European Taxonomy: Now the banking sector gears up for more disclosures

The second Taxonomy disclosures for banks include a variety of methodologies hindering comparability. Calculation differences aside, banks slightly improved their eligibility ratio with an average of 30% for 2022, 2pp above 2021. More banks reported their eligible asset share over their covered assets, in line with GAR requirements starting in 2024

Why should we keep an eye on the European Taxonomy?

While the European Union is showing its dedication to making the financial system more sustainable with the introduction of the Sustainable Finance Framework, the European Taxonomy is still being improved via the first disclosures.

For the first time, European corporates were required to disclose their share of Taxonomy-aligned activities this year. Next year, it will be the turn of the banking sector. For FY 2022, financial institutions were still required to disclose their share of Taxonomy-eligible assets. Surprisingly, this second year of disclosures is still marked by differences in the eligibility calculation. Comparing results with last year’s disclosures and between peers is, therefore, complex. However, several indicators are still worth analysing as the Taxonomy disclosures' tradition is building.

Banks must rely on their clients' disclosures to derive their own eligible and aligned share of assets. Hence, it is also interesting to have a look at corporates' disclosure patterns. Furthermore, these requirements are still evolving as the regulator recently shared the delegated acts covering the last four environmental objectives of the framework. With time, the European Taxonomy promises to be the cornerstone of sustainability both for financial and non-financial entities, limiting greenwashing by being the first comprehensive list of green activities.

The following sections give a refresher on the EU Taxonomy before diving into this year’s financial institutions' disclosure results. To conclude, we’ll look into the next steps and current challenges.

EU Taxonomy what?

The European Commission introduced its sustainable finance framework in June. The package aims to complete the EU sustainable agenda to support corporates and financial institutions' transition to a carbon-neutral and sustainable economy, starting with lowering implementation costs and enhancing the usability of the EU Taxonomy for all market participants. Indeed, the fundamental part of the European Union's action against climate change lies in the classification and definition of sustainable activities; in other words, the European Taxonomy.

The European Taxonomy classification system lists environmentally sustainable activities to enhance the transparency and comparability of ESG performance metrics. To do so, it uses six environmental objectives:

- Climate change mitigation

- Climate change adaptation

- Sustainable use of water and marine resources

- Transition to circular economy

- Pollution prevention and control

- Protection and restoration of biodiversity and ecosystems

The framework targets corporates as well as financial institutions and insurers in the EU. The first milestone was reached last year as both financial and non-financial institutions disclosed, for the first time, their Taxonomy-eligible assets as part of the Non-Financial Reporting Directive (NFRD).

Enforced in 2014, the NFRD aims to improve the transparency of social and environmental information provided by companies in all sectors. Large, listed companies but also banks and insurance companies with more than 500 employees fall under the NFRD and are therefore required to publish annual reports on their sustainable policies. These include a broad range of criteria such as social responsibility, respect for human rights, anti-corruption & bribery, but also diversity on their boards. As this directive only covers the largest European financial and non-financial entities, it includes around 11,000 companies having activities falling under the Taxonomy-eligible criteria. This number is expected to significantly increase with the enforcement of another directive, the Corporate Sustainability Reporting Directive (CSRD).

The CSRD aims to complete the current NFRD by gradually increasing its scope to incorporate smaller companies and third-country entities in the reporting framework. It will also tackle some NFRD issues by enforcing a common reporting framework. In December 2022, the European Commission amended the CSRD; it will become applicable in 2024. Entities gradually falling under the CSRD scope will automatically also have to disclose their Taxonomy-alignment under the European Taxonomy.

The EU Taxonomy is expected to be fully implemented in 2029

All these disclosure frameworks are implemented to direct the European economy towards a greener future through more transparency and comparability between market players. The Green Asset Ratio (GAR) seeks to do exactly this by giving at a glance, with one ratio, the sustainability of financial institutions.

The Green Asset Ratio in a nutshell

The European Commission requires credit institutions to publish several Key Performance Indicators (KPIs) giving insight into the extent to which their operations are environmentally sustainable, the most important one being the Green Asset Ratio. The GAR measures the share of the credit institution’s Taxonomy-aligned balance sheet exposures over the total eligible exposures. This allows to give a quick and comparable overview of the credit institution’s alignment with the Taxonomy.

GAR equation

The following on-balance sheet exposures are considered as eligible:

- Non-financial corporates subject to NFRD disclosure obligations

- Financial corporates

- Retail exposures

- Loans and advances financing public housing

- Repossessed real estate collateral

Taxonomy-eligible: Activities identified in the Climate Delegated Act and Environmental Delegated Act as eligible for the purpose of financing the EU Taxonomy six environmental objectives.

Taxonomy-aligned: Taxonomy-eligible activities that fully comply with the EU Taxonomy’s technical screening criteria for substantial contribution; they do no significant harm and with the minimum safeguards.

Exposures to central governments, central banks and supranational issuers are excluded from the calculation of the numerator and denominator of the GAR. Exposures to undertakings not (yet) obliged to disclose non-financial information under the NFRD (or CSRD) will be excluded from the numerator of the GAR.

What's new this year?

Financial institutions were already required to report their share of Taxonomy-eligible assets for FY 2021. In that sense, nothing changed this year as banks were only required to declare that same ratio but for FY 2022. Financial institutions were granted a one-year transition period in comparison to corporates as they rely on their clients’ disclosures to estimate their own portfolio alignment.

Financial institutions' first reports shed light on some important discrepancies in both methodologies and results, both between jurisdictions and banks domestically. When aggregating FY 2021 results at the national level, the highest Taxonomy-eligible assets rates were disclosed by both Belgian and Spanish banks (with 46%), followed closely by Norwegian banks (45%). Nonetheless, Belgian banks' eligibility rates varied domestically between 20% and 83%.

The same pattern was seen in Sweden, where banks reported Taxonomy-eligible asset shares between 19% and 67%. We explained these differences through the structure of each bank’s assets on their balance sheet. Indeed, as for corporate exposures, only the NFRD assets are considered in the eligibility criteria, banks with a portfolio mainly built of residential real estate disclosed higher Taxonomy-eligible rates than those active mainly in the corporate lending sector. To find out more about banks’ FY 2021 disclosures, read our previous research here.

Building on last year's results, we dived into the Taxonomy disclosures of the same sample of 31 European banks (from 13 countries) and derived the average national Taxonomy-eligible asset share. However, even with better accessibility to each financial institution’s documentation, one problem remains: there are still significant differences in the methodology used to derive the eligibility ratio. Indeed, the regulation allows corporates to calculate this share using three Key Performance Indicators based on the following:

- Their Turnover

- Their Capital Expenditure (CapEx)

- Their Operational Expenditure (OpEx)

Corporates are, therefore, reporting their eligibility over one or several of these KPIs. Consequently, banks disclosed their eligibility very differently, sometimes as a share of their non-financial counterparties' KPIs, sometimes as a share of total assets and in most cases, as a share of covered assets. These discrepancies are even more important than last year’s disclosures, in which the vast majority of credit institutions in our sample disclosed over their total assets and only a few over their covered assets.

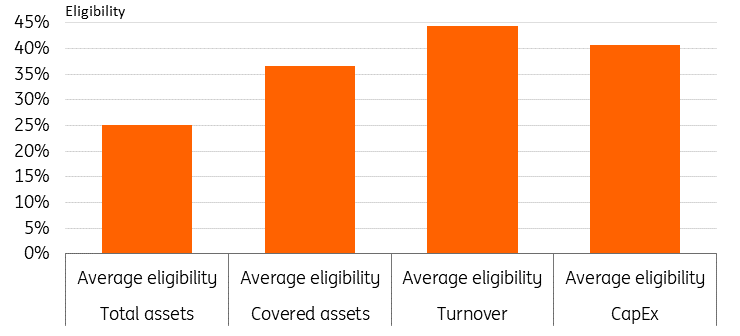

These differences significantly hinder the results’ comparability. Indeed, when aggregating the respective Taxonomy-eligibility ratio per methodology, we can see that, on average, banks disclosing over their Turnover have a better result (44.5% eligibility) than when disclosed over their total assets (with only 25%). It's important to note that 22 of our sampled banks disclosed their results with at least two different methodologies.

Banks disclosing their eligibility over their Turnover KPI were on average showing 44% eligibility

This rate drops to 25% when reporting over total assets

The most commonly used methodology remains Taxonomy-eligible share over total assets (used by 22 institutions); second comes the eligibility over total covered assets reported by 19 banks. Therefore, we can attribute the higher shares of eligibility when using Capex and Turnover ratios to both the methodology itself but also the sample of banks deciding to report in such a way.

Considering that last year's reporting was mostly done over banks' total assets, to identify national variations in Taxonomy-eligible assets, we only selected data points from the 22 banks that disclosed their eligibility as such this year. Aggregating the data nationally and averaging it allows us to highlight some changes.

At first glance, banks’ FY 2022 disclosure seem to indicate lower eligibility asset share

Nonetheless it's both related to the sample and change in used denominator.

Firstly, some countries such as Germany, Spain, France and Italy show no eligibility this year, but this is strictly due to a change in disclosure methodology. Their domestic banks are no longer reporting over total assets but opted for covered assets as the denominator.

Secondly, only three countries show an improved average eligibility disclosure over their total assets: Finland, The Netherlands and Portugal. This cascades from both a change in their portfolios' sustainability and a potential bias from banks changing their methodology since last year (thus being excluded from this graph and the national average).

The other interesting variable to look at is the share of non-financial counterparties not subject to the NFRD (NFC not subject to NFRD). Indeed, this part of the banks’ portfolio is currently not eligible under the Taxonomy, mostly because it is composed of small and medium-sized enterprises. Nonetheless, these entities will gradually become eligible through the enforcement of the CSRD. The higher the rate of NFC not subject to NFRD, the higher the eligibility might get in the future. This is exactly what we can observe in our data as Poland and Portugal disclosed, on average, the lowest Taxonomy-eligibility asset share but also have an important share of NFC not subject to the NFRD. Zooming in on disclosures over covered assets, this year is led by Spain, Sweden and Finland, which, on average, are disclosing more than 40% of Taxonomy-eligible assets.

Putting calculation differences aside, on average, the eligible asset share increased by two percentage points compared to the FY 2021 disclosure, reaching 30% for FY 2022. Unfortunately, deriving further conclusions from these data points remains difficult as national averages can be biased by the number of institutions choosing each methodology. In the future, we can only hope for the further harmonisation of methodologies as reporting standards are evolving.

German, Spanish and French banks only disclosed their eligibility ratio over their covered assets this year

Nonetheless, we can highlight important national differences in the disclosed eligible asset shares as we could last year. The most important one remains for Belgian banks, in which the variation between the highest and lowest disclosures is more than 40 percentage points. Important variations are also noted in the Netherlands and Sweden with respectively 34 and 35 percentage points differences. These discrepancies are both related to the methodology variation and the banks’ portfolio composition, as discussed above.

Belgium, the Netherlands and Sweden have the most important eligibility variations nationally

The first Taxonomy-alignment disclosures happened this year for corporates falling under the NFRD. Entities were also required to disclose their share of activity eligible to the Taxonomy over one of the following three KPIs: Turnover, CapEx or OpEx. In their 2022 Taxonomy barometer, EY highlighted that on average, aggregating data from all sectors sampled, eligibility disclosed over CapEx is showing the highest results with 35% eligibility, followed by shares over the OpEx and Turnover, respectively at 28% and 27%.

Most importantly, across all methodologies, EY reports that the sectors disclosing the most important eligibility ratio were the construction, energy, mobility and mining sectors. Health, manufacturing, consumer goods and oil & gas industries lie on the other end of the list. For energy companies, the share of Taxonomy-aligned activity depends on the KPI used. The disclosed shares of Taxonomy-alignment are between 1% and 20% lower than the one reported as eligible (the most important difference with Turnover KPI).

Insights on sectors declaring the highest share of eligibility can give a first idea of which type of bank will be able to improve or declare a high eligibility, now and in the future, Taxonomy-aligned share of their assets. Banks with an important mortgage and real estate portfolio but also banks with large corporate lending in construction, energy and mobility sectors will automatically be able to disclose higher shares of Taxonomy-aligned assets. However, banks that have an important portfolio of small and medium enterprises will see their Taxonomy-eligible share at a low level until the CSRD is enforced and more of these entities are required to disclose on their sustainability.

Step by step, going towards better disclosures?

Considering disclosures results from both financial and non-financial institutions, one question remains: are we heading in the right direction to reach the EU's sustainable goals?

The Taxonomy’s ultimate objective is to develop a financial system and economy as a whole, rewarding sustainable activities and supporting every sector to transition to more sustainability. Classifying and labelling an activity as green also involves comparing it to its industry peers. Nonetheless, results currently derived from the disclosures don’t allow a smooth comparison between actors, thus also preventing coming to extensive conclusions. It's the main issue hindering a thorough analysis is the variety of methodologies used.

Indeed, the Directive states that corporates should disclose a share of their assets over one of the three aforementioned KPIs. This affects results solely due to differences in the equation denominator. Through the nature of their business, banks inherently have to adapt to their clients’ variety of taxonomy disclosures when reporting on their own portfolio. That means that both the initial data points and calculation can vary between financial institutions.

We notice there's been a big decrease in calculations over total assets for financial institutions this year. Some banks started disclosing over CapEx KPI, which was unseen last year. However, we highlight the largest increase in the use of total covered assets in the denominator. This is rather unsurprising as it aligns with the GAR disclosure requirement for financial institutions entering into force in 2024.

Just as last year, obtaining sufficient and accurate information to qualify their portfolio remains an important challenge for credit institutions. There has been some improvement compared to FY 2021 in data accessibility as most banks are now more clearly disclosing their Taxonomy disclosures in their annual or sustainability report. The European Commission will further improve information sharing with the implementation of the European Single Access Point, a Directive aiming to improve data sharing for regulatory disclosures. The single access point is still in the legislative process. Nonetheless, the current proposal aims at an implementation in 2027 with a slow phasing in. This platform, once in place, will allow banks to gather companies’ disclosed data for their own regulatory disclosure.

Besides the difficulty of sourcing adequate information, the lack of suitable processes is also harming financial institutions’ ability to closely report on their portfolio. The EU Delegated Act on the first two objectives of the Taxonomy, climate change mitigation and adaptation, was only published in mid-2021. It left very little time for both corporate and financial institutions to prepare their first-year report. As time passes, we can expect an improvement in the application of the policy as more information will be available to banks and experience will be developed. That said, the Taxonomy still includes rather significant room for interpretation. It will require several years for European Institutions and the involved parties to smoothen the process.

Next year’s Taxonomy-aligned asset disclosures for financial institutions are the next important milestone in the implementation of the policy. It will be the second year for corporates, but as we can expect a bit more expertise in their disclosures, a lot is still to be done on the banks’ side to gather and analyse their clients’ data and draw their own share of Taxonomy-aligned assets. This process will also require a qualified workforce to both enforce the policy for the first time and gather the large amount of data necessary to comply with Taxonomy requirements.

European Institutions also have a consequent amount of work to provide. Indeed, only two of the Taxonomy objectives (climate change mitigation and adaptation) delegated acts are currently enforced. In June this year, the four other delegated acts were adopted (covering sustainable use and protection of water, transition to a circular economy, pollution prevention and protection and restoration of biodiversity and ecosystems). It is now time to enforce these new environmental objectives.

On the Financial Institutions’ side, this year was marked by a strong increase in reporting over the total covered assets, in line with the GAR disclosures. If that trend further develops next year, it will enhance peers and national comparison. It would also allow us to derive a potential improvement in banks’ portfolios.

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. Read more

Download

Download article

23 October 2023

Banks Outlook 2024: A world of higher for longer This bundle contains 7 Articles