GBP: Markets not convinced that Brexit will be alright on the night

- 29 October 2018

- FX United Kingdom

GBP will stay highly sensitive to Brexit headlines – with the balance of political risks and market positioning meaning rallies will be met with profit-taking and caution, while dips will be bought on big picture hopes that a Brexit no-deal crisis will be averted. GBP is cheap but investors will need to assess whether Brexit makes it justifiably cheap

They think it's all over... but it's not quite

While a buoyant pound had been heading into the October EU summit trading on sentiment that a Brexit Withdrawal Agreement was almost done – GBP bulls may have to put the champagne back on ice. There's still a long way to go.

It’s not a disaster for the pound if we don’t get an early Brexit deal, although it will undoubtedly raise questions over the stability of the UK government – and the degree of political risk premium that needs to be priced into GBP assets in the near-term. Indeed, the risks of a political miscalculation by the UK or EU – or some sort of negative turn in UK politics (DUP voting down the Tory budget or Brexiteers triggering a vote of no confidence in the Prime Minister) are growing.

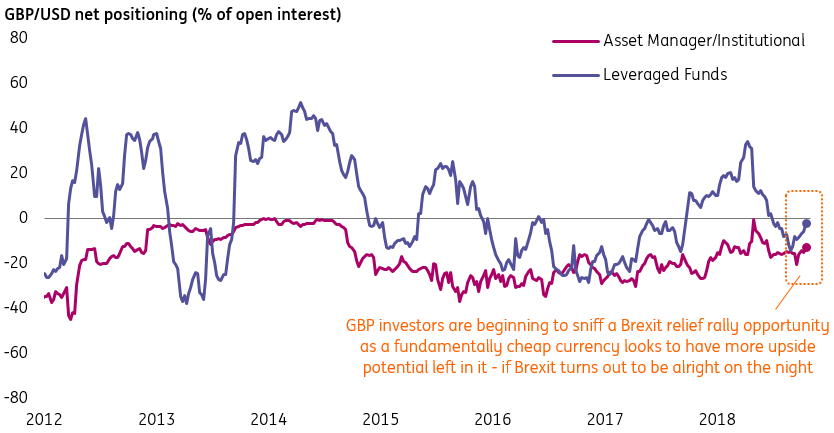

GBP positioning update: Leveraged funds sniff a bullish opportunity

Two tests for whether a Brexit deal can see a sustainable GBP rally

But a lot of bad news is priced in. Speculative short GBP positioning and the premium for hedging GBP downside highlights the degree of scepticism still in markets over the ability to get a Brexit deal over the line – not least with the Salzburg disappointment fresh in investors’ minds and the seemingly trivial, yet significant, UK political hurdles that still need to be overcome.

The agreement of an exit deal between the UK and EU – which requires both a solution on the Irish border backstop and a high-level political declaration on the future trade deal – might not be enough to see GBP rally on a sustainable basis. We think any deal announced would need to stand the following test for GBP to hold onto further gains:

- The deal is able to command a majority within the UK parliament

- The high-level future trade agreement doesn’t tie the UK to an obvious hard Brexit trade deal

It’s the former that will be the main challenge – with the DUP (and Tory Brexiteers) not quite on the same page as Prime Minister Theresa May when it comes to the Irish border backstop issue.

Extent of sterling's Brexit relief rally depends on how quickly a deal gets done

Scenario 1 – Hopes of an Early Brexit Deal (Oct/Nov): Any announced exit deal over the next few weeks that also meets the above two tests would see markets all but fully price out the risks of a no-deal Brexit – thus fuelling further bullish GBP momentum. We target GBP/USD moving to 1.34-1.35 (to the 200-day moving average) in the coming months – with a potential overshoot to 1.37-1.38, if external geopolitical risks (Italy, emerging market rout, US-China trade tensions) fade and the USD weakens heading into the US midterms.

Scenario 2 – Hopes of a Late Brexit Deal (Nov/Dec): The longer the impasse goes on, the more nervous GBP markets are likely to get – and so we should expect short positions to build with time. But with risk-reward favouring greater GBP upside potential, we still think a buy-on-dips strategy will be the preferred tactic for value chasing investors.

Scenario 3 – Impasse in November: If there are still doubts about whether a Brexit deal could get through UK parliament – or no big announcement by late November – we could see GBP/USD falling back to 1.27-1.28 (EUR/GBP 0.90). This is not our central scenario - although markets have in recent weeks drifted towards this sentiment given the lack of headline Brexit progress.

Summary: GBP's state of flummox presents an opportunity

GBP remains in its usual state of flummox as the Brexit impasse continues, with politics at home the biggest stumbling block. Until this is resolved, we expect GBP/USD to trade below 1.30. GBP/USD trading 2 big figures below the ‘neutral’ sentiment level of 1.30 presents a good opportunity to buy GBP again – if one believes that Brexit will, in fact, be alright on the night. We see GBP/USD’s short-term gravitational pull at 1.35-1.36 on a Brexit deal being reached this side of Xmas.

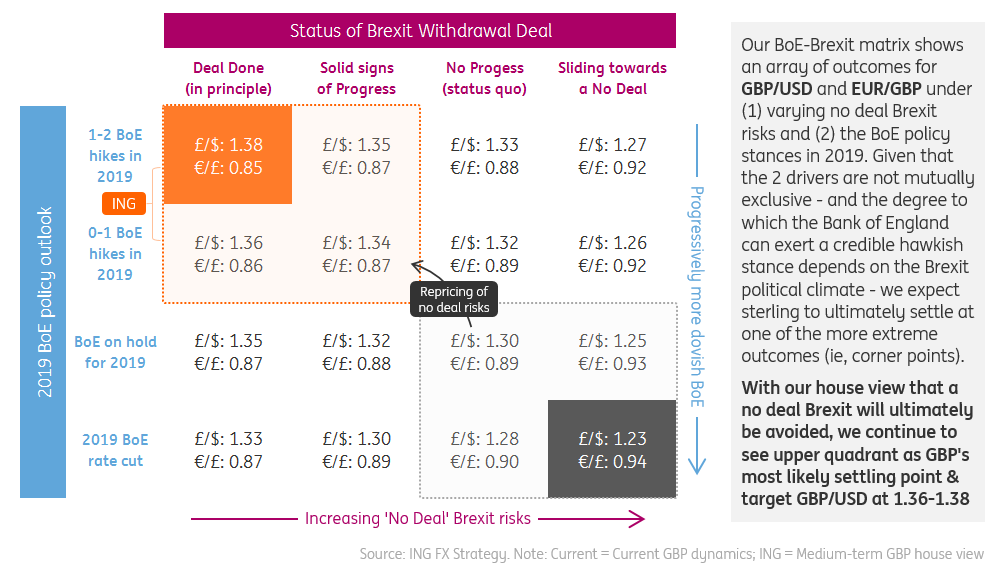

GBP's Binary 2019 Outlook - Brexit and Bank of England drivers interlinked

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more