G10 FX Talking: Door opens to a weaker dollar

- 8 August 2025

- FX Talking

The large downward revisions to the US job numbers have undermined the Fed's position that the US labour market is 'solid'. The central bank can now have greater confidence that the summer uptick in inflation will be short-lived and restart its easing cycle this September. We expect the dollar to trend broadly lower into year-end and throughout 2026 as well

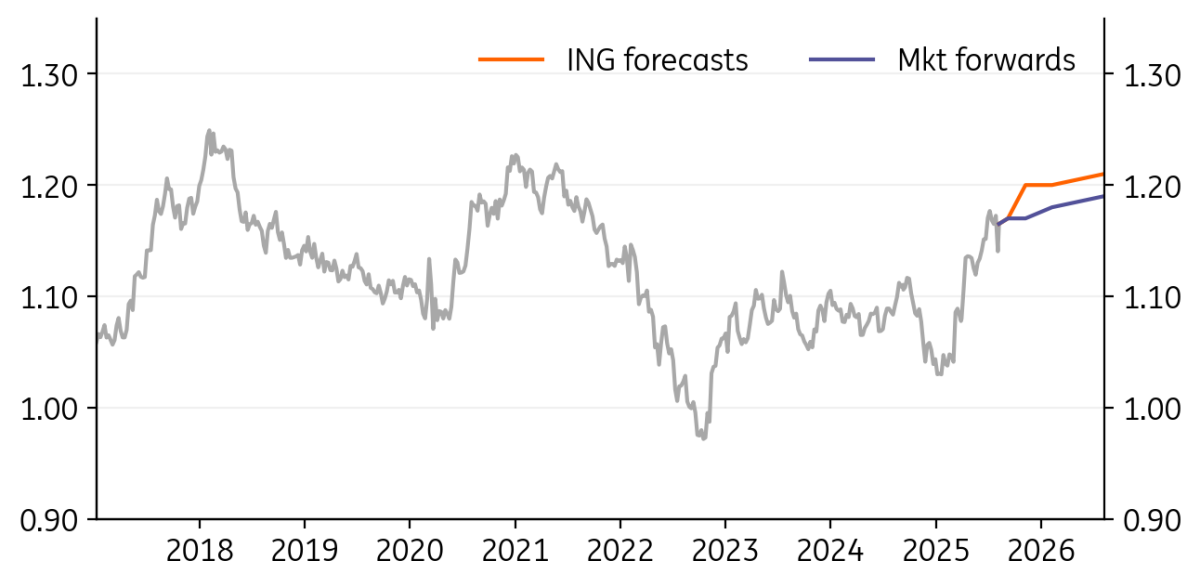

EUR/USD: Correction over

|

Spot

|

One month bias | 1M | 3M | 6M | 12M |

|---|---|---|---|---|---|

|

EUR/USD

1.1651

|

Mildly Bullish | 1.17 | 1.20 | 1.20 | 1.21 |

- The July US jobs report, especially the heavy back-month revisions, severely undermined the Federal Reserve’s position that the jobs market was ‘solid’. The Fed’s 21-23 August Jackson Hole event could now see the central bank formally swing behind policy easing. We now look for 25bp cuts at the September, October and December meetings.

- Lower short-dated US rates will now allow hedge ratios on US assets to be increased, and likely see the dollar trend lower for the rest of the year. Sticky US inflation might lead to brief, corrective dollar rallies, but these should be the exception.

- Risks to our bullish call from 1.20 mainly come from: a) a very dovish European Central Bank, or b) secondary sanctions on Russia, prompting a large sell-off in emerging currencies and a weaker risk environment.

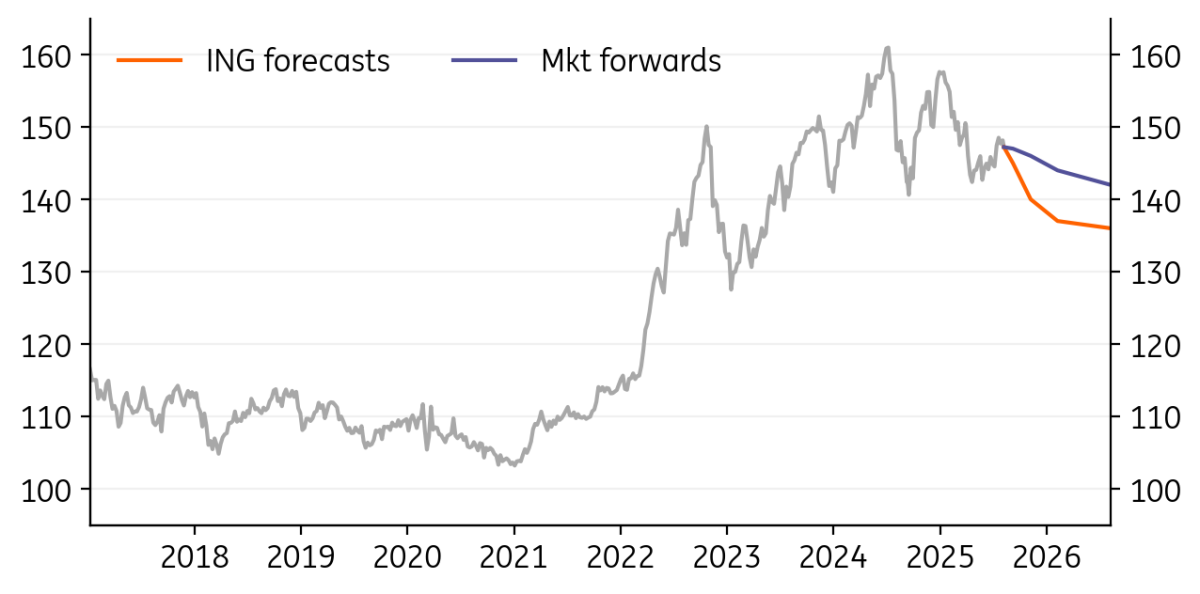

USD/JPY: BoJ hike in October should help the yen

|

Spot

|

One month bias | 1M | 3M | 6M | 12M |

|---|---|---|---|---|---|

|

USD/JPY

147.22

|

Bearish | 145.00 | 140.00 | 137.00 | 136.00 |

- USD/JPY fully participated in the jobs-triggered dollar sell-off last month, and those recent highs near 151 may be the best levels for many quarters to come. As the year progresses, expect attention to turn back to the Japanese domestic story, where looser fiscal policy and better domestic demand should give the Bank of Japan confidence to hike 25bp in October.

- In terms of trade, Japan’s deal with the US – especially 15% tariffs for the auto sector – is not seen as bad as others.

- Beyond the risks that sticky US inflation poses to our weaker dollar forecasts, we would add Prime Minister Shigeru Ishiba’s possible resignation and a new PM calling for the BoJ to go slow on rate hikes.

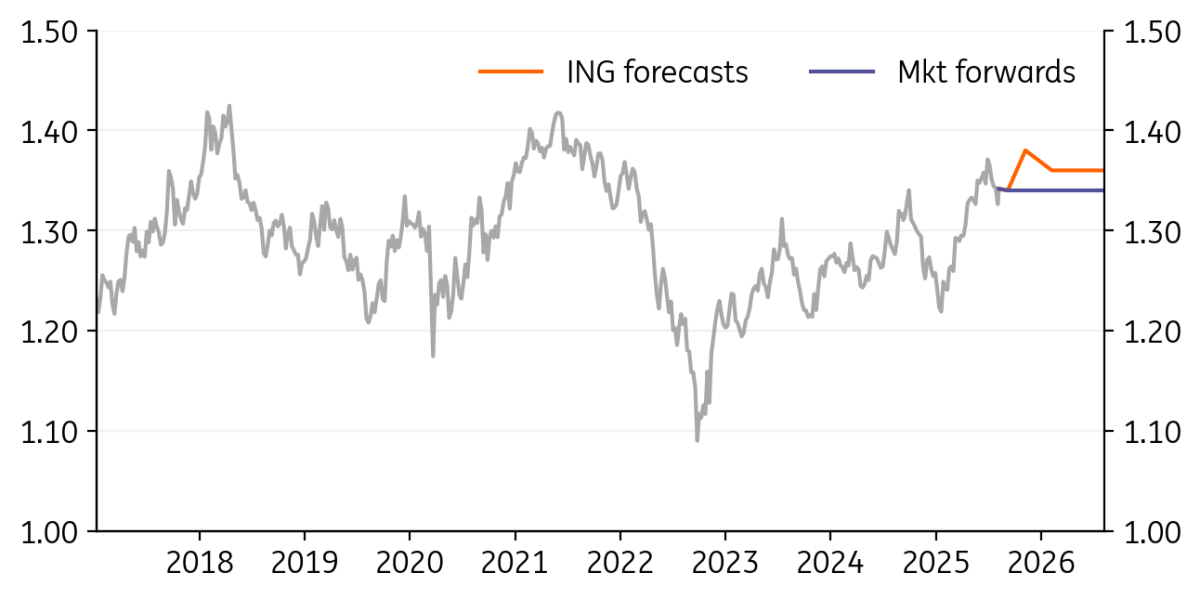

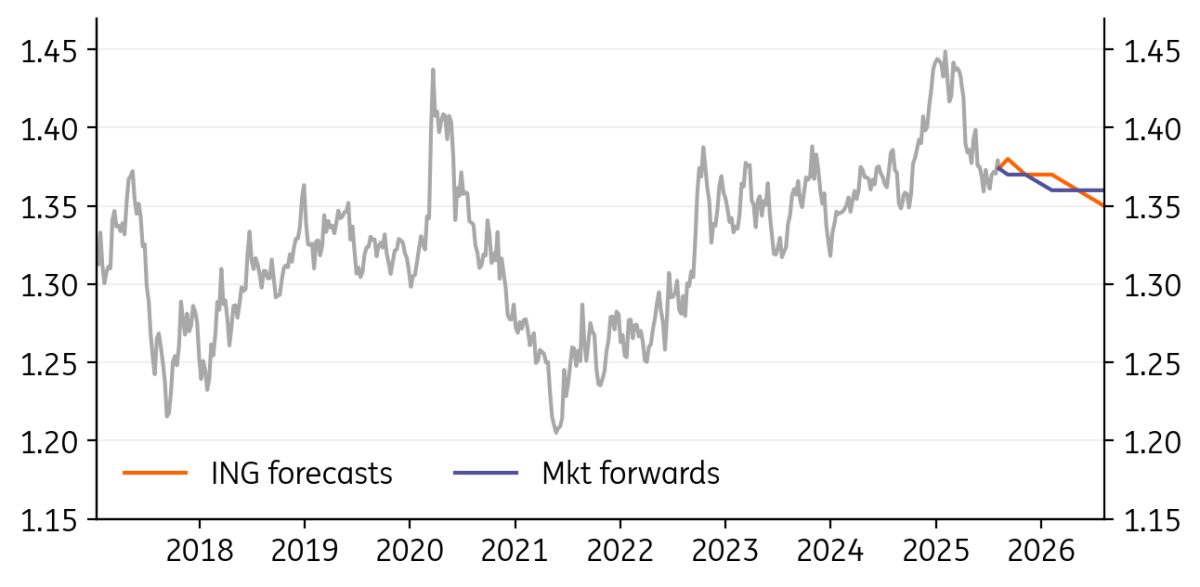

GBP/USD: Dragged higher by the dollar

|

Spot

|

One month bias | 1M | 3M | 6M | 12M |

|---|---|---|---|---|---|

|

GBP/USD

1.3417

|

Neutral | 1.34 | 1.38 | 1.36 | 1.36 |

- We’re bearish on the dollar into year-end and into 2026. GBP/USD may well lag a little, given the domestic story. Here, the fiscal situation in the UK remains tight and Chancellor Rachel Reeves needs to find a way to plug a £20-40bn hole in public finances at her next budget in November. Having ruled out hikes in the major taxes, her room for manoeuvre is quite limited, and any changes to the fiscal rules would be treated as a sterling negative.

- Indeed, there are signs that tax hikes earlier this year are starting to bite in the labour market. The baseline is one more Bank of England cut this year to 3.75% and then policy down to 3.50% next year.

- We’re relying on the broadly weaker dollar trend for GBP/USD gains.

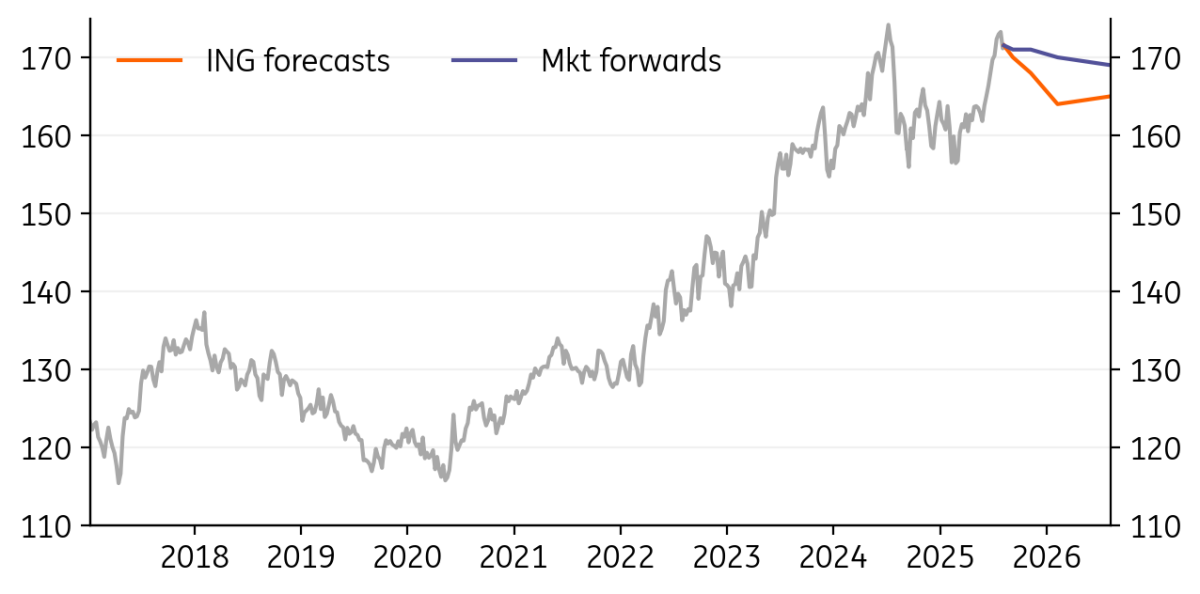

EUR/JPY: Pretty neutral

|

Spot

|

One month bias | 1M | 3M | 6M | 12M |

|---|---|---|---|---|---|

|

EUR/JPY

171.53

|

Neutral | 170.00 | 168.00 | 164.00 | 165.00 |

- We note that EUR/JPY is again pressing long-term resistance in the 170/175 area and that, on a medium-term basis, the yen is cheaper than the euro according to our models. We do tend to favour a lower EUR/JPY over the next twelve months, largely because the BoJ is hiking and perhaps the ECB has not finished easing. We think there is a risk of one more ECB cut in September.

- With regard to eurozone growth, we’re still waiting to see what impact this poor US-EU deal has on business and consumer confidence. Ideally, the removal of the uncertainty would lead to greater business investment and stronger domestic demand.

- Our confidence in a turn lower in EUR/JPY is fading a little, however. Japanese political uncertainty could be the wild card.

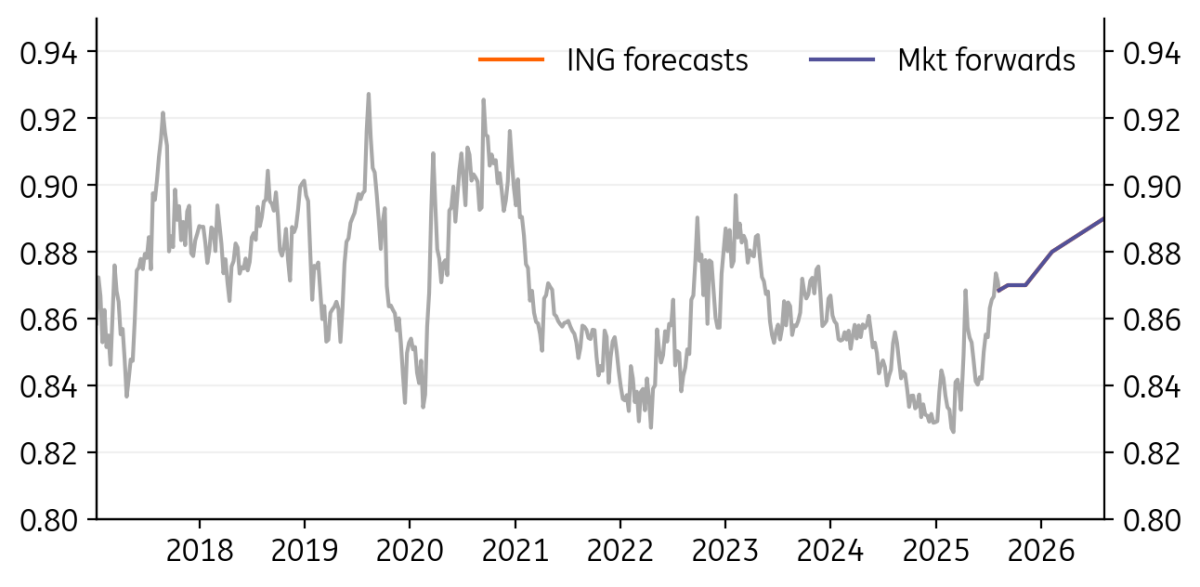

EUR/GBP: Keeping a close eye on the BoE

|

Spot

|

One month bias | 1M | 3M | 6M | 12M |

|---|---|---|---|---|---|

|

EUR/GBP

0.8685

|

Neutral | 0.87 | 0.87 | 0.88 | 0.89 |

- Were it not for the recent BoE meeting, we would have slightly higher year-end forecasts for EUR/GBP. Here, the BoE’s August meeting saw it raise some doubts over how restrictive monetary policy actually was. This questions how low the bank rate needs to be cut next year.

- But our baseline view is that UK activity and inflation does turn lower – perhaps more in the first quarter of 2026 and sterling can stay offered against the euro for most of next year.

- At the same time, we expect the German fiscal expansion to be registering much more in eurozone growth next year. Thoughts of an early 2027 ECB rate hike should send EUR/GBP to 0.90.

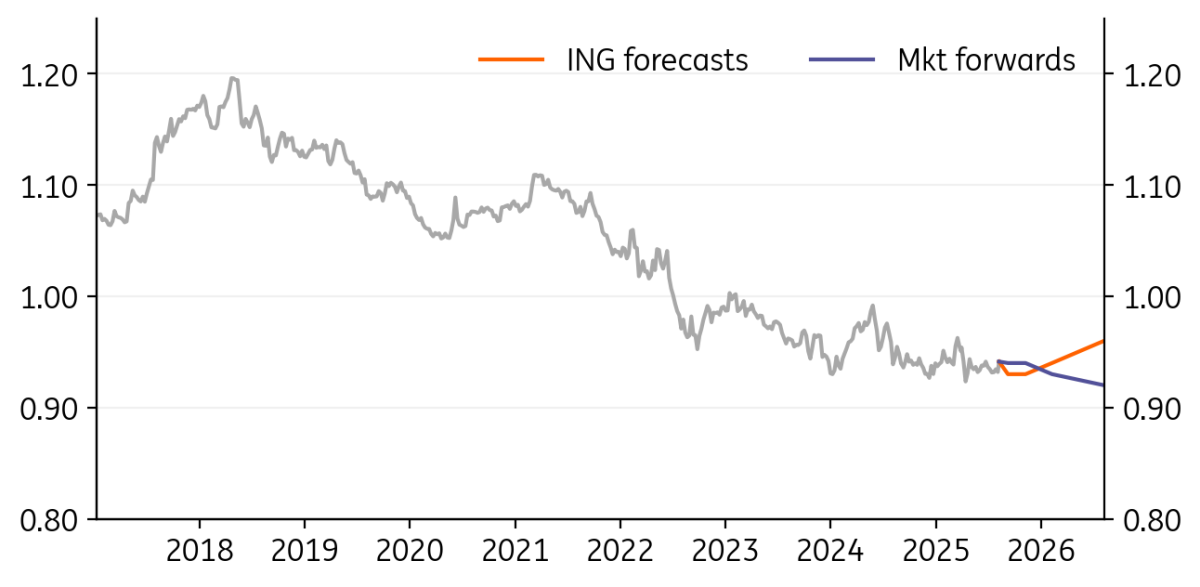

EUR/CHF: Switzerland the unlikely focus of Trump’s ire

|

Spot

|

One month bias | 1M | 3M | 6M | 12M |

|---|---|---|---|---|---|

|

EUR/CHF

0.9413

|

Mildly Bearish | 0.93 | 0.93 | 0.94 | 0.96 |

- It’s not clear what prompted the US to threaten Switzerland with 39% tariffs. On the face of it could have been the $40bn annual deficit the US runs with Switzerland. Or this high tariff is potentially being used as leverage for other deals, e.g., pharma.

- Nonetheless, should high tariffs stick, they will impact 60% of Swiss exports to the US or around $26bn worth of goods. The Swiss government is preparing worker compensation schemes, and presumably the Swiss National Bank will be under pressure to take rates negative.

- Progress on a Russia-Ukraine peace deal is a bullish wild-card for EUR/CHF – but a difficult factor to include in baseline forecasts.

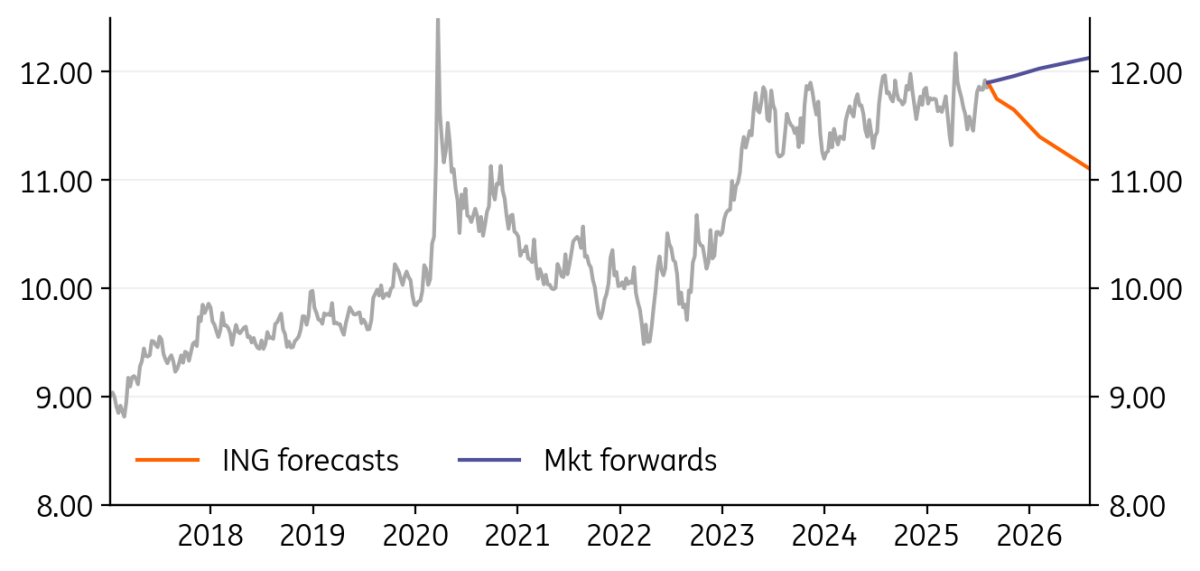

EUR/NOK: Gradual decline still possible

|

Spot

|

One month bias | 1M | 3M | 6M | 12M |

|---|---|---|---|---|---|

|

EUR/NOK

11.90

|

Mildly Bearish | 11.75 | 11.65 | 11.40 | 11.10 |

- A strong euro continues to prevent EUR/NOK from entering any sustainable downward trend. A 7% year-on-year drop in Norway’s June industrial production may be behind the latest NOK move lower.

- Norges Bank is likely to stay on hold in August. Inflation has rebounded, and the krone is significantly weaker since June’s surprise cut. Forecasting future moves remains challenging due to inflation volatility, with pricing likely to shift quickly in response to surprises in underlying CPI, which jumped back above 3% in June.

- Our baseline remains two rate cuts by year-end, in September and December, which are broadly priced in. Combined with earlier Fed easing and potential dovish repricing in the EUR curve, we continue to find the bearish case for EUR/NOK compelling.

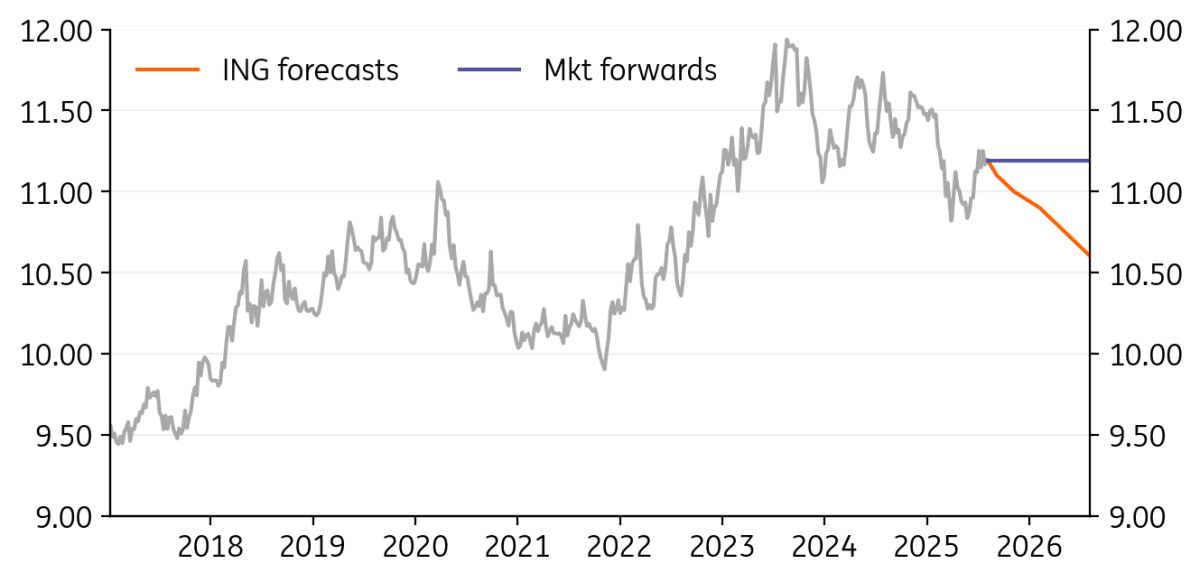

EUR/SEK: US-EU deal weighs on SEK

|

Spot

|

One month bias | 1M | 3M | 6M | 12M |

|---|---|---|---|---|---|

|

EUR/SEK

11.19

|

Mildly Bearish | 11.10 | 11.00 | 10.90 | 10.60 |

- Last month, we viewed market pricing for Riksbank cuts as too dovish. Since then, we’ve seen a hawkish repricing in the SEK 2-year swap rate to just above 2%. Still, EUR/SEK has struggled to move lower, as rising EUR rates and the EU-US deal – perceived as a setback for the EU’s export-oriented economies – have offset SEK support.

- While our baseline remains no further Riksbank cuts, recent macro data have tilted risks more to the dovish side. Core CPIF has slowed to 3.1%, and second-quarter GDP came in below expectations.

- The fundamental case for a lower EUR/SEK remains broadly intact, though with more uncertain timing. SEK is more attractive vs USD, especially if a Russia-Ukraine truce materialises.

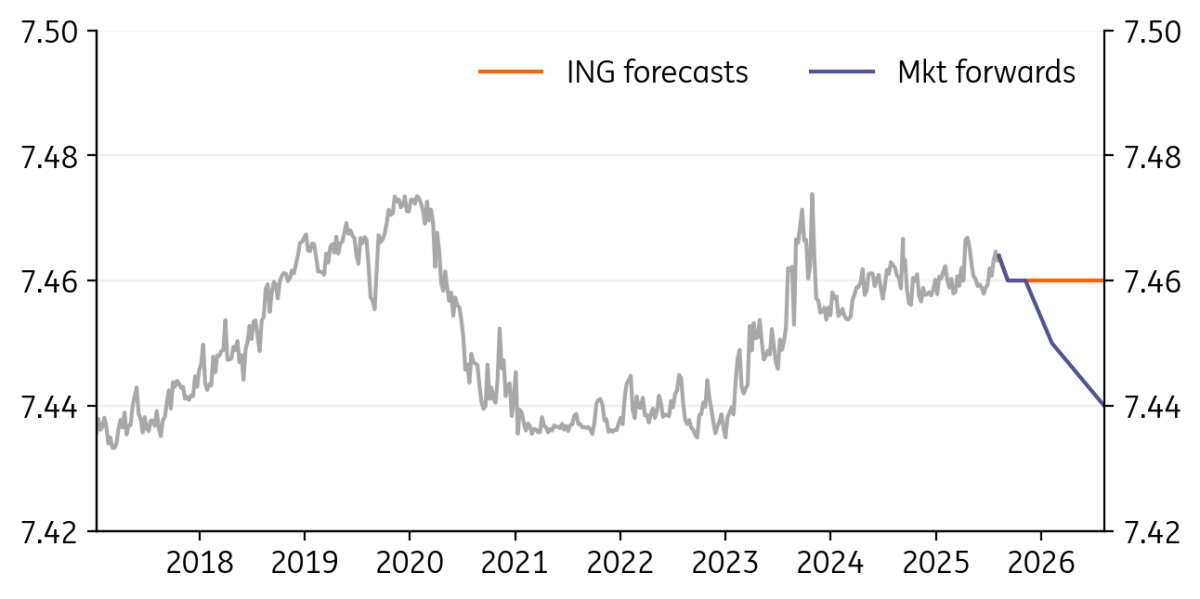

EUR/DKK: Slight upward drift

|

Spot

|

One month bias | 1M | 3M | 6M | 12M |

|---|---|---|---|---|---|

|

EUR/DKK

7.4639

|

Neutral | 7.46 | 7.46 | 7.46 | 7.46 |

- EUR/DKK started to drift slightly on the upside relative to the 7.46 anchor in the past weeks. But these are small moves, unlikely to generate any concerns at the Danish central bank.

- Our ECB call has become more uncertain following latest ECB communication. A September cut remains our base case for both the eurozone and Denmark, but risks are skewed to a later move, or no cuts at all.

USD/CAD: Dovish BoC repricing can continue

|

Spot

|

One month bias | 1M | 3M | 6M | 12M |

|---|---|---|---|---|---|

|

USD/CAD

1.374

|

Neutral | 1.38 | 1.37 | 1.37 | 1.35 |

- USD/CAD had been steadily advancing towards our near-term target of 1.390 before the US payrolls data reversed its course.

- We are flattening our USD/CAD profile due to emerging downside risks for USD. That said, the loonie remains broadly unattractive, and we expect further weakness in the crosses.

- Markets have begun to converge with our dovish Bank of Canada view; a December rate cut is now priced in. We expect it could come sooner, followed by another cut – which is not yet reflected in pricing. Risks tied to existing and potential new sectoral tariffs on Canada may still be underappreciated, and US-Canada trade negotiations have so far proved disappointing.

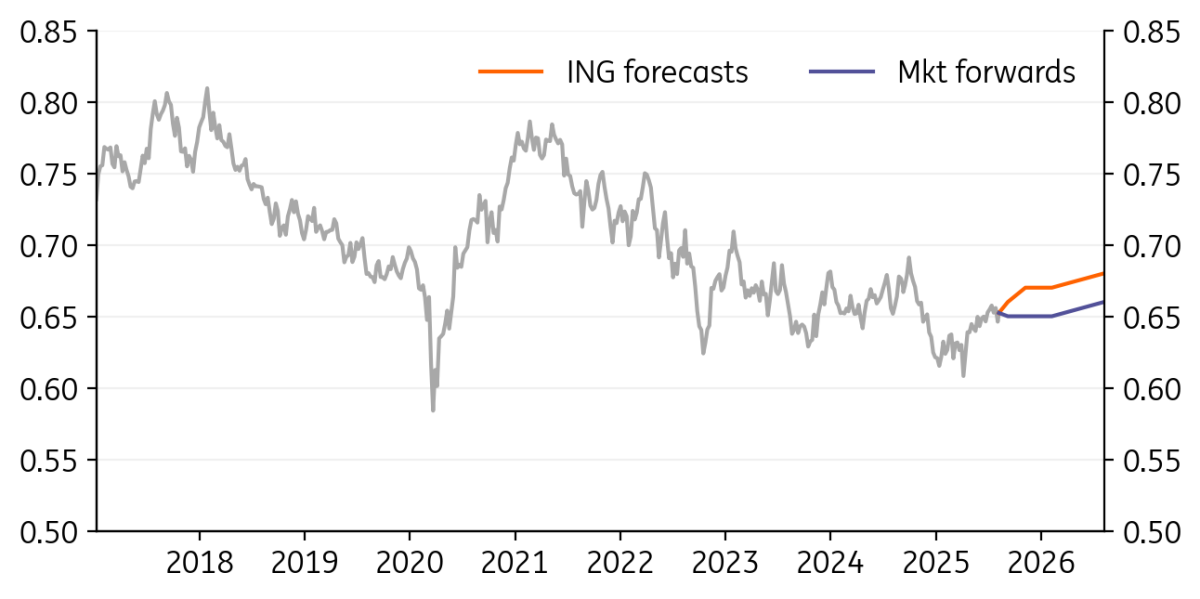

AUD/USD: Aussie looks in a good spot

|

Spot

|

One month bias | 1M | 3M | 6M | 12M |

|---|---|---|---|---|---|

|

AUD/USD

0.6523

|

Mildly Bullish | 0.66 | 0.67 | 0.67 | 0.68 |

- Australia has dodged US reciprocal tariffs (keeping the 10% rate), and pharma exports to the US (likely to be hit by duties soon) are only worth US$1.4bn annually. What matters more for Australian export stability is China’s commodities demand, which is holding up well – as demonstrated by the recent rally in iron ore prices.

- The Reserve Bank of Australia is likely to cut rates to 3.60% on 12 August following a rise in unemployment to 4.3% and a slowdown in inflation to 2.1% in the second quarter. Markets prefer to err on the dovish side of pricing, with 63bp of easing expected for the three remaining meetings this year.

- We only expect 50bp of easing by year-end, and we think AUD is well-positioned to benefit from further USD weakening.

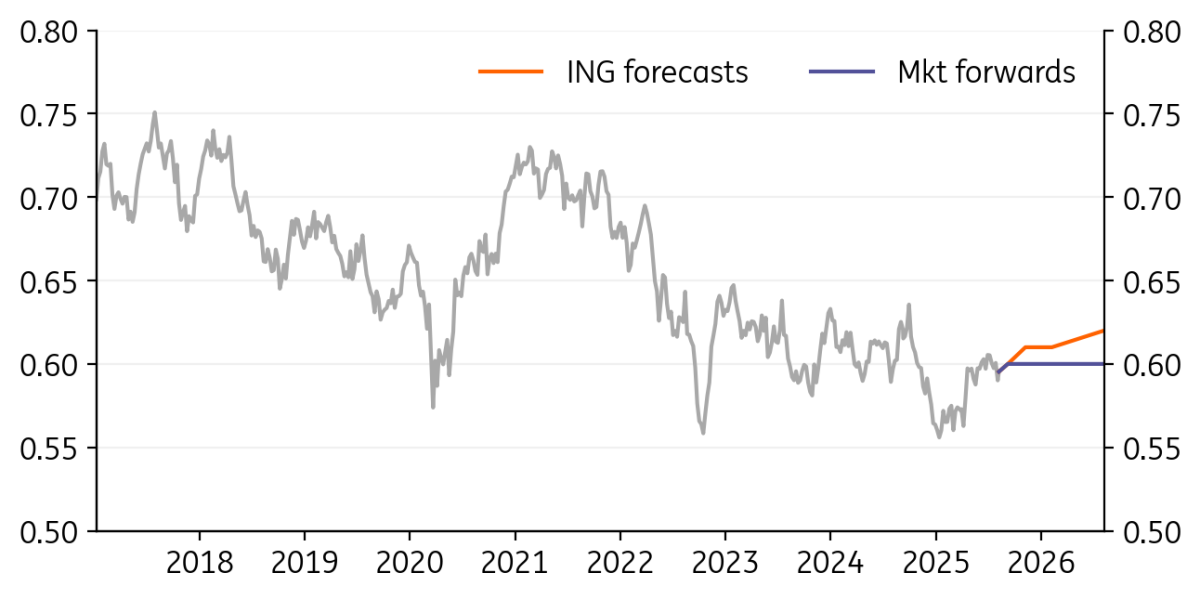

NZD/USD: NZD can lag AUD

|

Spot

|

One month bias | 1M | 3M | 6M | 12M |

|---|---|---|---|---|---|

|

NZD/USD

0.5954

|

Mildly Bullish | 0.60 | 0.61 | 0.61 | 0.62 |

- The NZD curve prices in 42bp of Reserve Bank of New Zealand easing by year-end, close to our forecast for 25bp reductions in August and November.

- New Zealand has been hit by a 15% reciprocal tariff on exports to the US, which are worth around 2% of GDP and 12% of total exports. Meat and dairy are the main components and are not expected to be subject to additional sectoral tariffs.

- NZD appears in a worse position than AUD from a fundamental perspective and we see a decent case for a break above 1.10 in AUD/NZD. But our bearish USD call for the remainder of the year means NZD/USD can make its way back to 0.60 soon.

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more

Authors

Included in the following bundle

Bundle

FX Talking: Cracks in the dollar’s shield

- This bundle contains 6 Articles