G10 FX Talking: Waiting on evidence of disinflation

- 12 June 2023

- FX Talking

Central bankers are yet to sound the 'all clear' on inflation. This threatens high rates, inverted yield curves and a strong dollar for longer. For the time being, however, we stick to the view that the Fed will have enough information to drop its hawkish stance in the third quarter - and that the dollar will embark on a multi-year bear trend

Source: Shutterstock

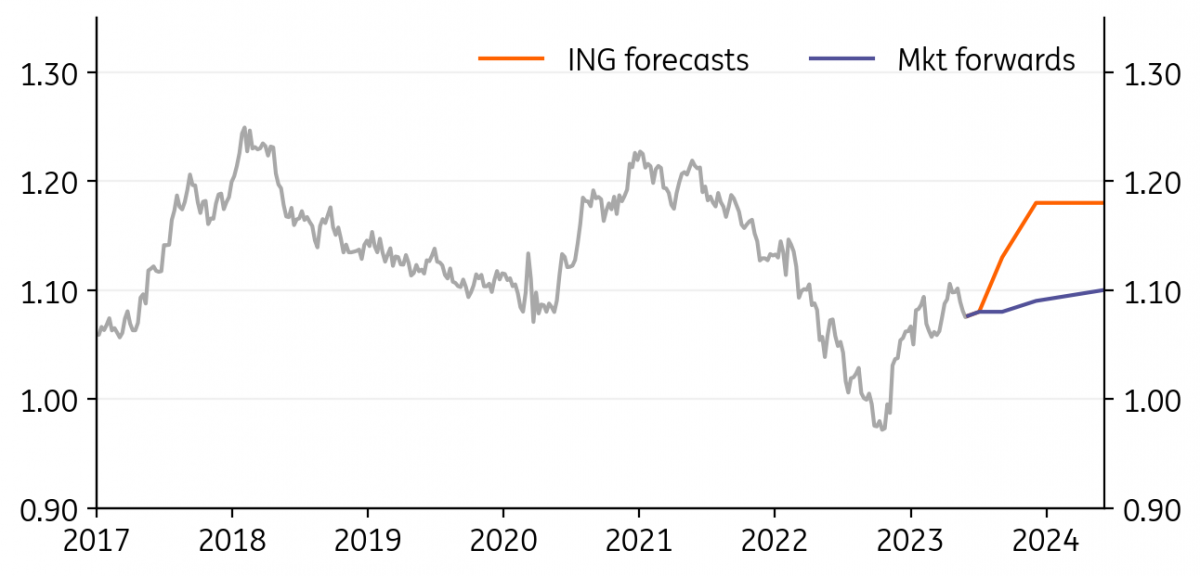

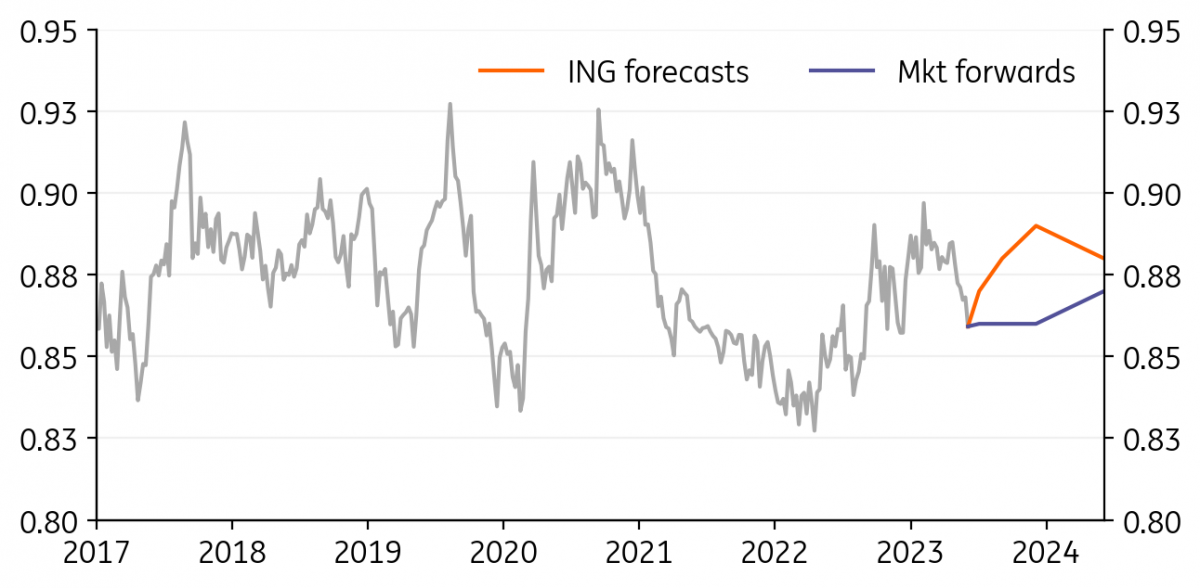

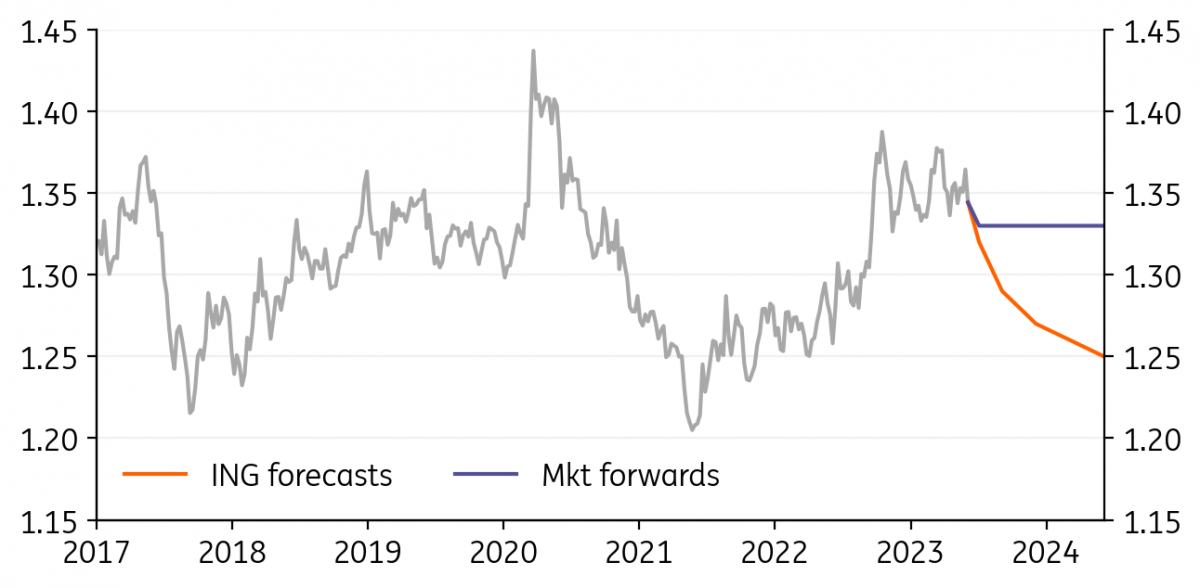

EUR/USD: Waiting for the US disinflation shoe to drop

|

Spot

|

One month bias | 1M | 3M | 6M | 12M |

|---|---|---|---|---|---|

|

EUR/USD

1.0771

|

Neutral | 1.08 | 1.13 | 1.18 | 1.18 |

- Like many other central banks around the world, the Federal Reserve’s inflation fight is ongoing, restrictive policy remains in place and the dollar remains relatively strong. In theory, tighter credit conditions from this year’s US regional banking crisis should help slow the economy – but there are no real signs of that yet.

- Our macro team cannot rule out one last Fed hike this summer, but still forecasts the start of sharp Fed rate cuts in 4Q. And over coming months there should be much clearer signs of US disinflation – data which should weigh heavily on the dollar.

- Our view is that 1.05/1.07 proves the base for EUR/USD, before softer US rates allow EUR/USD to rally to. 1.15+ by year-end.

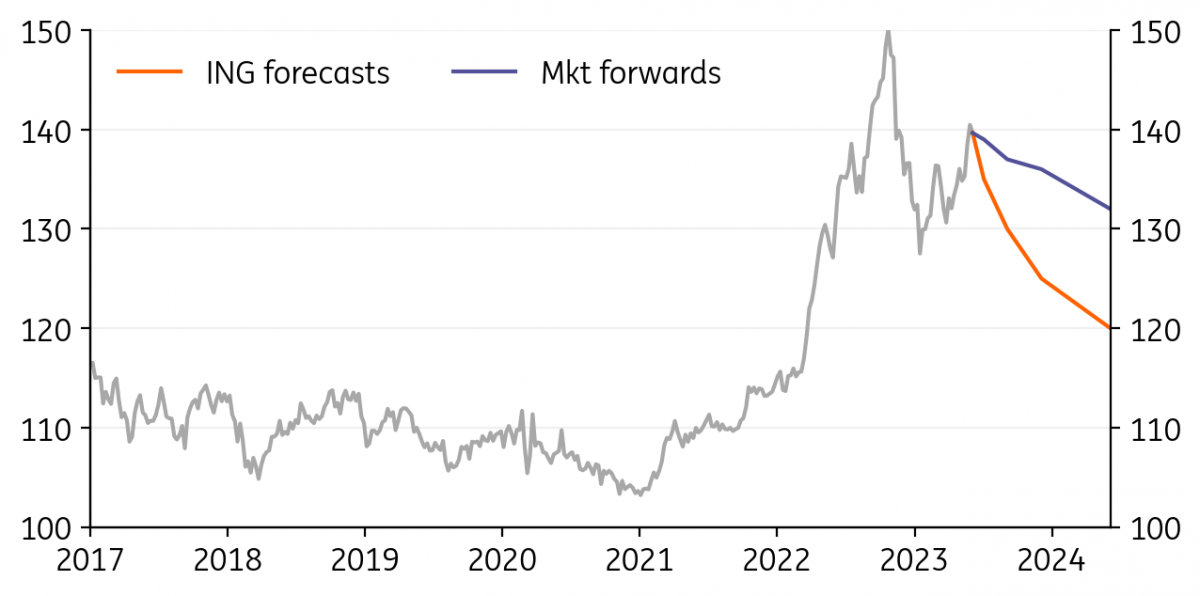

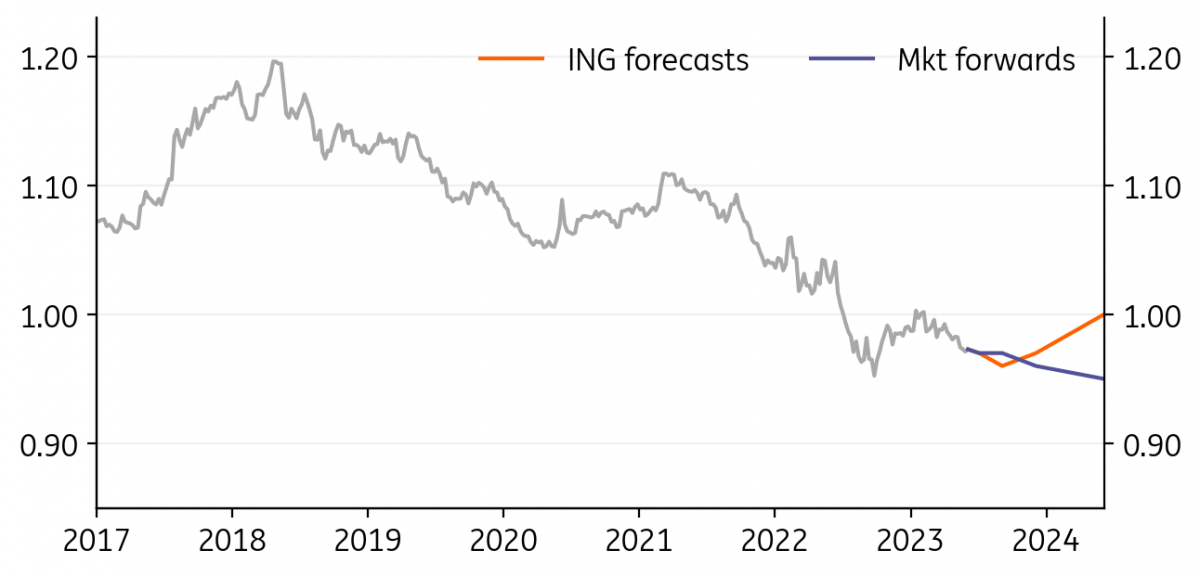

USD/JPY: Moving back into the FX intervention zone

|

Spot

|

One month bias | 1M | 3M | 6M | 12M |

|---|---|---|---|---|---|

|

USD/JPY

139.47

|

Bearish | 135.00 | 130.00 | 125.00 | 120.00 |

- In moving above 140, USD/JPY sparked the ire of Japanese officials again. Recall that FX intervention started at the 145 level last September. The problem for local officials is that: a) the dollar remains strong and b) low market volatility favours the carry trade, where the yen is by far the preferred funding currency.

- The question is whether policy makers in Tokyo are prepared to ride out another summer of strength in USD/JPY – or will be prepared to take action.

- We think the market is under-pricing the risk of further normalisation in the Bank of Japan’s Yield Curve Control policy on 16 June. By the end of 3Q, the dollar decline should be underway.

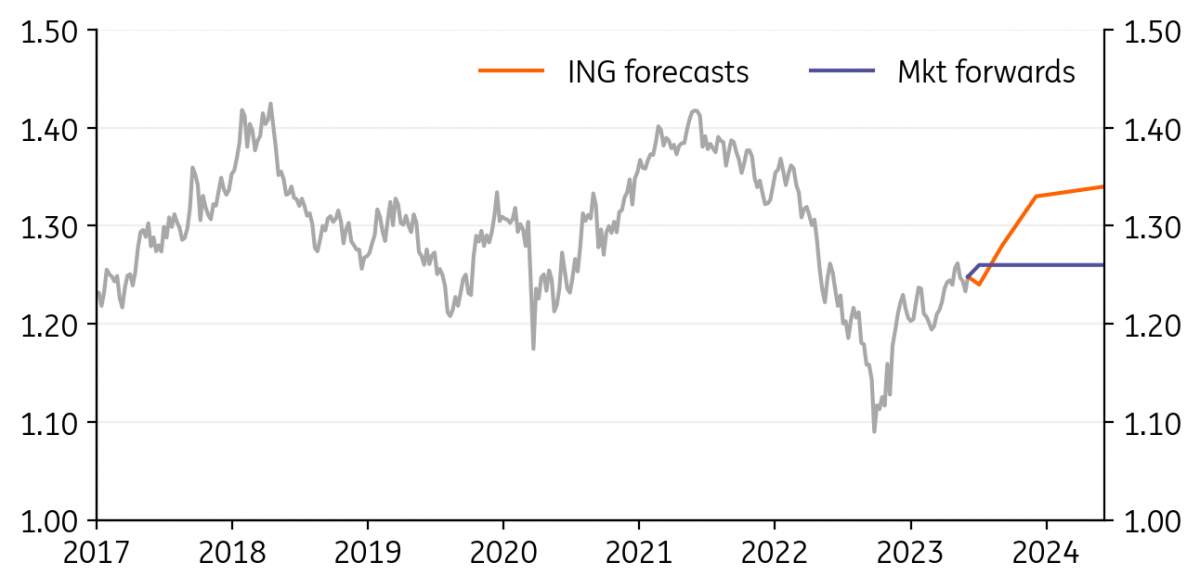

GBP/USD: Dragged higher by dramatic BoE expectations

|

Spot

|

One month bias | 1M | 3M | 6M | 12M |

|---|---|---|---|---|---|

|

GBP/USD

1.2591

|

Mildly Bearish | 1.24 | 1.28 | 1.33 | 1.34 |

- Somewhat amazingly, financial markets price the Bank of England Bank Rate at 5.50% for year-end – compared to 5.00% for the Fed funds. Sticky UK inflation has been the driver for this – and the BoE has adopted a strategy of saying very little.

- Our macro view is that the Bank Rate does not make it over 5.00% and that the market can be disavowed of its aggressive expectations by softer wage and price data over coming months.

- For GBP/USD that means slightly less help from the sterling side, but in what should be a weakening dollar environment. We see GBP/USD slowly grinding towards 1.30 this year – but suffering occasional setbacks when UK price data comes in soft.

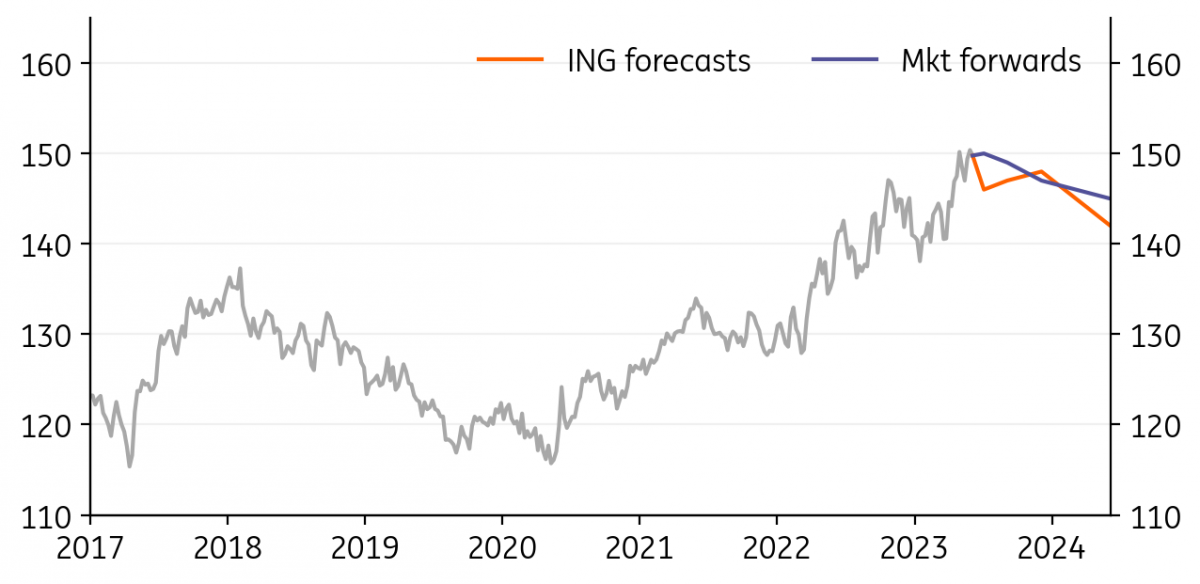

EUR/JPY: The risk asset sell-off that never was

|

Spot

|

One month bias | 1M | 3M | 6M | 12M |

|---|---|---|---|---|---|

|

EUR/JPY

150.28

|

Bearish | 146.00 | 147.00 | 148.00 | 142.00 |

- Many of us are surprised that the US regional banking crisis in March – amid tighter liquidity conditions in general – did not trigger a broader sell-off in risk assets. This has allowed EUR/JPY to push back up to 150. Any signs of US disinflation would allow risk assets to stay bid for longer, keeping EUR/JPY bid.

- For the European Central Bank, we and the market look for two more 25bp hikes (June and July) taking the deposit rate to 3.75%. Our team also looks for the first ECB cut in 2Q24.

- Unless some financial crisis emerges, it now looks like EUR/JPY can stay stronger for longer. Alternatively, some independent BoJ tightening would have to be the bearish game changer here.

EUR/GBP: Sterling comes in from the cold

|

Spot

|

One month bias | 1M | 3M | 6M | 12M |

|---|---|---|---|---|---|

|

EUR/GBP

0.8558

|

Bullish | 0.87 | 0.88 | 0.89 | 0.88 |

- Apart from the much higher yields now available in sterling deposits, it is hard to find many more supportive factors for sterling. True, Prime Minister Rishi Sunak seems to be engaging more with Europe, but UK economic prospects still look soft. We have full year 2023 growth at just 0.3%.

- The UK economy also faces a mortgage time-bomb, where 650,000 mortgage holders are due to refinance over the next six months at rates 400bp higher than their existing deals. The hit to consumption and house prices should weigh on sterling.

- We have been fighting this sterling strength for a while, but we cannot see a strong case for EUR/GBP to trade under 0.85.

EUR/CHF: SNB seems comfortable with softer EUR/CHF

|

Spot

|

One month bias | 1M | 3M | 6M | 12M |

|---|---|---|---|---|---|

|

EUR/CHF

0.9721

|

Neutral | 0.97 | 0.96 | 0.97 | 1.00 |

- In a world where central bankers are desperate for lower inflation, one might have thought the Swiss National Bank would be happy with core CPI dropping back below 2.0% year-on-year. But no, SNB President Thomas Jordan is still expressing concern about ‘second and third round’ effects from last year’s inflation spike. The SNB meet 22 June and are widely expected to hike rates 25bp to 1.75%. They will probably leave the door open for another 25bp hike in September.

- The SNB’s view on inflation is relevant for EUR/CHF since the SNB is happy to use CHF strength as a monetary policy tool.

- Intervening on both sides of the market to keep EUR/CHF heavily managed, expect it to stay offered near 0.96/97 for a while.

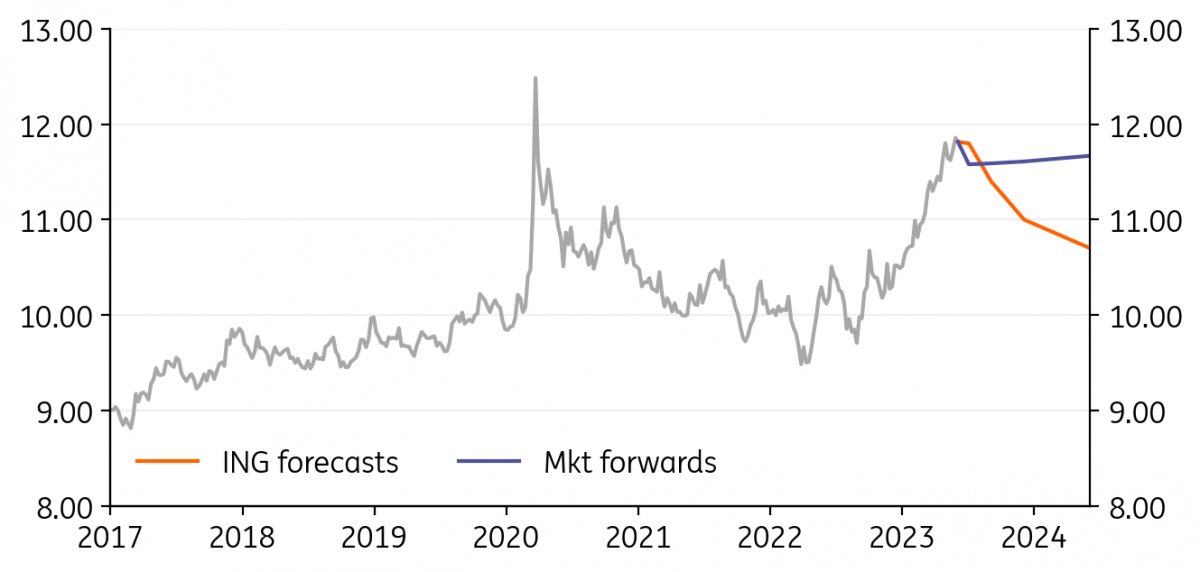

EUR/NOK: Norges Bank to step in with more hikes

|

Spot

|

One month bias | 1M | 3M | 6M | 12M |

|---|---|---|---|---|---|

|

EUR/NOK

11.578

|

Mildly Bullish | 11.80 | 11.40 | 11.00 | 10.70 |

- We were not expecting a rebound in NOK in the near term, and the krone has indeed remained under pressure throughout May and into early June.

- This means that Norges Bank will now likely need to step in with more tightening – we think to 3.75%, but don’t exclude 4.0% - especially considering FX rate purchases have remained relatively high at NOK 1.3bn daily in June and inflation has also rebounded.

- The threat of more Fed tightening argues against any snap rebound in the high-beta, illiquid NOK in the near term, but valuation and solid fundamentals can fuel a recovery initiated by NB hikes over the second half of 2023. A return to 11.00 is doable.

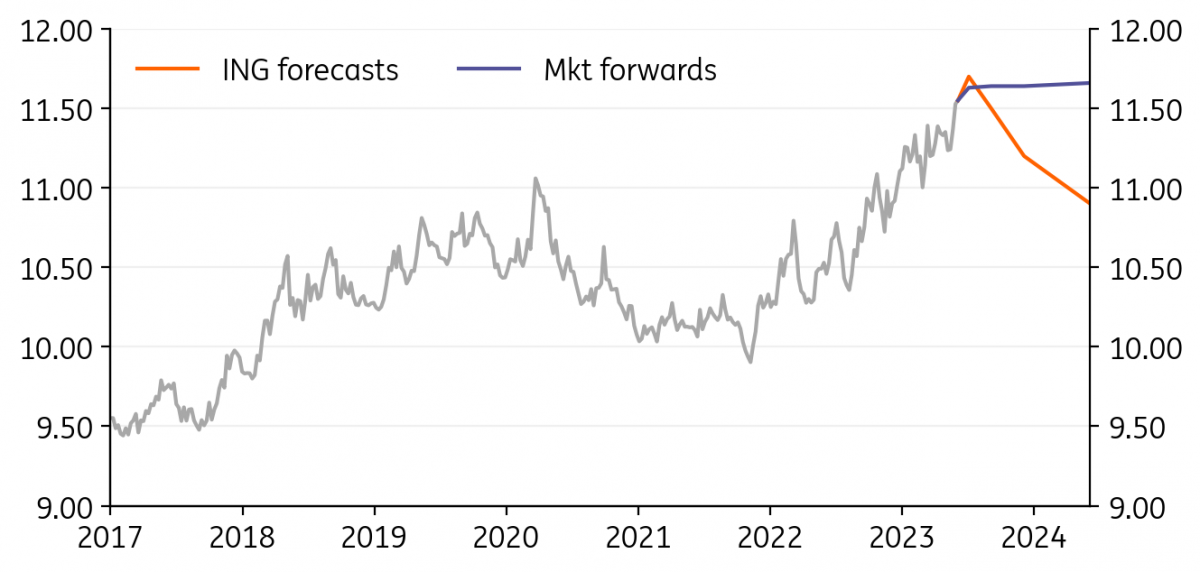

EUR/SEK: Riksbank’s communication incidents are no quick fix

|

Spot

|

One month bias | 1M | 3M | 6M | 12M |

|---|---|---|---|---|---|

|

EUR/SEK

11.631

|

Mildly Bullish | 11.70 | 11.50 | 11.20 | 10.90 |

- Except for verbally protesting SEK weakness, Riksbank members haven’t done much to rebuild confidence in the krona. The emergence of dovish dissent, admitting to a lack of tools to lift SEK and ruling out FX intervention even before testing the market’s reaction to this threat have left SEK vulnerable.

- On top of that, SBB (one of Sweden’s largest landlords) remains in very troubled waters, and markets may price more aggressively commercial real estate tail risks into SEK now.

- We think RB Governor Erik Thedeen will try to convey a hawkish message to support SEK at the end-June meeting, but the degree of dissent within the Board is unpredictable. SEK’s recovery almost solely relies on a benign turn in sentiment: this can happen in 2H23, but for now, SEK remains very vulnerable.

EUR/DKK: DN to follow the ECB with two more

|

Spot

|

One month bias | 1M | 3M | 6M | 12M |

|---|---|---|---|---|---|

|

EUR/DKK

7.452

|

Neutral | 7.45 | 7.46 | 7.46 | 7.46 |

- Danmarks Nationalbank refrained from intervening in the currency market for the fourth consecutive month in May.

- EUR/DKK traded marginally lower in the past month after April’s jump but has remained well clear of the bottom of the peg’s lower-bound, finding support at 7.4450. Crucially, EUR/DKK’s volatility has continued to decline from the February/March peak.

- We expect DN to hike rates by 25bp in June and July, in line with our ECB call. FX intervention should remain the primary line of defence for the peg, but higher policy rates naturally mean greater discretion on using the rate gap as a tool.

USD/CAD: Bank of Canada hikes keep loonie going

|

Spot

|

One month bias | 1M | 3M | 6M | 12M |

|---|---|---|---|---|---|

|

USD/CAD

1.332

|

Mildly Bearish | 1.32 | 1.29 | 1.27 | 1.25 |

- The Bank of Canada surprised with a rate hike in June, and we think another 25bp move in July is quite likely (60% priced in by markets). This is cementing CAD’s position as the currency with the best volatility-adjusted carry in G10.

- When adding the stabilisation in the domestic growth outlook and supported oil priced, a softening in the USD can easily trigger a break below 1.30 as early as this summer.

- We still expect a negative re-rating in US growth expectations later this year to hit the highly exposed CAD more than other pro-cyclical currencies, but the coincident drop in USD means that USD/CAD can end the year closer to 1.25 than 1.30.

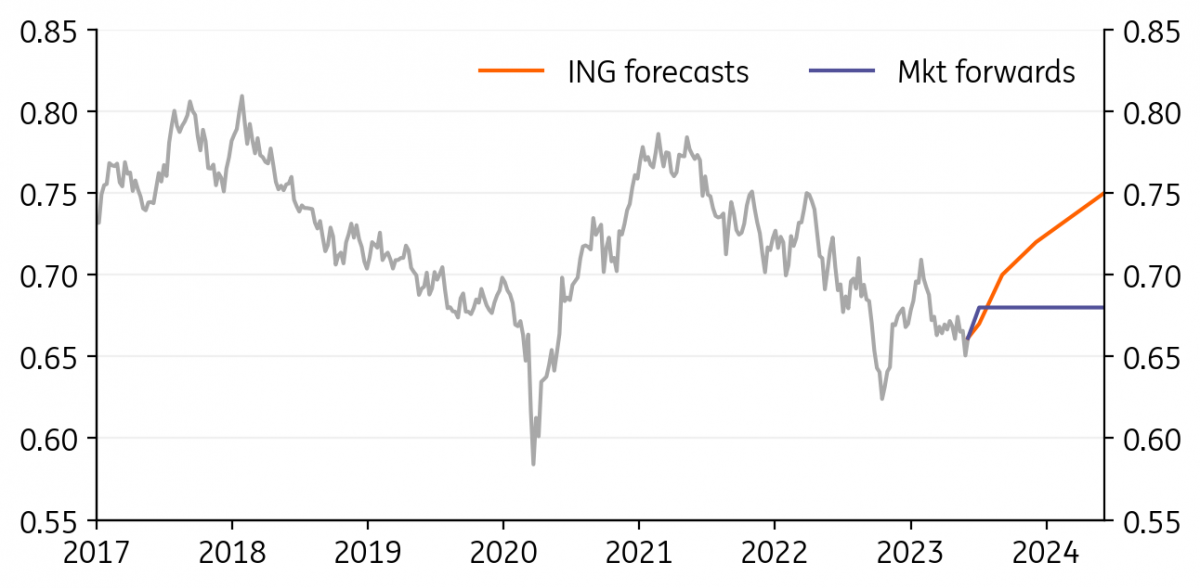

AUD/USD: The unpredictable RBA may be done with hikes

|

Spot

|

One month bias | 1M | 3M | 6M | 12M |

|---|---|---|---|---|---|

|

AUD/USD

0.6765

|

Neutral | 0.67 | 0.70 | 0.72 | 0.75 |

- A 4.10% peak rate for the Reserve Bank of Australia was our original call, but the path to this level was very tumultuous given data releases pointed firmly, and more than once, towards a pause in tightening.

- At the June meeting, the RBA turned a blind eye to grim jobs figures and focused on April’s inflation spike. Moving forward, we expect inflation to start declining at a faster pace, which should make the real policy rate less negative and ultimately mark the of end of the hiking cycle. Still, risks are firmly on the upside.

- Any data surprise will likely re-ignite hawkish bets and support AUD, which is already benefiting from news of stimulus in China and a recovery in iron ore prices. We target 0.72 by year-end.

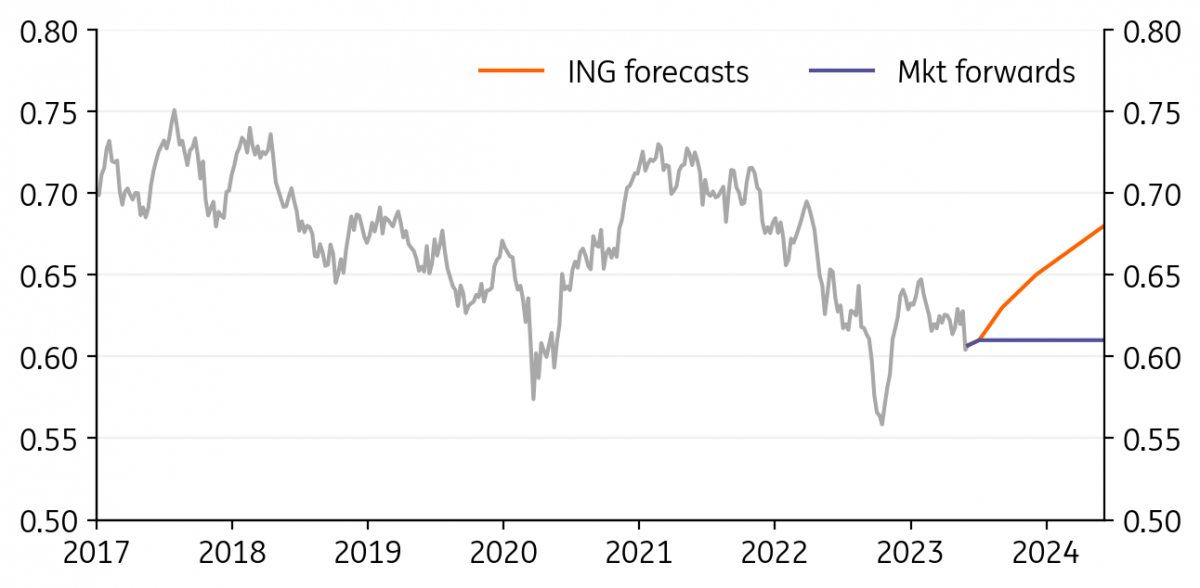

NZD/USD: RBNZ might not be done after all

|

Spot

|

One month bias | 1M | 3M | 6M | 12M |

|---|---|---|---|---|---|

|

NZD/USD

0.6137

|

Neutral | 0.61 | 0.63 | 0.65 | 0.68 |

- The Reserve Bank of New Zealand defied hawkish expectations at the May meeting, and despite the spending boost included in the latest budget and sharply rising migration, rate projections showed no more hikes.

- The latest round of tightening (Australia, Canada) and the risk of the RBNZ having underestimated inflationary risks mean another hike or even two by year-end cannot be excluded.

- The room for a hawkish repricing is quite large (only 10bp of tightening is in the price for now) but NZD can also be hit by more domestic tail risks – mostly related to the real estate market – than AUD, so we don’t see a strong bearish case for AUD/NZD. USD softening can take NZD to 0.65 by year-end.

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more