USD: A different kind of decline

- 5 December 2019

- FX

The end of US exceptionalism is sparking calls for a weaker dollar in 2020. We think the dollar decline will be far more differentiated than broad-based. We do not think the dollar is particularly overvalued against the euro and Japanese yen. If the dollar does turn lower in 2020, we think it will probably be against the battered commodity currencies

2019 has been a good year for the dollar

2019 has generally been a good year for the dollar. Marginal new highs have been seen in the rally which started in February 2018 – when the White House fired the opening salvos in the trade war. The dollar rally has largely been concentrated against pro-cyclical currencies with occasional exceptions in G10 (Canadian dollar, British pound) and in emerging markets (rouble,Thai baht).

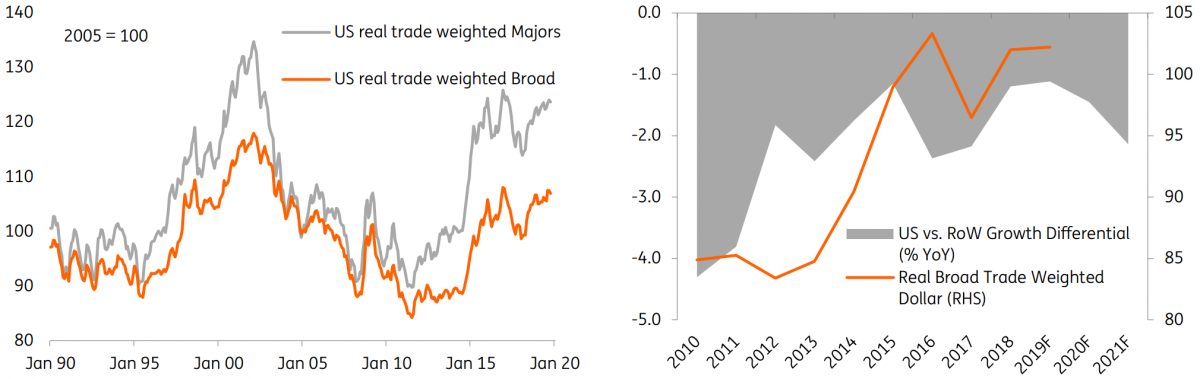

A common expectation for 2020 now seems to be one of broad dollar depreciation. Fund managers are most bearish on the dollar since September 2007 and the familiar narrative is that the end of US exceptionalism spells trouble for the dollar. Certainly we subscribe to the view that the US growth differential against the Rest of the World (RoW) will shift against the US over the next couple of years.

The difference is that we expect the growth performance in the RoW to be far from uniform. Most importantly, 2020 will not be a repeat of 2017 when the world economy was firing on all cylinders (even Europe participated). Back then, synchronised global growth saw trade volumes growing 5% year-on-year and the dollar embarking on a broad decline.

Given our view that Europe will not be a particularly attractive investment destination in 2020 and that the popular DXY is 77% weighted towards European currencies, we are not looking for a major DXY decline next year.

Based on our view of only modest upside for EUR/USD in 2020 (1.13 end 2020) we expect DXY to fall just over 2% next year. If EUR/USD is closer to 1.10 rather than 1.13 at the end of 2020, then that DXY decline is cut to just under 1%.

Dollar nudges higher in 2019, but should it decline as US growth slows?

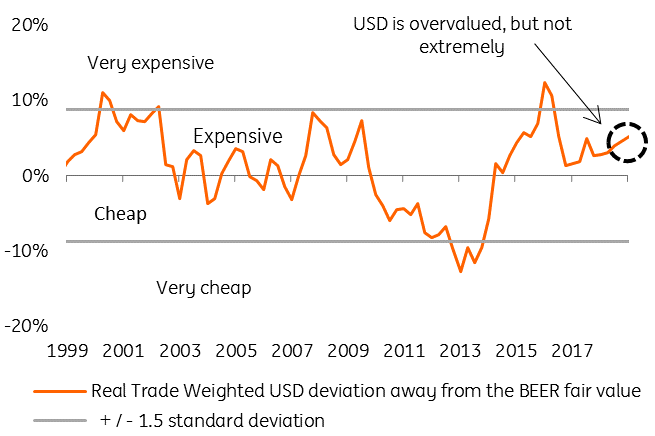

The dollar is not particularly overvalued

We also take issue with some views that the dollar is materially overvalued. Our medium term fair value measures have it nowhere near as overvalued as it was in early 2017, largely because we see EUR/USD’s fair value having fallen to 1.10.

Additionally, we think that the Federal Reserve has to deliver at least three independent cuts (relative to other central banks) to bring rate differentials back into a range that makes a difference for dollar pricing. One of the core stories in 2019 has been that, despite three Fed rate cuts, dollar hedging costs have still been too expensive to make a difference. For example, the costs for European investors to hedge USD exposure have fallen 100 basis points this year, but, at 2.5% per annum, they are still too high in a low yield world.

The yield story is probably more important than we think. Looking at the portfolio flow both from ECB and US Treasury data suggests hot money – or short term financial flows - could be driving exchange rates. For example, we talk about US exceptionalism and the US sucking in capital, but data does not bear this story out.

Through the 12 months to September 2019, foreigners bought only a net US$41 billion of US securities (Treasuries, corporate bonds and equities) versus US$334 billion in the 12 months to September 2018. Instead then we believe short term financial flows are driving dollar strength. Unless the Fed cuts very aggressively in 2020 (e.g. three or more times) we do not see a stampede out of USD deposits.

Dollar valuation based on medium term fundamentals

Will the White House target a lower dollar in 2020?

When it comes to Washington’s FX policy, it is fair to describe this as mercantilist. The White House occasionally rails against the strong dollar, but its biggest bug-bears are the cheap currencies of China and Europe that have contributed to the huge US trade deficit. Should a phase one trade deal with China be signed, look out for any currency clause.

Such a clause may mirror the one suggested in the US-Mexico-Canada deal, which effectively backs a free-float and transparency on FX intervention. In theory, this would prevent massive FX intervention from the Chinese to support USD/CNY should the dollar trend turn lower. Interference with an orderly Balance of Payment adjustment is Washington’s concern.

We doubt that President Trump would turn to physical FX intervention to weaken the dollar – though he does have the authority. And occasional bills in Congress to effectively tax short term capital inflows are unlikely to gain much cross-party support – where capital flow measures are more frequently associated with emerging economies.

G3 currencies relatively subdued, commodity currencies to rebound

In our recently released 2020 FX Outlook: Diamonds in the rough, we made the case that the fresh injection of central bank liquidity from the Federal Reserve, European Central Bank and Bank of Japan would likely depress interest rates and volatility, while also keeping G3 currencies quite range-bound. We roughly see EUR/USD trading in a 1.10-1.15 range (ending 2020 at 1.13), while USD/JPY should roughly trade in a 105-110 trading range.

On a total return basis, we see the Norwegian krone, Canadian dollar and New Zealand dollar performing the strongest against the US dollar through 2020, while in the emerging markets space we see the Brazilian real as the top performer in 2020.

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more

Included in the following bundle

December Economic Update:Prepare to be disappointed in 2020

- This bundle contains 9 Articles