The global implications of Germany’s September elections

Germany's September elections not only mark the end of the Merkel era but could also mark a structural change in Germany’s fiscal stance

Since the 2017 elections, the German economy has gone through several ups and downs, while the structural economic problems have not changed. The 2017 elections took place against a backdrop of strong growth, low unemployment and the last phase of what many called the country’s second Wirtschaftswunder the so-called economic miracle.

The German economy had started to fall behind its eurozone peers

Since then industry, in particular, has experienced what it means for a traditional stronghold to face structural changes. On a gradual decline since mid-2018 due to several one-off factors, as well as ongoing trade tensions, this was the first sector to suffer from the outbreak of Covid in Asia. It became an important growth driver during the second lockdown and is currently suffering from supply chain frictions.

More generally speaking, the German economy had started to fall behind its eurozone peers in 2018 and 2019 but thanks to significant fiscal stimulus since the start of the pandemic will be one of the first eurozone countries to have returned to its pre-crisis level. Were all the warnings about structural weakness exaggerated or have they simply been resolved?

WEF Global Competitiveness Ranking

The answer to that question is 'not really'. Looking at some structural indicators, the German economy has, at best, stood still over the last few years, if not lost further ground. Rankings on international competitiveness have seen the German economy dropping further between 2017 and 2019. The quality of traditional infrastructure has weakened. Investment growth had been much weaker than in the rest of the eurozone until the start of the crisis.

The Digital Economy and Society Index, 2020 Ranking

Internet access remains slow and expensive compared with many other countries. And the costs of the energy transition are still high. Due to the pandemic, not all of the structural economic indicators were updated in 2020 or 2021 but the overall picture of the available indicators hardly looks any different to how things were in 2017.

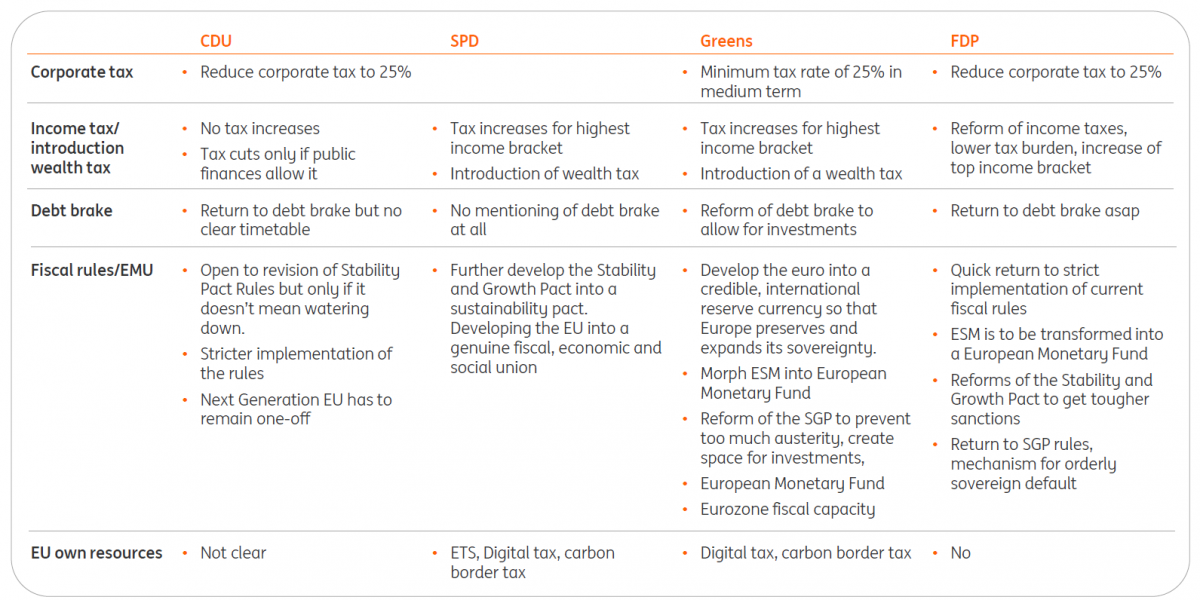

Economic policies according to the election manifestos

The pandemic has just been another reminder of Germany’s lack of digitalisation. Whether it is the digital infrastructure, the educational system, e-government or digital services, there is clearly plenty of upside potential for the economy in the years ahead. The U-turn of the incumbent government on fiscal policy, already ahead of the pandemic but in full swing during the pandemic, has prepared the ground for a more general acceptance of public spending and investment. Therefore, it does not come as a surprise that all parties have presented many plans on how and where to invest in the coming years. Climate change, demographic change with its impact on pensions and health care, digitalisation, energy transition and the structural change from manufacturing to services, just to mention a few hot topics, are all in the proposals. The financing of all these ideas, however, is not always very clear.

The pandemic has just been another reminder of Germany’s lack of digitalisation

What differentiates the four parties, with the highest likelihood to join the next government, is taxes. While the CDU/CSU and FDP advocate no tax increases but propose different forms of tax relief, the Greens and the SPD have proposed tax increases for the highest income bracket as well as the introduction of a wealth tax.

The discussion on the constitutional debt brake has somehow died down. CDU/CSU and FDP advocate a relatively swift return to fiscal policies in line with the debt brake, while the SDP remains silent on this issue and the Greens propose a reform. In our view, this discussion is mainly shadow boxing as it requires a two-thirds majority in parliament to change the constitutional debt brake. It looks very unlikely that any such majority could emerge after the elections. However, the CDU/CSU, Greens and also the SPD seem open to the idea of at least temporary workarounds, allowing for more investment and, in turn, higher debt in the coming years. This workaround could be a shadow household for investment in digitalisation, infrastructure or the fight against climate change.

All in all, there seems to be a broad consensus on the need for more investment and fiscal stimulus, obviously with widely differing views on the size and how to finance it. Regarding the eurozone level, however, views and proposals diverge much more. The Greens have the most ‘federal’ approach, while the CDU and FDP manifestos clearly put a brake on dreams of a fiscal union. Both parties would like to return to strict implementation of the fiscal rules. The CDU/CSU is keeping the door open to some changes in the fiscal rules but only if these changes lead to stricter rules.

The FDP is again advocating a mechanism for orderly sovereign default in the eurozone. While the SPD is keeping further reforms of the monetary union’s institutional framework in the air, the Greens are more precise with their ideas of eurozone fiscal capacity and changes to the fiscal rules. This demarcation line is also visible on other European fiscal issues with the Greens and SPD advocating own resources for the EU from a digital or carbon border tax, while the FDP rules out such own resources and the CDU remains rather vague.

The manifesto options

Main (European) economic topics in election manifestos of the four parties realistically forming the next government, in whatever combination

The experience question

The September elections will be the first federal elections ever in which the incumbent chancellor will not run for another term in office. As a consequence, the so-called Amtsbonus, the advantage of having the incumbent chancellor on the ticket, will not apply. Except for the SPD candidate and current finance minister Olaf Scholz, none of the running candidates has any experience at the national executive level.

CDU candidate Armin Laschet is currently minister-president of North-Rhine Westphalia, while Green candidate Annalena Baerbock does not have any experience in the executive. She is currently a member of the German parliament and party co-leader of the Greens. This lack of experience and a lapse in judgement by some of the candidates - be it slightly blown-up resumes, plagiarism, inappropriate laughing in public or other communication missteps - have put the focus on personality over policy. Instead of winning the electorate’s hearts, it currently looks as if the candidate who makes the least mistakes in the next two months will win the race.

However, don’t forget that at the elections, German voters cannot directly vote for the next chancellor; they have to give their vote to a party. Here, local personalities and topics matter as well. Fun fact: the Chancellor doesn’t have to be a person from the election list. In theory, anyone could be put forward to be elected as the next chancellor by the next parliament. As long as he or she gets a majority of the votes there.

How the politicians stack up

Evaluation of politicians according to sympathy and achievement (Mean values on a scale from -5 to +5)

A more fickle electorate

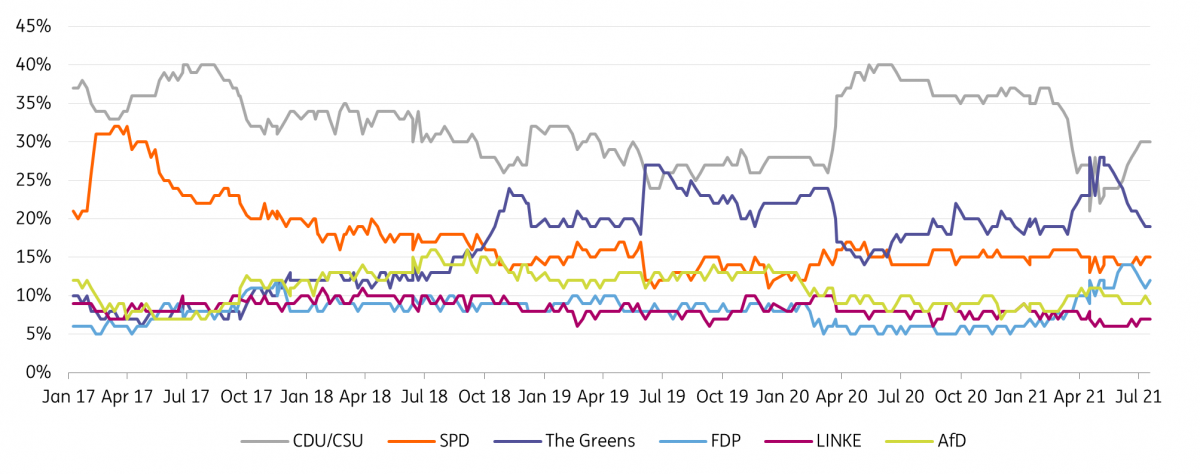

Developments over recent months have shown that German politics, or at least voter support, has become more fluid. Larger swings in the polls have become normal. Look at the latest rise and fall of the Greens. Therefore, with some two months to go, no one should jump to early conclusions about the final outcome. Personal missteps by the leading candidates as well as unexpected events such as the recent floods in parts of Germany could easily be game-changers in the coming weeks.

If there were general elections next Sunday who would you vote for?

Generally speaking, unless the Greens stage another comeback due to the latest floods, with climate change taking centre stage again, the CDU/CDU will probably come in as the largest party. Anything north of 30% would be a success, anything below a disappointment. The Greens currently look like the clear number two, still hoping to close the margin with the CDU/CSU. FDP, AfD and SPD will fight to become the third-largest party, with all three ranging between 10% and 15% currently. The Left Party has lost some ground and stands around 7%. Next to these six parties, no new party is expected to make the 5% threshold. But we should watch out for the European party Volt, which made some surprising gains in other European countries.

Change of times? Not really

Judging from the latest developments, we've expanded our base case scenario and see a CDU/Green and a CDU/FDP coalition as the most likely outcome (or possibly even another attempt to get the three parties into a coalition, as in 2017). In our view, any of these outcomes bodes well for more fiscal stimulus in Germany but don’t expect any major changes regarding fiscal policy at the eurozone level.

Given the CDU’s very explicit views, a coalition with the Greens is unlikely to advance ideas for making the European Recovery Fund more permanent and for closer fiscal integration. While in other countries, political divisions may centre around europhiles and eurosceptics, in Germany, it is only the level of eurozone integration that separates parties.

It currently looks as if the big German push for more eurozone fiscal stimulus will come with a “Germany first” investment agenda and some trickling through effects for the rest of the eurozone, rather than a “euro first” push. While this is bad news for euro federalists, it is good news for analysts and commentators, as the never-ending discussion on what should and will (or is politically acceptable to) happen is set to continue.

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. Read more

Download

Download article

23 July 2021

Message in a bottle This bundle contains 6 Articles