GBP: Theresa May’s impossible Brexit trinity

- 11 June 2018

A tricky summer of Brexit politics lies ahead, with PM Theresa May facing an impossible Brexit trinity. While the pound still remains a good value play, we have some sympathy for investors wanting to shy away from the currency until there is political clarity. We provide three scenarios for GBP based on how Brexit political risks unfold in the near-term

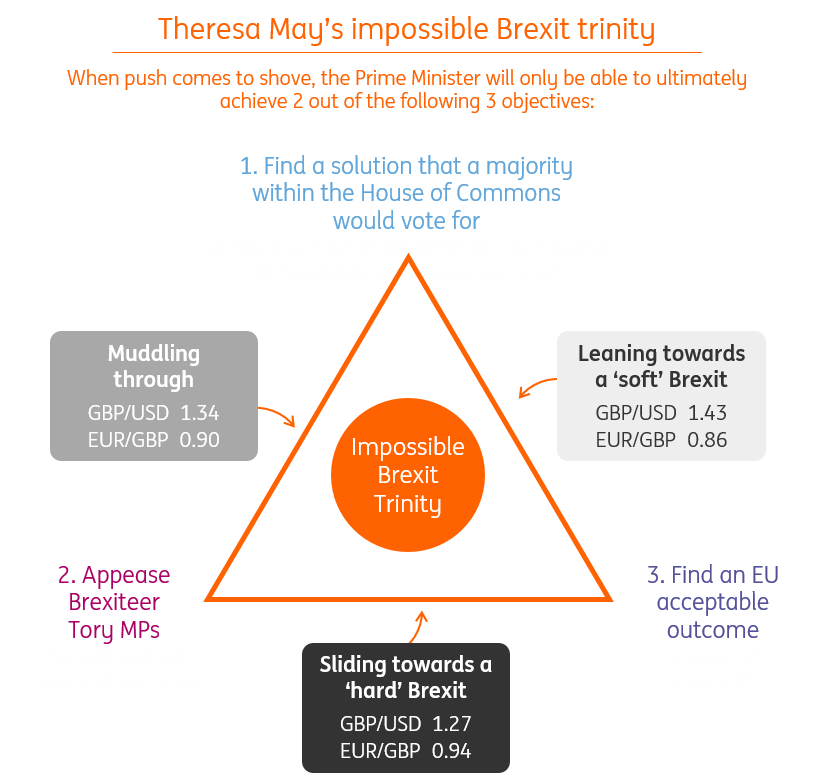

Theresa May's Impossible Brexit Trinity

While more recent GBP-specific ebbs and flows have been driven by the sharp re-pricing of Bank of England policy expectations, we expect the focus for sterling over summer to shift back to Brexit politics ahead of a crucial Commons Withdrawal Bill vote (tomorrow) and the 28-29 June EU leaders’ summit.

Theresa May’s predicament can be characterised as an impossible Brexit Trinity – with the Prime Minister trying to achieve three simultaneous objectives: (1) appease Brexiteer MPs within her own party; (2) find a solution that a majority of MPs in the House of Commons would back; and (3) find an outcome that is politically suitable for all EU members to accept.

When push comes to shove, we think the PM will only be able to choose two of these three objectives – and the broader trajectory for GBP will be a function of her choice.

Nervous times as May attempts to square the impossible Brexit Trinity

While our house view is currently leaning towards the UK government ultimately opting for a more benign (or a ‘softer’) Brexit customs union and trade solution – that is one that would ultimately pass the House of Commons and EU hurdles – this is a fairly low conviction call at this stage. Moreover, the risks of this outcome could be rebel Tory Brexiteers pushing for a leadership contest – or even a general election (though we place a low probability on either event occurring).

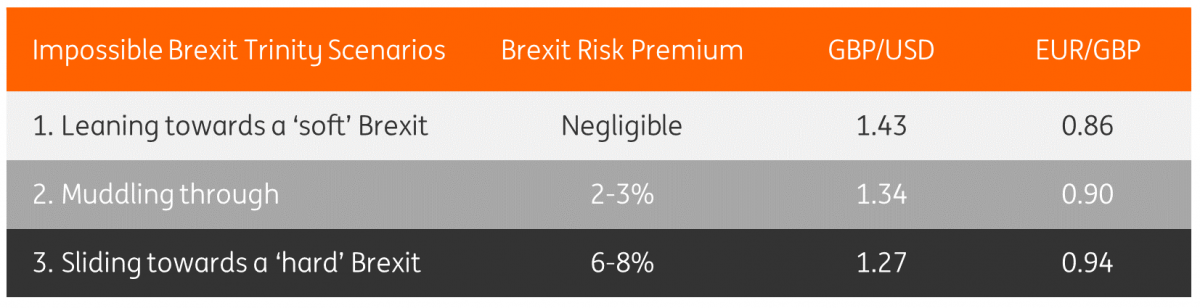

The focus of this note, however, is not to form a judgement on the likely political outcome (our economists do a good job at tackling this impossible task). Instead, we provide some scenario-based estimates for GBP/USD and EUR/GBP - modelling the outcomes based on the level of Brexit risk premium we expect to be priced into the currency within each scenario:

- Leaning towards a 'soft' Brexit (negligible risk premium): PM May forced down the path of a more benign and smooth Brexit transition that lifts GBP sentiment and allows the currency's focus to shift firmly on the UK data and Bank of England policy tightening story (note in this scenario the probability of an August BoE rate hike increases – assuming UK data remains in line with the Bank's expectations).

- Muddling through (2-3% risk premium): Clarity on the government's Brexit strategy remains vague as the Prime Minister attempts to appease both Brexiteer ministers in her own Tory party and the majority within the House of Commons. The likelihood here is that any solution that unites both groups will be rebuffed by the EU.

- Sliding towards a 'hard' Brexit (6-8% risk premium): Theresa May opts to align with the Brexiteer Tory MPs – and pushes talks with the EU towards a 'hard' Brexit. The likelihood of a 'No Deal' picks up – with material risks that the UK could exit the EU in March 2019 without a transition in place.

Brexit risk premium assumptions under each scenario

Short-term Brexit uncertainties keeping GBP sidelined for now

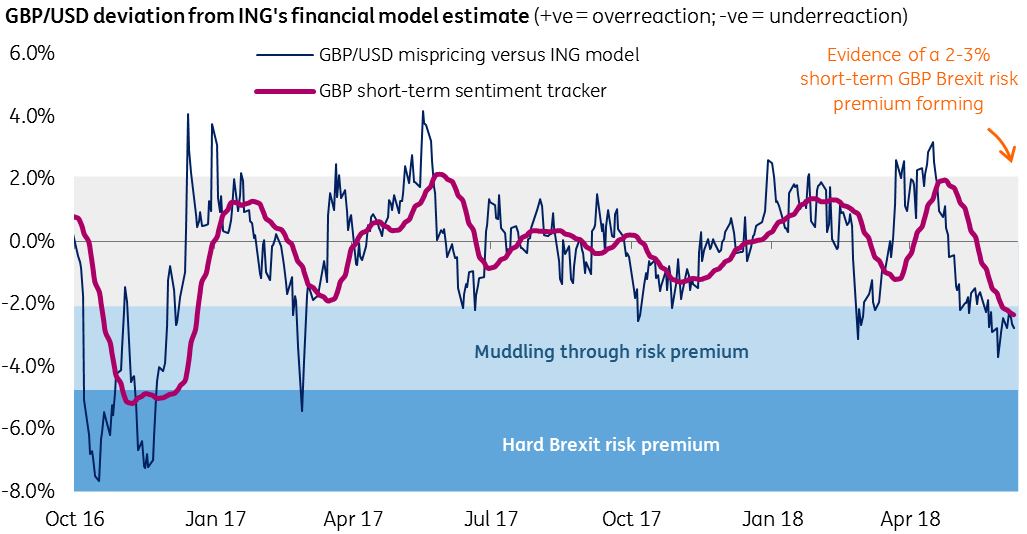

We estimate that GBP/USD is trading with a 2.5-3.0% discount at present – which is indicative of a 'muddling through' Brexit risk premium. This is unsurprising given the near-term focus on the Commons Withdrawal Bill vote (tomorrow) and the 28-29 June EU leaders’ summit. We would expect this uncertainty premium to remain in the price of GBP until further clarity on the Brexit front.

However, GBP's currently depressed value suggests that a lot of 'bad' Brexit news is already in the price. For a more sustained downturn, we'd need to see the probability of a 'hard' Brexit pick-up substantially. This week's events in the House of Commons are unlikely to shift one's assessment materially (in either direction).

Bottom line: A lot of bad news priced in... but hard to find a positive Brexit catalyst

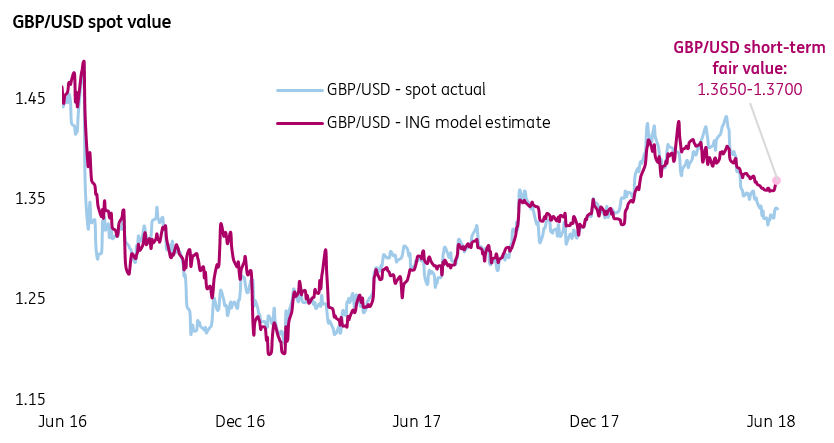

While a tricky summer of Brexit politics lies ahead, with May facing an impossible Brexit trinity, the pound still remains a good long-term value play. Our current forecasts continue to look for sterling to navigate towards levels consistent with a ‘neutral’ Brexit later this year (GBP/USD: 1.43 and EUR/GBP: 0.86)* – with the near-term balance of risks tilted towards GBP/USD moving back towards 1.36 (200-day moving average).

*These remain under review – and we will address GBP's longer-term direction in a note later this summer.

GBP/USD trading with a 2-3% short-term Brexit uncertainty premium

Current GBP price action indicative of a 'muddling through' Brexit risk premium

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more

Included in the following bundle

In Case You Missed It: Confidence and cracks

- This bundle contains 7 Articles