FX Positioning: USD bearish sentiment building up again

All G10 currencies except sterling saw a net increase in speculative positioning against the US dollar in the week ending 4 May, a sign that USD bearish sentiment is rising again. The Canadian and New Zealand dollars now show sizeable net long positioning, likely due to higher rate expectations. GBP’s short-squeeze may have been related to UK politics

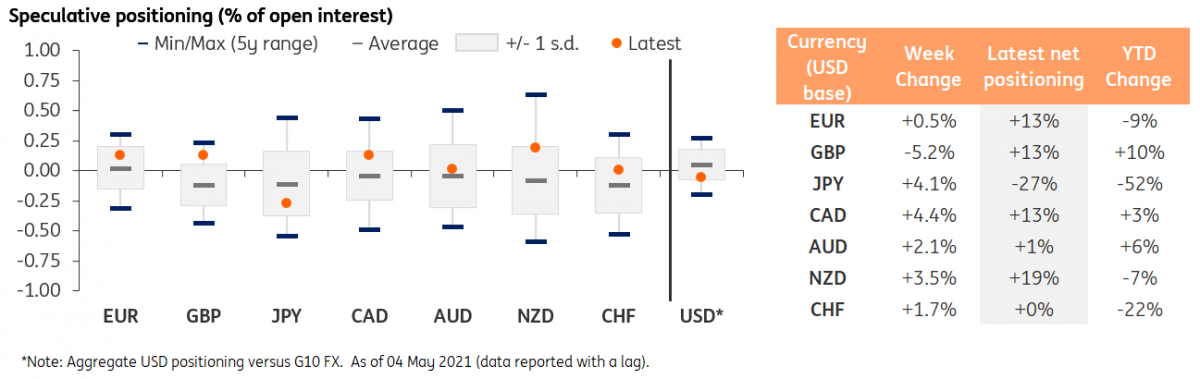

USD net shorts back on the rise

CFTC data on speculative positioning ending 04 May provided clear indications that USD bearish sentiment is consolidating again. The aggregate USD positioning vs reported G10 currencies (i.e. G9 excluding Norway's krone and Sweden's krona) moved deeper into net short territory for a fourth consecutive week, with net shorts now worth 6% of open interest.

All currencies except GBP saw an increase in their net positioning versus the USD in the week ending 04 May. While euro positioning was only marginally changed, currently at +13% of open interest, the yen saw some trimming of its very wide net shorts, possibly aided by the more stable environment for Treasury yields. That said, there is still considerable room for JPY shorts to be unwound considering that it is the only currency with a net short positioning in the G10, currently worth 27% of open interest, although much will depend on the moves in US yields over the coming weeks.

CAD and NZD longs outweighing AUD ones

With the commodity space being broadly supported of late, CAD and NZD continued to see a larger increase in their net longs compared to their closest peer, the Australian dollar. CAD net longs are currently worth 13% of open interest, NZD net longs 19%, both being at the top end of their one-standard-deviation band.

This looks likely to be a function of the diverging monetary policy outlooks within the dollar bloc. The Bank of Canada has been tapering asset purchases and recently signalled it may hike as soon as 2022. The Reserve Bank of New Zealand has retained a bearish stance, but positive developments on the inflation and employment side – along with lingering concerns about surging house prices – are keeping some expectations of a hawkish shift alive. Conversely, the weak inflation profile in Australia is keeping the central bank there firmly tied to its dovish rhetoric.

Incidentally, Australia is facing the short-term risk of escalating tensions with China, which may continue to contribute to the divergence from the rest of the $-bloc in terms of positioning.

GBP: A “political” long squeeze?

Sterling was the only currency that experienced a drop in its net positioning in the week ending 04 May, as its net long positions were trimmed by 5% of open interest, and are now worth 13%. This was a case where positioning and spot dynamics diverged, as GBP/USD was only marginally weaker in the week to 04 May, while the majority of the other G10 currencies performed considerably worse (despite seeing a jump in net long positioning).

There is a possibility that the recent political noise in the UK - with Prime Minister Boris Johnson at the centre - has prompted some speculative investors to cash in on their long GBP bets given the perceived higher risk of political instability in the country. What might also explain the long-squeeze in sterling is that part of the market may have positioned for a less hawkish message by the Bank of England on Thursday and possibly an outcome from the Scottish elections that could have raised the risk of a new Independence Referendum.

All in all, political risk (both regarding the stability of the UK government and the risk of a Scottish referendum) appears to be a secondary story for GBP at the moment, considering that hopes of a strong economic rebound continue to be fuelled by the reopening plans in the UK and this should continue to put a floor under GBP.

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. Read more

Download

Download article