Global car market to hit the speed bumps in 2024

We expect global car sales growth to moderate this year after a strong 2023, which was driven by pent-up demand. The three key regions, the US, China and Europe, are all expected to maintain a mild positive trend. Meanwhile, we think the electrification process may slow although the upward trend should continue

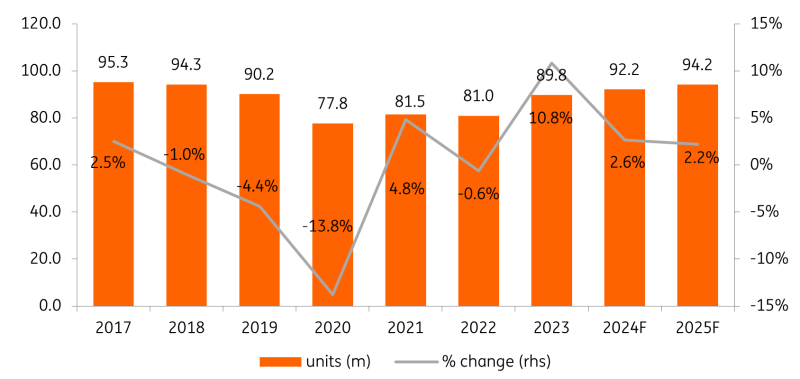

Strong growth recorded in 2023

Global auto sales recorded strong growth in 2023, exceeding our positive expectations. According to Moody's estimates, global car sales expanded at a robust rate of +10.8% year-on-year. Car sales recorded a double-digit rate of growth in all three major geographical markets last year, rising +12.4% in the United States, +11.0% in China and +13.7% in Europe (comprising the EU, UK and EFTA markets). Light vehicle sales in the United States, China and Western Europe increased last year by +13.3%, +12.0% and +14.2%, respectively, according to Moody’s statistics which we have been using for our historical data and forecasts. Importantly, the Chinese growth includes a contribution from China’s car exports (up approximately 58% YoY), whereas domestic sales grew by 6.0%, according to Moody’s (+5.6% according to the China Passenger Car Association, when excluding imported cars and commercial vehicles). The strong growth reflected pent-up demand that had been realised after delays with production and delivery experienced in the prior years.

Momentum to slow this year but remain positive

In 2024, we expect this positive sales momentum to continue but at a much slower pace after a strong increase in the previous year and given a muted macroeconomic backdrop. Another factor reflected in our forecasts is the expected slowdown in the rate of proliferation of electric vehicles, which has been supportive during the last couple of years. Currently, we forecast global car sales growth of +2.6% in 2024.

Global car sales growth rate set to slow

In terms of regions, we assume car sales growth of +2.0% in the United States, +3.0% in China (including exports) and +1.5% in the European market. Our cautious outlook for sales growth across the regions stems from the muted economic outlook for this year across the key geographies with consumer confidence still subdued. With interest rates remaining more elevated right now and second-hand car prices falling, demand for new vehicles is more muted. In addition, as we will discuss later, we expect slower demand for new electric cars during the current year. We also expect Chinese export sales growth to slow after a very strong jump in 2023 while domestic demand may also be less strong. We will monitor our forecasts as the year evolves as new supportive or negative factors may come to the forefront.

We expect relatively flat production volumes in the current year

We anticipate that light vehicle production volumes will stay flat or increase only slightly year-on-year in 2024. This is because we believe that after the robust rates of production growth during the past two years, in excess of the respective yearly sales volumes, inventories have now been rebuilt sufficiently to allow for more balanced production volumes relative to sales volumes. In fact, a flattish rate of production growth should still allow for the replenishment and maintenance of inventories at sufficient levels given a more modest expected rate of growth in sales relative to 2023.

Auto makers' margins to soften this year

We would expect the profit margins of automakers to come under some pressure during the current year after a period of above-average profitability in the post-pandemic period when OEM’s had relative pricing power and greater influence over the mix of sales. While we anticipate margins softening in 2024 year-on-year, we do not expect, and so far the car manufacturers are not flagging, a particularly pronounced margin dilution this year either. Conversely, we expect that auto parts manufacturers have a higher chance of maintaining or even slightly expanding their margins in 2024. This is because we believe that they will benefit from the tail-end effect of the earlier price adjustments and cost cuts implemented during the prior years. We also note that lower raw material prices should present tailwinds for both car and auto parts manufacturers.

Sense of reality for electrification while the upward trend continues

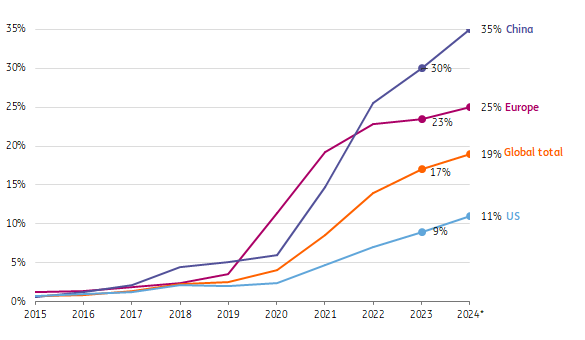

The global penetration rate of electric cars (EVs) continued to increase to 17% of new sales over 2023 (battery electric vehicles BEV + plug-in hybrid electric vehicles PHEV), but the regional picture is currently more mixed. The main engine is still China, also the world’s largest market. With continued fiscal support, an abundance of production capacity and well-developed regional supply chains, Chinese new EV sales hit 9m last year (30% of total sales), making up the vast majority of global sales. Chinese-built cars also gained more traction in the rest of the world. Exports of vehicles - including those of BYD (which overtook Tesla as the largest BEV producer in 4Q 2023) soared (+57%) and growth is set to continue in 2024 as they seem to be meeting customers' needs. Europe is increasingly wary of the adverse effects of dumping and started an investigation that may lead to extra levies, although not before the end of the year.

At the same time, Europe and also the US, face a slowdown in EV uptake compared to previous expectations. The main reason behind this is the scaling back of subsidies in large car markets, while subsidies are currently still an important driver for EV sales growth. In particular, the sudden termination of purchase subsidies in Europe’s largest market, Germany, will be a drag on EV sales into 2024 and the ending of subsidies has also stalled the further uptake in the UK. But there are more reasons:

- Residual values of EVs are under significant pressure because of price cuts for new cars. This leads to a more cautious approach among leasing and rental companies. As such, rental companies, Hertz and Sixt, also decided to trim their EV fleets in the US and Europe.

- EVs are often financed and the combination of higher interest rates and lower residual values pushes up monthly leasing terms.

- New EV drivers increasingly have to rely on public charging infrastructure and this hasn’t kept up with electrification in countries that have seen a surge recently. The opening of Tesla’s charging network to others can only create some extra charging opportunities.

Chinese EV rate steams ahead while lower prices support demand in Europe and US

Despite the current slackening in demand, the electrification trend inevitably continues and EV rates are still expected to hit 25% in Europe (from 23%). The US is behind in the market penetration of EVs but, supported by IRA subsidies, its share is still expected to go up to 11% in 2024, although this is less than previously anticipated. Moderation of demand, combined with receding (battery) raw material prices and largely resolved supply chain constraints puts average EV prices on a downward track again since the last few months of 2023. And gradually, newly introduced models are contributing to this. Increasing affordability brings electric cars closer to break-even again for car drivers, which is a positive signal for 2024. After rounds of reductions, a Tesla model Y now sells below the average car price in the US.

Within Europe, the differences are still large. A positive element in this is that lagging countries will have to catch up in light of a complete shift to zero emissions in 2035. As such, Europe’s fourth largest market, Italy, with a lagging total EV share of just 9% (BEV + PHEV) is expected to implement a subsidy scheme this year, which supports Europe’s total figure.

In China, there are still not many signs of a slowdown. The Chinese car market is less mature, and it benefits from growing car ownership (first buyers opting for EVs) and the government is keeping its hands on the subsidy tap. We therefore expect the pace of growth to continue, with EVs reaching a share of 35% in 2024. Nevertheless, the adoption of electric cars is increasingly spreading from early adaptors to middle-class drivers in China, which comes with more concerns around charging possibilities (although battery swapping is seen as a promising concept in the country).

EV shares continue to climb, while Europe faces a slowdown and the US lags

Share of electric vehicles (BEV + PHEV) in total new car registrations per region

Competition mounts in EV race – manufacturers in strategic balancing act between margins and repositioning for the future

Exporting Chinese car manufacturers have increased the competition in the global EV market. In the run-up to 2024, Tesla added to the pressure by reducing its new prices several times to keep production figures growing. Other car makers were forced to follow suit, such as Ford with its Mustang Mach E. But this eats into margins that are already small or still negative. The pressure on new EV prices challenges new and incumbent manufacturers to reduce costs and puts them in a difficult strategic position. On the one hand, they are pressed to temporise EV production increases as conventional cars still generate higher margins. On the other hand, progress is important to secure future market share in the run-up to 2030, when EVs will likely see more traction among drivers with further improving economics and improved charging infrastructure. Together with the extra time required to bring local production of batteries up to speed (and reduce dependency on China), several of them including Ford and GM in the US decided to push back production ambitions for EVs. In Europe there have been announcements of delays as well, such as for VW's ID.2. Manufacturers face a new European CO2-emission hurdle in 2025 (-15% vs 2021) for the average production, but they can still work around it by buying emission credits from Tesla (delivering $9bn in 2023). But the tumbling share prices of pure EV players also indicate that the EV transition is increasingly putting them under pressure too, indicating that some brands will not survive as the market restructures and matures.

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. Read more

Download

Download article