G10 FX Week Ahead: The Dollar’s Hocus POTUS

- 20 July 2018

- FX United States

The markets' love for the US dollar was abruptly ended by a series of comments by President Trump on US interest rates and currencies. With the short-term USD fundamental dynamics starting to turn lower, these comments mark the end of the USD rally – and bar any immediate escalation the global trade war, it’s a mini-lifeline for currencies elsewhere

Source: Shutterstock

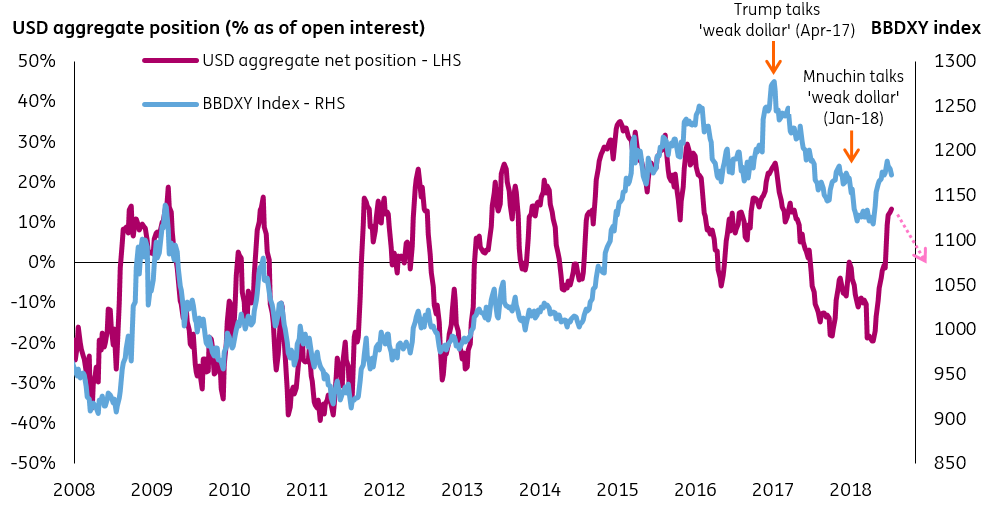

Trump jawboning could see USD longs clear out

Source: ING, Bloomberg, CFTC. Note: Positioning data as of 10 July 2018

EUR: Trump providing some respite to EUR/USD

| Spot | Week ahead bias | Range next week | 1 month target | |

|---|---|---|---|---|

| EUR/USD | 1.1700 | Mildly Bullish | 1.1530 - 1.1850 | 1.1700 |

- Yet again, President Trump's comments have shaken the FX ground. His criticism of (a) China and EU for manipulating the exchange rates; and (b) the Fed for hiking interest rates reversed the some of the USD strength (which has been in a great part generated by President Trump and his trade policies/wars to start with) and is likely to put some floor under EUR/USD (and in the absence of the escalating trade wars be also supportive for EM FX).

- On the data front, the expected strong 2Q US GDP figure (on Friday - our economists look for 4% QoQ annualised) should provide some support to the dollar following Trump induced USD weakness. We expect the July ECB meeting (Thu) to be a non-event for the euro as the ECB already provided a guidance on QE and deposit rates in June. We expect EZ July PMI (Tue) and German Ifo (Wed) to remain largely unchanged, thus suggesting a limited impact of trade tensions on the sentiment. We see a modest upside risk to EUR/USD particularly in the first part of the week as Trump induced negative USD sentiment continues.

JPY: Brought back to life by a mercantilist Trump

| Spot | Week ahead bias | Range next week | 1 month target | |

|---|---|---|---|---|

| USD/JPY | 111.80 | Mildly Bearish | 110.50 - 112.80 | 110.00 |

- The negative yen drivers look to be in reverse - with President Trump sparking renewed USD weakness that has also seen the US yield curve steepen (not flatten). But equally on the domestic Japanese front, reports that the Bank of Japan may discuss changes to its current policy settings at its 31 July meeting - and in a way that leads to a de facto policy tightening - also helped to drive USD/JPY below the 112 level (after reaching a high of 113.15/20 earlier in the week). In the absence of any major positive US data surprises, we see room for USD/JPY to move significantly lower as long USD (short JPY) positions neutralise. We think we've seen a top in USD/JPY for now - with risks tilted towards 110 over the coming weeks.

- Indeed, Trump’s comments about interest rates and the dollar may see investors reluctant to chase USD/JPY much higher above 114-115 – or at least see Japanese investors think twice about investing in US assets unhedged. Should the global trade war escalate from here, we would expect the yen to revert back to its typical safe-haven nature. A broader sell-off in global stocks would see one-way JPY repatriation flows – thus reigniting a bearish USD/JPY trend back towards the 105-108 area.

GBP: Short-term downside risks as politics to outweigh economics

| Spot | Week ahead bias | Range next week | 1 month target | |

|---|---|---|---|---|

| GBP/USD | 1.3110 | Neutral | 1.3000 - 1.3250 | 1.3000 |

- All the drivers for the pound have turned on their head – with a strong dollar (weak global economy), domestic political uncertainty and a muted UK economic cycle all weighing on the pound. We think the stormy political clouds over Westminster will remain in place until at least October – and are thus confined to pencilling in a 1.27-1.28 trough for GBP/USD at some point in 3Q18 (EUR/GBP at 0.92).

- This near-term downgrade accounts for a significant degree of political uncertainty – and is in spite of the Bank of England raising rates in August. While we could be positively surprised by the Brexit progress, we feel the balance of risks suggests that further uncertainty is more likely between now and October – so long as the UK government's Brexit strategy remains one that is seemingly trying to fit a square peg into a round hole. A weak USD may see GBP/USD consolidate in the low 1.30s - but watch out for EUR/GBP potentially testing 0.90 should we see any negative Brexit headlines (note the UK Parliament will be in summer recess from Tuesday).

AUD: Fading external headwinds may provide temporary relief

| Spot | Week ahead bias | Range next week | 1 month target | |

|---|---|---|---|---|

| AUD/USD | 0.7410 | Mildly Bullish | 0.7300 - 0.7500 | 0.7200 |

- The key domestic event in the week ahead will be the 2Q Australian CPI report (Wed); bar any meaningful inflation surprise - note markets are looking for core inflation readings to come in at 1.9%, which is still outside the RBA's 2-3% target range - we suspect there will be muted implications for AUD rates and the currency. External factors will dominate AUD sentiment and the current US policy mix is particularly toxic for the currency; higher US rates (due to a relentlessly hawkish Fed) and sliding industrial metal prices (a by-product of the US-China trade war) is weighing heavily on the currency – keeping AUD/USD anchored below 0.75. While we may see a near-term short AUD squeeze, our view of a further escalation in the global trade war narrative means that we have a big picture negative outlook on high-beta FX. We continue to cite risks of AUD falling to 0.70 if the US follows through with US$200bn Chinese import tariffs.

- An additional source of market risk for APAC FX is Chinese yuan (CNY) weakness. What's catching markets by surprise is the willingness of the PBoC to let market forces prevail in CNY markets; however, with a large chunk of USD/CNY's move higher due to a strong dollar - and that trend likely nipped in the bud for now - we could see a period of stability in USD/CNY. This sentiment will be reflected in APAC FX - including the China trade-sensitive AUD. We're still looking for AUD/USD to stabilise in the 0.73-0.75 range over the coming months.

NZD: All set up for a period of tactical outperformance

| Spot | Week ahead bias | Range next week | 1 month target | |

|---|---|---|---|---|

| NZD/USD | 0.6800 | Mildly Bullish | 0.6700 - 0.6930 | 0.6900 |

- The fundamental NZD outlook turned slightly favourable this week after the RBNZ’s core inflation measure (sectoral factor model) moved up to 1.7% YoY in 2Q18 (which is a 7-year high). The positive inflation surprise coupled with a flat NZD OIS curve (limited RBNZ tightening sentiment), short NZD/USD speculative positioning at 5-year lows, signs that the USD may be turning lower and a potential pause in trade war risks means that we see room for short-term tactical NZD outperformance. But given the volatility and uncertainty of US trade policy - and the potential for an escalation in the global trade war narrative - we prefer to play NZD strength against AUD and CAD (both more vulnerable to US tariffs).

- It's a quiet week ahead for local data - we'll get June trade figures (Wed) and July consumer confidence (Fri). Look for NZD/USD to potentially climb up towards 0.69-0.70 if the risk relief rally continues and key US data misses in the week ahead.

CAD: Looking particularly chirpy all of a sudden

| Spot | Week ahead bias | Range next week | 1 month target | |

|---|---|---|---|---|

| USD/CAD | 1.3135 | Mildly Bearish | 1.3000 - 1.3220 | 1.3000 |

- Solid Canadian retail sales and a positive domestic CPI surprise - coupled with broad USD weakness following President Trump's jawboning - has seen USD/CAD move away from its 1.32-1.33 highs. There's a good chance that the Bank of Canada hikes again later this year (odds of this have picked up to around 64%) - but we may need to see external headwinds (US trade risks) fade, while domestic data needs to continue to print constructively. The Canadian calendar is particularly light in the week ahead.

- In terms of NAFTA, progress continues to stagnate; there’s an element of CAD markets giving up hope and expecting the worst (short USD/CAD positions are at their highest in over a year). While we believe the pair is overvalued on a short-term basis above 1.32-1.33, we may need to see some positive NAFTA news to see a corrective move below 1.30. Worth noting that the lack of Saudi oil exports in August may help to keep crude prices (and CAD) bid over the coming weeks.

CHF: Little reaction to Trump comments

| Spot | Week ahead bias | Range next week | 1 month target | |

|---|---|---|---|---|

| EUR/CHF | 1.1650 | Neutral | 1.1580 - 1.1720 | 1.1600 |

- CHF exerting a rather limited reaction to the President Trump’s comments on USD and the Fed and the long/short franc trade being more about the trade wars (as is the case for SEK, though with different reaction to rising / falling risk of trade wars vs CHF) rather than the US interest rates or the general dollar behaviour. With the trade war factor still in play, there is limited reason for meaningful franc reaction.

- The Swiss economic data should continue to exert a limited impact on CHF, with June Money supply data and SNB sight deposit having no effect on the franc. With the ECB July meeting being a non-event, EUR/CHF should stay in the 1.1600-1.1700 area.

SEK: The last beneficiary from the Trump induced FX rally

| Spot | Week ahead bias | Range next week | 1 month target | |

|---|---|---|---|---|

| GBP/USD | 10.3850 | Neutral | 10.2850 - 10.4750 | 10.5000 |

- President Trump's comments induced rise in higher beta currencies may be only modestly supportive of SEK. This is because the risk of escalating trade wars is still in place (making SEK vulnerable) while the rising EUR/USD doesn’t have to translate into a stronger SEK (which was not the case in 2017 either) given the inherently dovish Riksbank, the feeble underlying inflation pressures and the negative SEK carry.

- We expect EUR/SEK to remain around the 10.40 level next week. The domestic data (July Economic Tendency Survey on Thu and June retails sales on Fri) are unlikely to cause a sharp moves in SEK.

NOK: Some stability following the fall

| Spot | Week ahead bias | Range next week | 1 month target | |

|---|---|---|---|---|

| EUR/NOK | 9.5900 | Neutral | 9.5100 - 9.6780 | 9.4500 |

- It is a very quiet week on the Norwegian data front (May unemployment rate expected to remain at 3.7% - Thu) suggesting that EUR/NOK should remain primerily driven by (a) the general risk sentiment (b) the oil price. the latter has been the key driver behind the recent EUR/NOK rise to the 9.6000 level.

- Should the softer USD ease the latest decline in the oil price, this should put a lid on the EUR/NOK rise too, particularly in the context of the hawkish Norges Bank which signalled the September hike.

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more