Higher Bund yields: Tapering in focus for eurozone sovereign spreads

- 20 May 2021

- Credit Rates

Eurozone sovereigns have been the worst affected by the rise in yields. Some of this has to do with the eventual end of emergency PEPP purchases. With the ECB's help, or as carry demand re-emerges, spread widening should reverse. Italy will be the main beneficiary

Sovereign spreads: The other financial conditions indicator

An additional indicator of how much tighter financial conditions are is the dispersion of borrowing costs among eurozone sovereigns. There is more than one way to measure this but we refer to the GDP-weighted average yield on 10Y European Government Bonds (EGBs), and the difference with swap rates. By that measure, sovereign spreads have widened significantly since the through touched in February to levels last prevailing in November 2020.

The problem is that markets have had a tendency to force the ECB's hand

In the grand scheme of things, we are tempted to say that the ~25bp or so of widening is acceptable, provided it doesn't snowball into something more significant.

The problem is that markets have had a tendency to force the ECB's hand in the past. Sovereign spreads, Italy's in particular, have been the main conduit of that pressure. We could see yet more widening into the June 10th ECB meeting.

Sovereign yields have risen faster than swaps, a sign of tapering angst

Tapering angst

It is easy to pin the blame on PEPP angst. After all, the programme invests almost the entirety of its $80bn/month in sovereign and supranational bonds. Replacing it with smaller APP purchases, say from €20bn/month to €40bn/month, can’t completely replace that. There is a silver lining though. The Asset Purchase Programme is linked to inflation returning to target, PEPP to the ‘pandemic crisis phase’. As the latter comes to an end, the former is far from certain. In short, APP purchases could be with us for much longer.

The widening of sovereign spreads has been an almost mechanical effect of higher rates

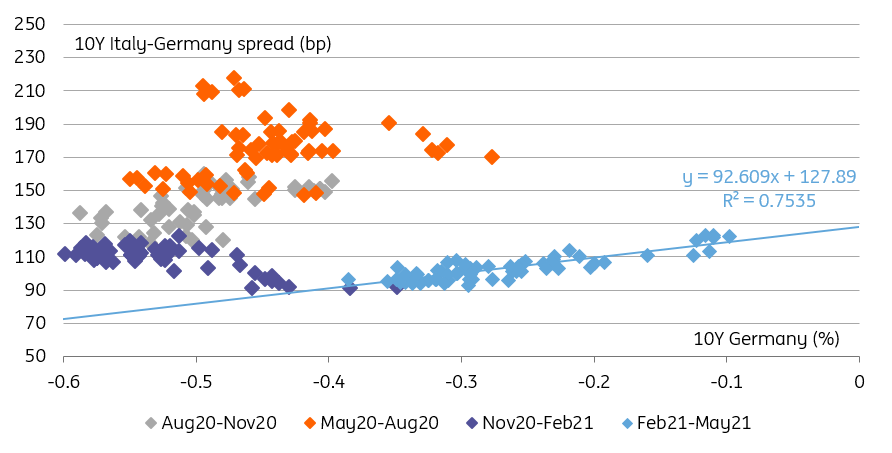

It will take time for that message to sink in, unfortunately. The widening of sovereign spreads this year has been an almost mechanical effect of higher rates. As we expect further Bund rises, wider spreads should ensue. Our best guess is that this relationship will ultimately be broken by ECB communication. This is all the more true given that fundamentals conspire to tighten sovereign spreads. Namely, the simultaneous recovery, greater fiscal spending at the EU level, and the prospect for more of both, and we've written about that here.

Only the ECB can break the mechanical link between higher rates and wider sovereign spreads

The Italian bond market is most vulnerable

Italy is a case in point. Its bond market is one of the most vulnerable on account of the just €380bn of debt it needs to sell this year. Fears of a lack of demand are misguided though. After accounting for bond redemptions and ECB purchases, we estimate Italy doesn’t need to find new buyers for its debt.

Based on the current relationship, our Bund yield forecast would imply another ~25bp of widening in the 10Y Italy-Germany spread.

| €380bn |

Italy's gross bond supply 2021Most will be offset by redemptions and ECB purchases |

We think cooler heads will prevail before, either thanks to ECB rhetoric or as the economic implications of Draghi’s ambitious recovery package sink in. This will in time bring that spread to 100bp, although we haven’t seen the end of the widening near-term.

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more

Included in the following bundle

Higher Bund yields: The complete picture

- This bundle contains 4 Articles