Grid operators, utilities and oil & gas majors invest in hydrogen

Hydrogen could be an important future energy source, but it can only thrive with the support of good infrastructure. A European hydrogen backbone requires €43-81bn investment. European transition system operators have been taking the lead, followed by European utilities that are allocating 3%-6% of total investment to hydrogen

It all starts with infrastructure

The establishment of a hydrogen market will not be possible without a network infrastructure in place. Isolated national hydrogen grids will not be viable in the long term because hydrogen procurement will need to be established on at least a European-wide basis, if not even more broadly international than that. Overall, the reconversion of existing natural gas networks, the building of new pipelines, storage capacities and international interconnections, implies the need for substantial investments. In this article, we look at current investment plans by grid operators, utilities and the oil and gas majors.

European hydrogen backbone requires €43-81 bn investment

Published in April 2021, the report “European Hydrogen Backbone”, also called the EHB initiative, offers the vision of 23 European gas infrastructure companies on the future of hydrogen grids. The report was first published in 2020 and included 11 players. The latest version provides analysts and specialists with a vision for the potential development of a European hydrogen grid infrastructure across Europe. The document presents updated hydrogen infrastructure maps for 2030, 2035 and 2040 with a dedicated hydrogen pipeline transport network, largely based on repurposed existing gas infrastructure.

| €43-81bn |

Costs of a European hydrogen backboneEstimate by 2040 |

The report also provides the readers with the estimated costs of the development of that 39,700km European hydrogen network infrastructure between now and 2040. Based on using 69% of repurposed natural gas pipelines and 31% new pipeline stretches, the European hydrogen backbone would cost between €43bn and €81bn. The range in costs can be explained by variable parameters, notably the various existing diameters of the pipelines (24, 36 or 48 inch) with smaller pipelines cheaper to repurpose.

European transmission system operators already invest in hydrogen

Natural gas has been a major source of energy for industries and households in a number of European countries. As a consequence, it is not surprising to see countries such as Italy, Spain or the Netherlands to be already testing and investing in hydrogen infrastructure. Although a lot of open questions remain about the future success of hydrogen in Europe and across the globe, Italian, Spanish and Dutch gas transportation network companies have developed an advanced vision of what they want to achieve. We focus on these specific grid operators as they currently seem to be the most active in hydrogen pipeline adaptation. We also only focus on the transition system operators (or TSO’s who operate the grid on a national level) as hydrogen use is generally first adopted by the manufacturing sector. Hydrogen is not yet much of an issue for distribution system operators (or DSO’s who operate local grids) as it is not yet a significant part of the built environment or transportation sector.

Snam is dedicating 50% of its 2020-2024 investment plan to hydrogen

In Italy, Snam SpA, the national gas transportation network company, included a €7.4bn investment target in its 2020-2024 strategic plan. About 50% of these €7.4bn are dedicated to the replacement and development of a gas network compatible with hydrogen. Today, the company has about 70% of its pipelines that can already carry hydrogen. Snam is also cooperating with players contributing to the other parts of the value chain to help enable the development of the supply chain. The company has partnerships with electrolyser producers as well as energy and utility suppliers, like A2A, Hera and ENI, as well as Italian railway operators for transportation capacities.

Enagas’ gas grids are already hydrogen compatible and do not require additional investment

In Spain, the Hydrogen Roadmap designed in October 2020, includes an investment of €8.9bn for projects across the hydrogen value chain. The main objectives are the installation of 4GW electrolysis capacity and 25% of industrial hydrogen consumption of renewable origin by 2030. The roadmap also set objectives for mobility services such as a minimum of two commercial train lines powered by hydrogen and 5,000 light and heavy vehicles in circulation.

As far as the Spanish gas transportation grid operator, Enagas, is concerned, the company claims to fully utilise the current gas infrastructure for hydrogen and does not need new hydrogen pipelines. Enagas concentrates its efforts on the production of biogas in partnership with various players.

| €6.3bn |

Amount of combined investments, in which Enagas is participating, to help develop and promote hydrogen production |

In collaboration with 60 partners, Enagas plays a role in 55 different projects throughout Spain: 34 green hydrogen and 21 biomethane projects. As such, the Spanish gas transportation company is taking part in a total joint investment plan worth €6.3bn. Some projects have secured funding from the European Union, such as the Puertollano plant, which is also being developed in collaboration with Repsol. The plant will generate hydrogen from solar energy and is capable of producing around 100kg of hydrogen per day. The amount of the funding has not been divulged. The power plant could be operational in 2024.

The Netherlands used to produce a substantial part of its own natural gas consumption. Over time, production has decreased, due to field depletions and the repetitive earthquakes in the region attributed to the gas fields’ exploitation. This has led to a substantial gas extraction decline from the Groningen gas fields. After 2022, the Groningen gas fields will be mostly maintained in order to provide a supply backup in case of harsh winters. This means that for the next few years, the Netherlands will be, by and large, dependent on international gas imports.

The energy transition plan of the Netherlands pushes natural gas partially, and potentially totally, outside the energy mix by 2050. Hydrogen is seen as one of the solutions to partially replace that possible natural gas gap.

| €1.5bn |

Nederlandse GasunieExpected investment between 2021 and 2027 |

Nederlandse Gasunie, the national gas transportation system operator, has been mandated by the Dutch government to build a hydrogen network. The company announced an investment plan which includes the adaptation of pipelines to transport hydrogen. The company identified investment needs of €7bn between now and 2030, including €1.5bn dedicated to a hydrogen network that connects the main industrial clusters in the Netherlands. 85% of the hydrogen grid involves the retrofit of existing gas infrastructure, 15% involves new pipelines. The Dutch government announced on 21 September, that it will provide half of the capital (€750 mln).

Furthermore, Gasunie has joined coalitions that focus on increasing the supply and demand of hydrogen, to ensure that the infrastructure meets high utilisation rates. Aligning infrastructure with hydrogen production and demand is therefore important but it is difficult to achieve in practice, as different actors have different investment horizons. Grid operators have to plan 15 years ahead, hydrogen producers 5 to 10 years, whereas the hydrogen users look just 3 to 5 years ahead.

European utilities allocate 3% to 6% of total investment to hydrogen

With current electrolysers capital costs of around €1 million per MW, one can estimate the amount of capital expenditure dedicated to hydrogen by European utilities. However, the electrolysers equipment is not the only cost associated with hydrogen development. Design, site construction, new installation of renewable capacity to feed electrolysers, storage and commissioning also add to the required total hydrogen capital expenditure.

As a result, a base of 100MW hydrogen capacity installation will generally incur a capital expenditure much higher than €100m. One example is Iberdrola’s 800MW green hydrogen plant project in partnership with Fertiberia. The project’s estimated capital expenditure is €1.8bn for a capacity of 800MW which is due to be ready by 2027.

| 3%-6% |

European integrated utilities’ average capital expenditure dedicated to hydrogen projects vs. total investment |

Looking at some of the European utilities’ ambitions (Engie, Iberdrola, Enel and Naturgy), we think that capital expenditure dedicated to hydrogen production remains modest in comparison with the companies’ total investment plans. On average, we estimate investments for hydrogen to account for between 3% to 6% of total investment plans per annum in the short and medium-term. Nevertheless, these estimates do not take into consideration support schemes including capex or revenue subsidies, which could account for up to 50% of the companies’ dedicated capex for hydrogen.

Hydrogen plans and estimated investments from European utilities

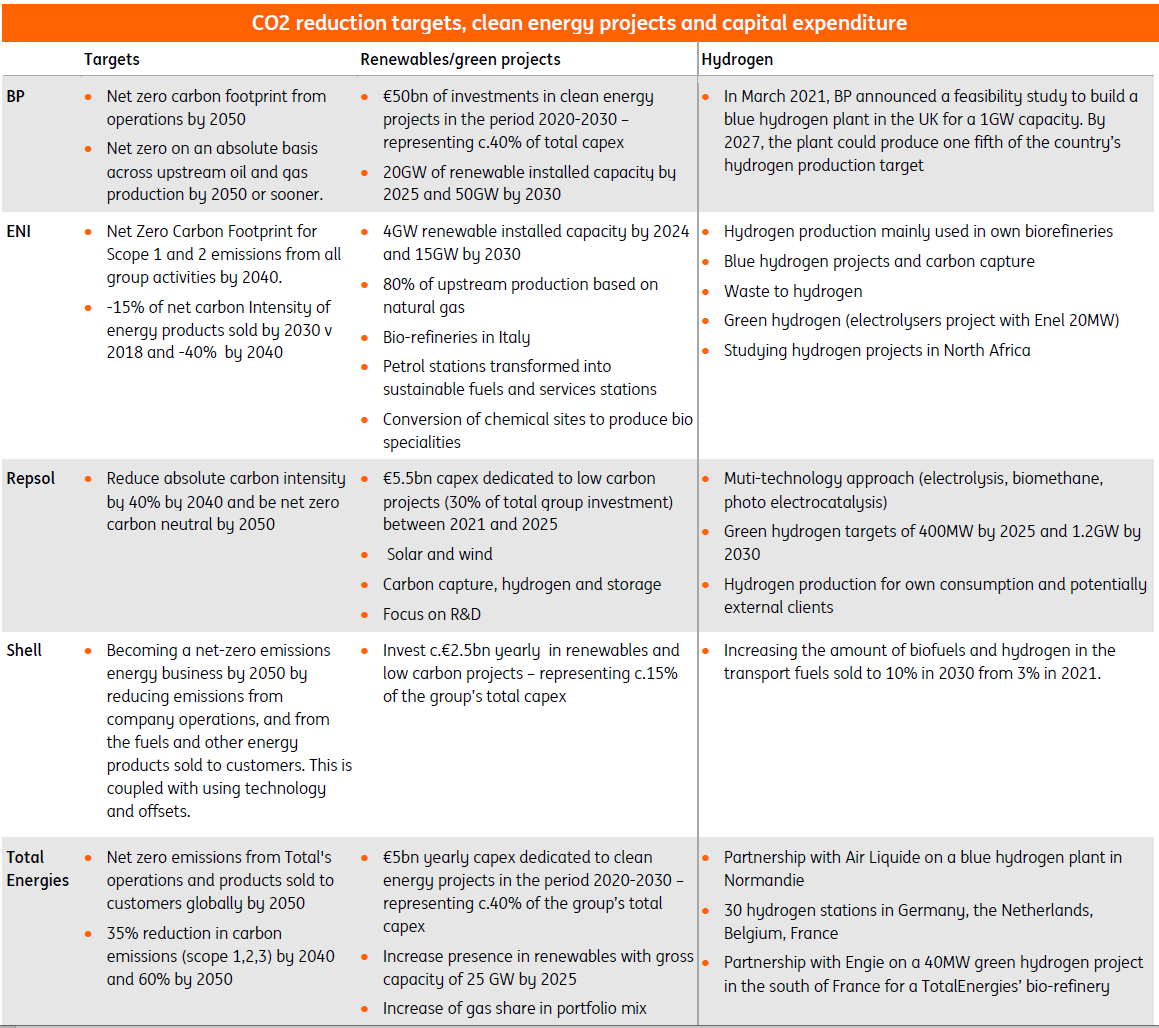

Oil and gas majors only commit small percentage of total investment to hydrogen

European oil & gas majors, such as BP, ENI, Repsol, Royal Dutch Shell and TotalEnergies, are committing investments for low carbon and green energy projects that range from between 15% and 40% of their total investment plans. All five European oil & gas companies are involved in hydrogen (grey, blue or green hydrogen projects). However, we estimate these projects will represent a very small part of the groups’ total capital expenditure.

Hydrogen plans for European oil and gas majors

Hydrogen could allow for new business positioning

Nobody knows yet how the growth of hydrogen will transform the energy value chain. In this section, we provide possible forces that could lead to new business positioning.

The European oil & gas majors announced major changes in their business models in the last two years. Under the pressure of societies, organisations and shareholders, energy companies are looking towards clean energies. With renewables, carbon capture and storage (CCS), hydrogen and biofuels projects in general, the sector wants to be part of the energy transition. However, compared to integrated utilities, oil & gas major’s hydrogen projects are skewed towards blue hydrogen given their historical business footprint in natural gas. That being said, European oil & gas majors have green hydrogen plans in the pipeline as well.

Oil and gas majors also have big pockets as far as investments are concerned and that's another advantage in taking a position in the hydrogen value chain. In the early stage, capital expenditure for hydrogen plants is relatively high compared to lower operational costs. That might give oil and gas majors an advantage. At a later stage, when the technology is more mature and cheaper, operational expenses will become more important which might benefit utilities that excel in running power plants.

Oil and gas companies have a competitive advantage in grey and blue hydrogen, utilities in green hydrogen

While integrated utilities see their role as hydrogen producers that offer solutions to industrials and corporates, European oil & gas majors look at hydrogen first as one of the means to decarbonize their own assets and products with the introduction of hydrogen for the obtainment of cleaner fuels. As such, utilities and energy companies are not necessarily direct competitors and have sometimes partnerships in place to develop hydrogen projects.

Although there are few signs of direct competition at the moment, some projects indicate that things could change in the future. As an example, BP is studying the feasibility of a blue hydrogen plant of a 1GW capacity in the UK with a potential construction green light in 2024 and that could start producing hydrogen in 2027. The Teesside project would capture CO2 and store it under the North Sea. The hydrogen plant would be linked to an industrial zone and the produced hydrogen could also be used for transportation and heating residential homes.

While we do see clear competitive advantages between the different players, it does not automatically means the market ends up in fierce competition. Some players might also choose to leverage each other’s strengths and will prefer to co-operate.

So hydrogen allows market players for new business positioning. How this plays out for the sector is still unclear but it is likely to increase market dynamics.

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. Read more

Download

Download article

28 October 2021

Hydrogen: The complete picture This bundle contains 4 Articles