Global Outlook: Trump’s Trade Gamble

- 6 July 2018

Uncertainty from President Trump's economic pronouncements could be more dangerous for the global economy than the direct impact on trade

The downside risks for market and boardroom sentiment

Our monthly economic outlook for July is dominated by the uncertainty created by Donald Trump's moves on tariffs and trade. The President vowed to “Make America Great Again” and a strong economy with low unemployment has been achieved. This success has emboldened him to push harder on trade. Although the EU and the US are still exploring possible solutions, business is braced for a step-up in protectionist policies over the summer. The uncertainty such behaviour generates implies downside risk for financial market and boardroom sentiment. This could be even more dangerous for the global economy than the direct impact on trade.

There is limited evidence so far that protectionist measures are derailing the global economy, but growth risks are skewed towards the downside over the summer. The coming months could see $600bn of trade hit with tit-for-tat tariffs between the US and China. Worse for Europe, there is also the possibility that auto imports to the US will also attract tariffs of around 20%.

The wider perspective

On their own, we are probably talking an impact measured in only one or two-tenths of a percentage point on global growth. However, the impact on financial markets and economic confidence may be much larger and lead to a more substantial slowdown in activity. Steep equity market falls and a downturn in investment and job creation could trigger a greater willingness to compromise. However, we doubt President Trump will change tack before the 6 November mid-term elections. His personal approval ratings have been trending higher and there has been some evidence of Republicans doing a little better in the polling. Nonetheless, right now the Republicans look set to lose control of Congress, which could open the door to an eventual shift in policy.

The fiscal and monetary situation

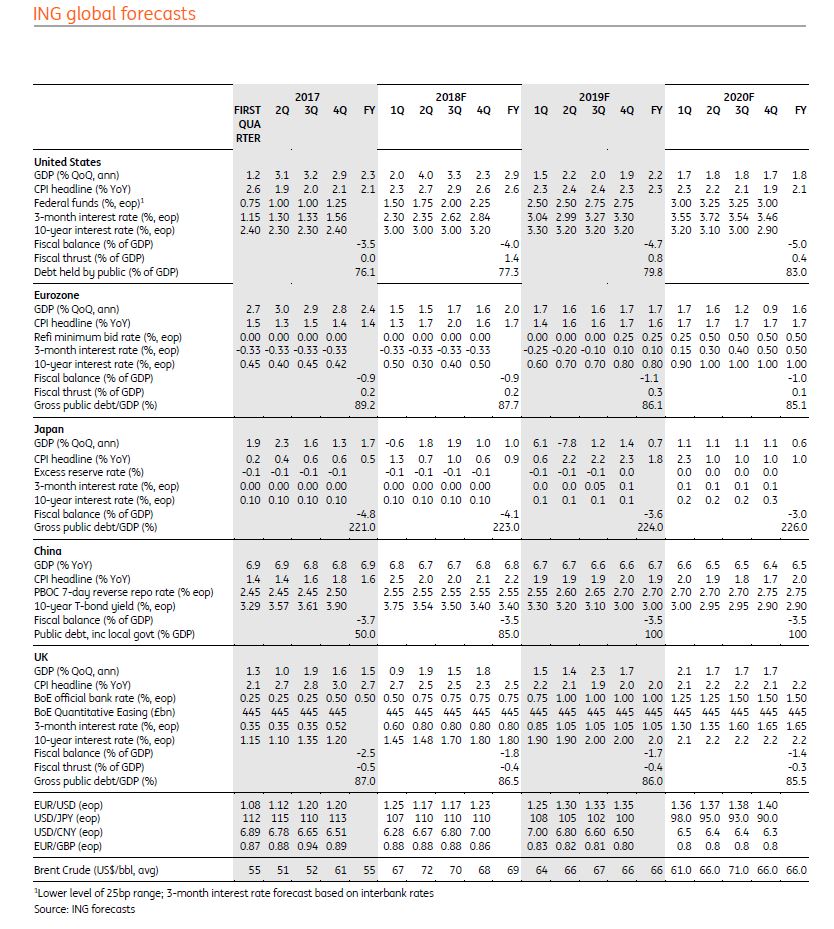

The US economy itself is performing well. 2Q GDP growth is likely to come in at around 4%, while inflation is set to rise above 3% in the next couple of months. With unemployment at 50-year lows, the Federal Reserve will stick to its “gradual” policy tightening of one hike per quarter, but the trade-related drags on activity will slow the pace of hikes next year. Trade war fears and financial deleveraging reform pose clear downside risks to Chinese growth. However, we are now seeing both fiscal and monetary policy loosening from authorities. The People’s Bank of China has ceased rate hikes and has cut reserve requirement ratios, while government spending is picking up. At the same time, the currency is weakening under market forces, which should all help to limit the damage.

Under the surface of falling sentiment indicators, political tensions in several countries and trade war fears, the Eurozone economy is continuing its solid recovery. As a result, the European Central Bank (ECB) can bring its quantitative easing (QE) programme to an end this year, but interest rates will likely be left unchanged for at least another year. Japan is not growing as fast as it was, and will not be immune to a looming global trade slowdown. But the domestic economy is looking a little more robust than for some time, and this could help provide some offset to a poorer export backdrop.

A dangerous cocktail in FX markets

FX markets continue to be governed by trade tensions and firm US interest rates. This is a dangerous cocktail for emerging markets as an asset class and supportive for the dollar in general. Risks to our EUR/USD forecasts are firmly skewed to the downside.

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more

Included in the following bundle

Global Economic Outlook: Trump’s Trade Gamble

- This bundle contains 7 Articles