Global Central Banks Outlook

As many developed markets tentatively begin to emerge from the Covid-19 pandemic, attention is turning to taper and tightening in many economies. Here's what to expect from the major central banks over the coming months

The outlook for central banks

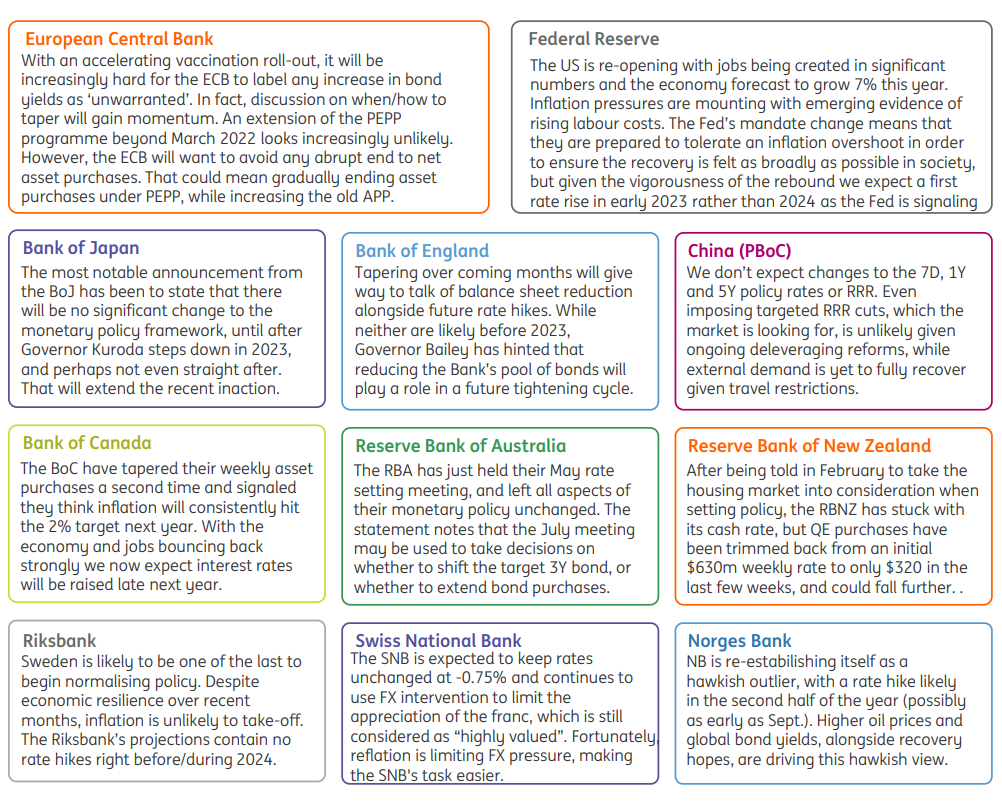

Federal Reserve

With the US economy set to return to pre-pandemic levels of activity in the current quarter and, by the end of the year, exceed the level of output had there been no pandemic, and the economy had merely continued at its 2014-19 growth trend, this has to raise concerns about potential inflation. The government has already pumped in $5tn of stimulus, and with another $4tn of infrastructure and social spending on its way on top of a rebound in consumer and business spending, we think the risks are skewed towards higher and more persistent inflation readings.

Indeed, there are near-term supply constraints, but with jobs also being created in significant numbers, the economy's spare capacity is being eroded, particularly given the pandemic has led to scarring in many sectors. The Fed has made it clear they are prepared to tolerate an inflation overshoot to ensure the recovery is felt as broadly as possible in society, but given our growth outlook, we think the Fed will soon be forced to bring their guidance on the first-rate hike forward. They are currently suggesting that it could be up to three years before the first move, but we suspect it will end up being early 2023.

European Central Bank

After the ECB successfully fended off higher bond yields on the back of spill-over effects from the US and higher headline inflation in the eurozone, a new challenge is looming in the summer. With an accelerating vaccination roll-out and some 50% of the eurozone population having had at least one jab by June, it will be hard to label once again any increase in bond yields as ‘unwarranted’. In fact, we see the discussion on when and how to taper gaining momentum in the coming months.

An extension of the PEPP programme beyond March 2022 looks increasingly unlikely with the current vaccination and economic backdrop. However, the ECB will want to avoid any abrupt end to net asset purchases. In our view, it will do its own operation twist: gradually ending asset purchases under the PEPP while increasing them under the old APP.

People's Bank of China

Our view remains that the People's Bank of China will keep its current monetary policy stance unless there are significant changes in the market.

The Chinese economy is undergoing deleveraging reforms, particularly in the real estate sector, and relaxing the monetary policy would contradict this process. But tightening of the current stance – the 7D policy rate at 2.2% and 1-year loan prime rate at 3.85% - when export demand is fragile is also equally unlikely. If anything triggered a change in monetary policy, it would be a rapid deleveraging process that creates market volatility.

The central bank would have to step in to relax liquidity temporarily. That could be probably a targeted RRR cut for environmental protection projects and the agricultural sector. But even then, the probability is small as the central government is very cautious and is adopting a gradual approach to the deleveraging process.

Bank of Japan

10-year Japanese government bonds currently yield close to 0.1%, higher than the Bank of Japan’s 0.0% target, but within its +/- 0.25% tolerance band.

In recent weeks, the central bank has refrained from buying ETFs. At its latest meeting, on 27 April, it projected the economy to grow at 4% for the year through to March 2022, but expected core inflation of only 0.1% and does not project that the target rate of 2% will be reached until after 2023 when Governor Kuroda steps down.

The Bank of Japan has also stated that the monetary framework will not be significantly altered until after Governor Kuroda has left, all of which implies that the current -0.1% target on cash rates will not be changed and that any changes in qualitative and quantitative easing (QQE) policy will be unofficial with official targets remaining unchanged.

Bank of England

With green shoots appearing across the UK economy, further Bank of England stimulus looks unlikely, barring any Covid surprises. That means attention is quickly turning to future tightening, and what’s becoming increasingly clear from officials is that this is likely to involve a mix of interest rate hikes and balance sheet reduction. Unlike the Fed, the BoE never got around to this in the post-GFC years. But under Governor Andrew Bailey, the Bank looks poised to shrink its bond holdings, partly due to the BoE’s ever-increasing market share it owns.

In practice, this could involve setting an annual target, which could see the Bank’s gilt holdings reduced via reduced reinvestments of maturing bonds. A £30-40bn annual reduction looks achievable – anything more may require active selling, which we think is initially less likely.

That all said, with inflation likely to present less of a threat than in the US beyond this year, we doubt any of this will happen before early-2023

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. Read more

Download

Download article

6 May 2021

The new symbol of global optimism: Dining in the rain This bundle contains 12 Articles