GBP: More narratives than Game of Thrones

- 31 July 2017

- FX

Expect a more confusing narrative at the August BoE meeting than a Game of Thrones episode, though only a clear dovish message would weigh on the pound

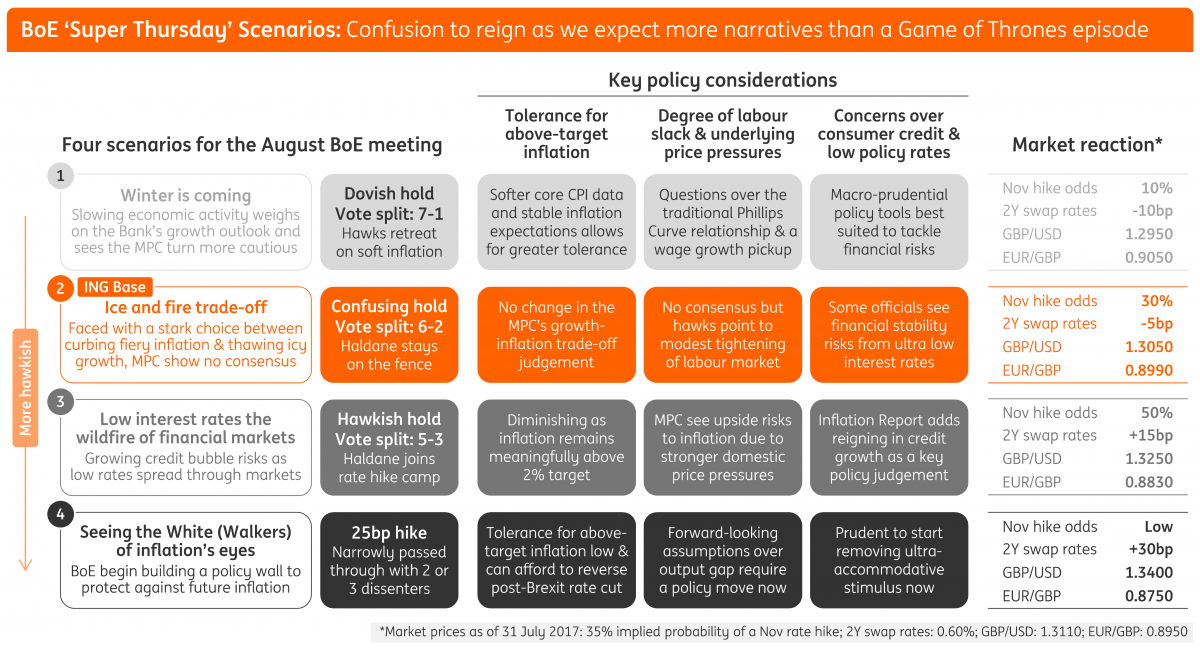

Four BoE August 'Super Thursday' scenarios

Four signals GBP markets will be watching out for

Signal 1: How close are the MPC to hiking rates?

Our base case is for the MPC to keep rates on hold this week with a 6-2 split vote (McCafferty and Saunders dissenting). This should be a neutral to slightly negative outcome for GBP; despite the OIS curve pricing in little chance of a rate hike this week, recent BoE talk means that markets are going into the August Super Thursday meeting with a slightly hawkish bias and a vote split of only two active dissenters could be seen as a disappointment.

A 6-2 MPC split vote will be a neutral to slightly negative outcome for GBP

Admittedly, we don't see our central scenario meaningfully weighing on GBP given that (a) it is the most probable outcome and (b) policy signals elsewhere, most notably the meeting minutes, are likely to raise prospects of 'silent hawks' - that is one or two MPC officials who were close to voting for a hike this month.

Any deviation from a 6-2 vote split is likely to have a more lasting impact on GBP - with the risks fairly symmetric in the event of a dovish or hawkish surprise:

- A third dissenting vote - with Chief Economist Andy Haldane the most likely candidate - would heighten the debate over a November rate hike. With markets currently seeing a 34% chance of this occurring, a 5-3 vote split would add upward pressure to short-term UK rates and GBP.

- A 7-1 vote split - and either McCafferty or Saunders retreating given the recent softness in data - would be a dovish surprise for markets and is likely to push expectations of a Bank rate hike further out into 2018. This outcome would see GBP/USD fall to 1.2900 and EUR/GBP breach 0.90 (moving towards 0.9050).

Signal 2: Is the tolerance for above-target inflation fading?

The key area of focus in the policy statement will be the language around the tolerance for above-target inflation and whether this has reduced or increased in the eyes of the MPC. Both the softer core inflation print this month and declining trend in market-based inflation expectations suggest that the majority of the MPC should have a greater tolerance for above-target inflation - at least relative to the prior meeting. Any softening of language over the MPC's inflation concerns will be perceived as a dovish signal and is likely to weigh on GBP - though, in reality, we are unlikely to see any real consensus here.

Signal 3: Will the Quarterly Inflation Report (QIR) introduce a new policy risk?

The recent run of data in the UK means there are slight downside risks to the 2017 growth and inflation projections made in the May QIR. However, in the absence of any wholesale changes, this is unlikely to be new news for GBP markets - which have to some extent already priced in a softer near-term economic outlook. The BoE currently sees NAIRU at 4.5% and while the latest jobs report saw the unemployment rate reach this figure, we do not anticipate any major changes to the Bank's assumptions over the degree of labour market slack. Indeed, doing so would inadvertently have consequences for the (optimistic) outlook for wage growth that is partly underpinning the hawkish BoE sentiment.

One possible hawkish tail risk that we could see emerge from the Aug QIR is if financial stability concerns over persistently low interest rates were added to the MPC's list of key judgements. The May QIR briefly touched on this idea and while the current approach from the Bank has - rightly so - been to use the FPC toolkit to address any financial vulnerabilities, some MPC officials may see growing leverage risks as another reason to start removing the ultra-accommodative monetary stimulus.

Signal 4: Will we get an emerging consensus in the MPC minutes?

Most probably not. The minutes are likely to serve best at highlighting the current dichotomy within the MPC; the range of views on show - and little consensus on key policy judgements - means that we expect markets to remain confused over the Bank's near-term policy bias. There will be enough for both the market doves and hawks to cling onto and the lack of clarity means that a 30-35% chance of a November rate hike is likely to remain in place - which will ultimately leave GBP directionless.

GBP outlook: BoE policy confusion to render markets directionless

Status quo from the BoE this week - and a lack of emerging consensus over how best to address the growth-inflation trade-off - is unlikely to have a major impact on short-term UK interest rates or the near-term outlook for the pound. While some of the recent hawkish sentiment may fade as a result of the Bank showing little appetite for a policy change, we suspect that only a formal ruling out of a 2017 rate hike by Governor Carney - if explicitly asked in the post-meeting press conference - would have a sustained negative impact on GBP. We see this as highly unlikely given that BoE officials will probably want to keep all policy options on the table.

GBP/USD: Recent rally more dollar weakness, less sterling optimism

- The move above 1.30 has been supported by a narrowing of UK-US rate differentials, though much of the heavy-lifting has come from fading Fed rate hike expectations - as opposed to greater market confidence over a BoE hiking cycle.

- Our short-term financial models show GBP/USD fairly priced around the 1.3100-1.3150 area meaning that it should be fairly responsive to a dovish or hawkish BoE surprise this week. Neutral positioning - with short GBP bets still hovering around their lowest since Brexit - also suggests greater two-ways risks.

- We still retain a mildly bearish outlook for GBP/USD over 3Q17. A US data-driven recovery in the markets' outlook for Fed policy should see the USD sentiment recover from its current lows, while it may take another layer of bad US political news to take the USD another leg lower. Any recovery in the USD will be most pronounced against those currencies where there are clearer signs of monetary policy divergence; a more cautious approach from the BoE this week could mean that GBP/USD is one of the crosses where we see greater downside potential in a recovering dollar market.

EUR/GBP: 90s Throwback?

- A more dovish-than-expected BoE message this week could see EUR/GBP test the psychological 0.90 level. Under our central scenario of policy confusion, however, we think there will be little dovish momentum to take us beyond here; in the absence of Bank officials playing down prospects of a near-term rate hike, we suspect EUR/GBP bulls will have little new information to work with.

- The tailwind of a stronger EUR - driven by ECB QE tapering expectations - has kept the pair honest around current levels. After widening to around 83.5bp in late June, UK-EZ 2-year swap rate differentials have narrowed to 75bp over July and this is consistent with a modest rise in EUR/GBP towards 0.89.

- We continue to forecast EUR/GBP at 0.90 in 2H17 - although we do see growing risks of a near-term overshoot. A more cautious ECB - as well as progress towards a Brexit transition deal later this year - are why we think a sustained move beyond 0.90 looks unlikely at this stage.

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more