Greece: Uncertainty to grow amid upcoming elections

- 19 January 2023

- Eurozone Quarterly Greece

The end of re-opening effects will bring about softer demand as normalising fiscal policy takes away extra support. Upcoming elections will also add a pinch of political uncertainty to the mix

Greece's economic profile

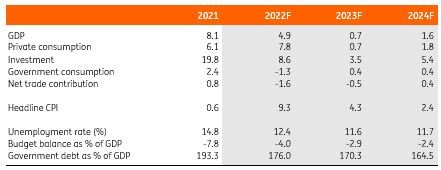

The Greek growth profile has recently reflected developments on the inflation front. The acceleration of inflation over the summer (culminating in September's 12.1% peak) took its toll on consumption, which saw a 0.1% quarter-on-quarter contraction in the third quarter of 2022 despite generous energy subsidies. Together with a net export drag, this caused a 0.5% contraction in GDP for the third quarter of 2022. We suspect a similar pattern will follow in the fourth quarter despite confirmed fiscal support and decelerating inflation.

End of re-opening effect to be followed by more domestic demand uncertainty

The outlook for 2023 remains uncertain. With GDP well above pre-Covid levels, re-opening effects should now be over. Tourism receipts also returned back to their historical peak in the summer of last year, making it unlikely that we'll see further substantial gains in 2023.

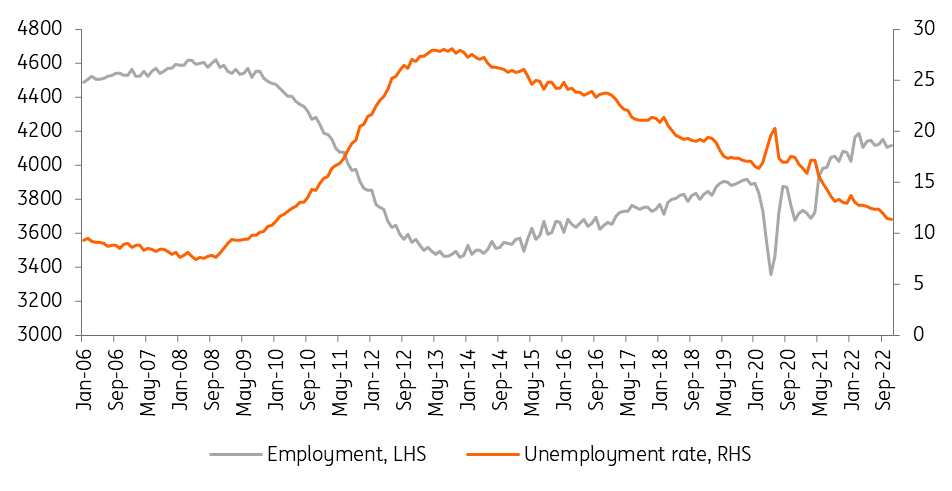

The recovery seen in employment was a powerful driver of consumption over 1H22 but now appears to be losing steam. Changes to real disposable income will increasingly depend on inflation developments, with inevitable side effects on consumption. Investments should, in principle, remain relatively supported thanks to the inflow of European Recovery Funds but will not be immune to persistent uncertainty surrounding the cost of projects.

Employment recovery is losing steam

Normalising fiscal policy to help further declines in debt/GDP

Fiscal policy, while possibly accommodating some extra temporary support in the case of continued energy price disruptions, will take a more disciplined turn. The Greek budget for 2023 targets a return to a primary surplus, which is consistent with the fiscal overperformance of 2022 and a more optimistic GDP projection.

We're currently less upbeat on growth, and although the primary surplus could be slightly missed, we see a substantial fall in the debt/GDP ratio towards the 170% level materialising nonetheless. With an average debt maturity of more than 18 years, the ongoing sharp rise in interest rates can still be accommodated in the short run without raising debt sustainability concerns. The inflation tax effect, albeit less powerful than in 2022, will still be at work.

Elections also carry some uncertainty

2023 will be an election year for Greece. Legislative elections are due to be held in July, but we can't exclude the possibility of prime minister Kyriakos Mitsotakis calling Greeks to the polls a few months early. The upcoming election will be held under a purely proportional system, a shift from the previous structure, which integrated the proportional element with a majority premium and has allowed New Democracy (ND) to rule the country in isolation since 2019.

The new system will make it much more complicated for any participant to obtain a parliamentary majority. According to the latest available opinion polls, ND leads with 37% of the votes, followed by Syriza (28%) and Pasok (11.5%). With these numbers, ND would be far from reaching a majority under the new system if it does not align itself with others (Pasok). Setting up a reliable coalition may turn out to be a difficult task. Add to this a campaign which might touch upon delicate issues (such as Qatargate) along with wiretapping accusations, and you get a decent mix of potential sources for political uncertainty over the second quarter.

The Greek economy in a nutshell (%YoY)

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more

Included in the following bundle

Eurozone Quarterly: Better is not good enough

- This bundle contains 10 Articles