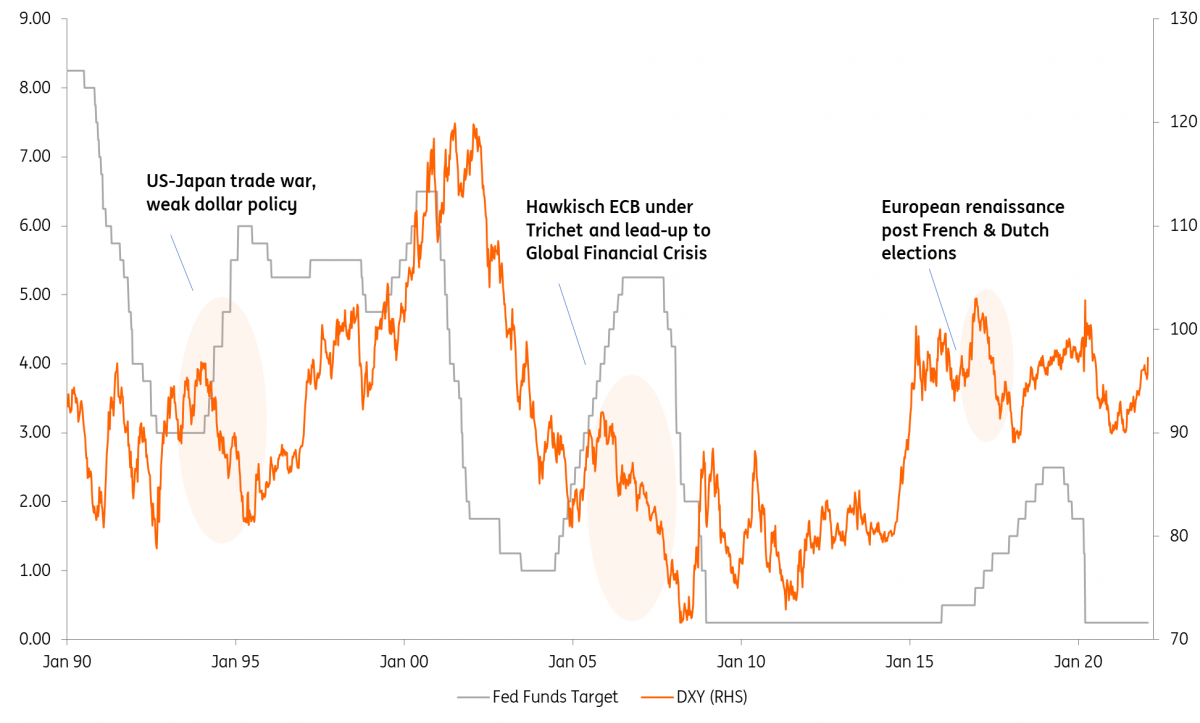

We've outlined a stylised chart of Fed tightening cycles since 1990 marked against the DXY – a trade-weighted measure of the dollar heavily weighted towards European currencies, and you can see that below. One can probably make out around four tightening cycles during that period. Using a broad brush, most cycles have been associated with some periods of dollar strength – as one would expect with a central bank welcoming tighter monetary conditions.

Fed tightening cycles and the dollar

But periods of exceptions – as you can see in 1994, but also in 2006 and 2017 – were very much driven both by US policy choice and developments overseas. In 1994 the dollar was under broad-based pressure as the new Clinton administration fought a trade war with Japan. Dollar under-performance of the Fed tightening cycle in 2006 was a function of the take-off in the ECB policy rate under hawkish President Trichet. In 2017, DXY weakness was again driven by a re-assessment of the euro’s prospects following the Dutch and French elections.

What of the Fed tightening cycle in 2022? We doubt the Fed cycle’s positive effects on the dollar will be undermined by domestic US policy. Here the White House, like many administrations around the world, will increasingly favour a strong currency to keep inflation in check and to protect real incomes. A re-assessment of European growth prospects and a hawkish ECB would be a threat to a strong dollar story. After this month's hawkish ECB press conference, this threat seems a little more real. Yet we would argue that a very aggressive Fed tightening cycle - including five hikes in 2022 - can see the dollar largely hold onto gains. In particular, the Fed terminal rate is currently priced near 1.60/70% and could well be priced closer to 2.50% as 2022 progresses.

Clash of the balance sheets

A further challenge to FX markets in 2022 is how to understand the role of central bank balance sheets. For example, does a quicker reduction in the Fed’s over the ECB’s balance sheet have any implications for EUR/USD?

We take our lead on this from this research piece produced by then ECB Council Member, Benoit Coeure, in 2017. The article looked at the FX impact from QE. Our take from this was that QE did indeed drive international portfolio choices, especially fixed-income choices. But linking those international fixed-income allocations with currency moves was near impossible.

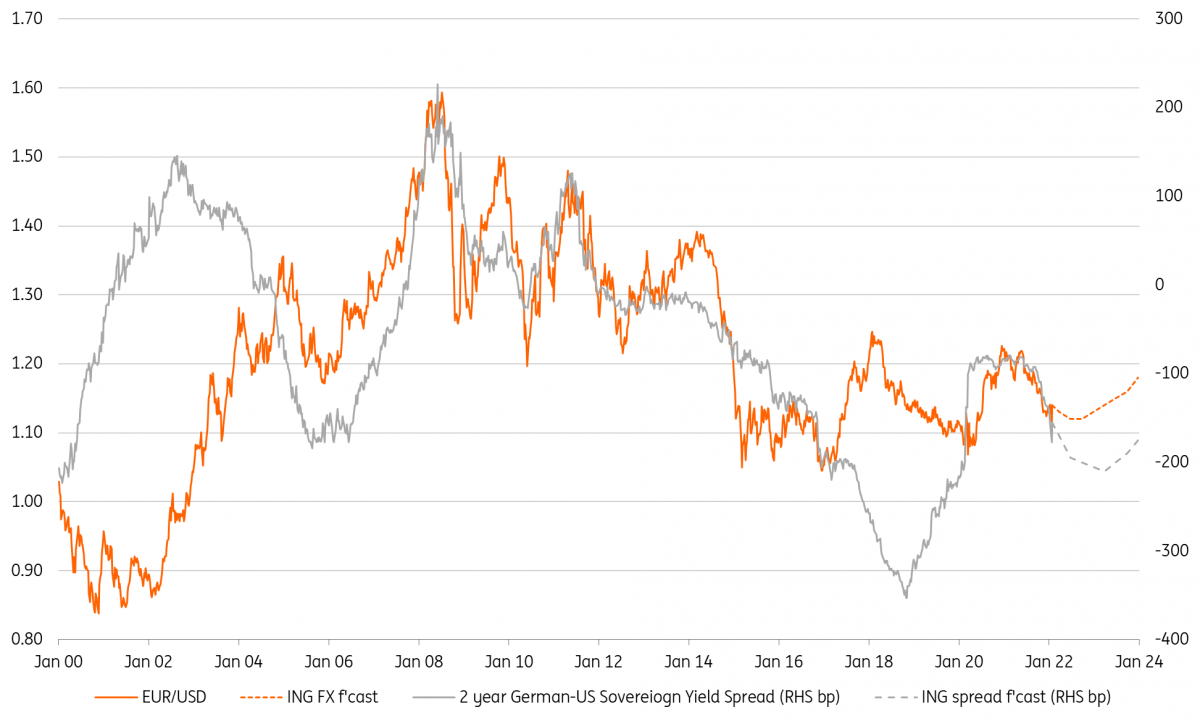

The ECB’s QE programmes have played a major role in driving the eurozone’s basic balance (its net current account, net foreign direct investment and net portfolio flows summed) into deeply negative territory. The biggest driver of the negative basic balance is fixed income flows, where ECB QE has driven both eurozone residents and foreigners out of eurozone fixed income. This large negative basic balance leaves the euro vulnerable.

But as the 2017 report concluded, short-term interest rate differentials, capturing expectations of policy rates, have a much bigger say as to where FX rates are headed. Based on our team’s forecast yield spreads between German and US sovereign bonds, we expect EUR/USD to stay under pressure in the first half of the year. However, a sustained move below 1.10 looks too much of a stretch now because of the hawkish ECB. And we are revising our FX forecasts this month in favour of EUR/USD trading within a 1.10-1.15 range through to year-end.

Two year yield divergence suggests EUR/USD stays under some pressure

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more

Included in the following bundle

ING Monthly: The masks, and the gloves, are coming off

- This bundle contains 15 Articles