FX Positioning: EUR bulls slowly re-emerging

- 26 April 2021

- FX

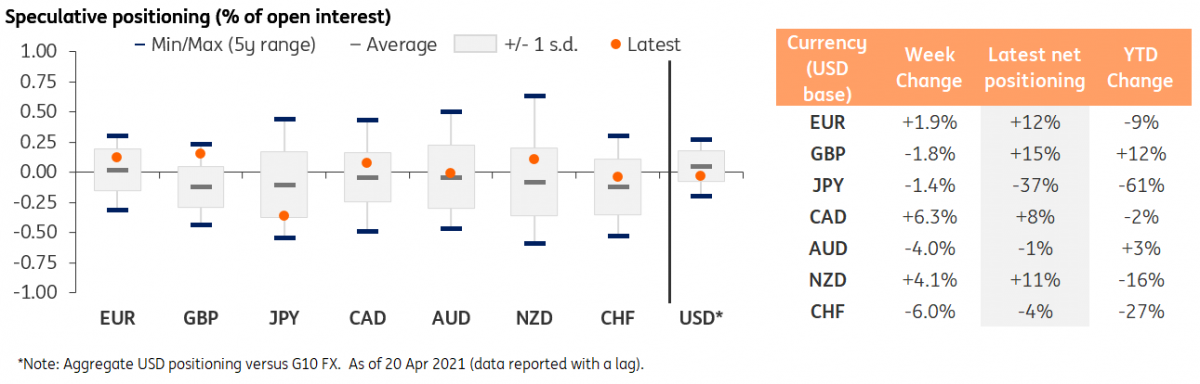

CFTC data shows EUR/USD net speculative positioning moderately rebounding in the week ending 20 April, signalling a turn in sentiment on the pair after an extended long-squeeze. In the rest of the G10, the picture was mixed, as commodity currencies faced diverging paths, GBP and JPY saw a marginal long-trimming, while CHF moved into net-short territory

EUR net longs showing signs of life

CFTC speculative positioning data showed EUR/USD net positioning increasing by 1.9% of open interest in the week ending 20 April, as net longs rose to 12% of open interest. That was the first material increase in net positioning on the pair since January, considering speculators had been consistently trimming their long positions on the euro in 2021.

The move in positioning mirrors the evident change in sentiment on EUR/USD in the second half of April, thanks to a combination of fresh USD weakness and somewhat improved recovery hopes for the eurozone economy on the back of a faster vaccination rollout in the region.

What was already clear from previous CFTC positioning reports was that the benefits to the dollar from the extended trimming of USD net shorts had run its course as the dollar’s aggregate positioning vs the G10 (i.e. G9 excluding Norway's krone and Sweden's krona) moved into neutral territory. The USD was displaying net shorts worth 3% of open interest as of 20 April, compared to 2% o.i. a week earlier.

As shown in the chart above, the euro has further to run in positioning terms (it is still within its 1-standard-deviation band) before its net longs reach extreme levels and before another round of position-squaring possibly curbs the EUR/USD upside. As the vaccination process in the eurozone gathers pace and recovery expectations consolidate, we may well see the EUR net positioning overshooting again to the overbought side.

CHF, JPY and GBP lose some ground

The yen’s net shorts continued to increase in size despite the recent correction lower in US yields, which have a strong inverse correlation with JPY. The currency remains the most deeply oversold in the G10 space, with net shorts worth 37% of open interest. The correction in the yen’s net positioning since the start of the year has been worth 61% of open interest. While there is a stark divergence with other G10 currencies, the yen’s positioning is still within its standard-deviation band.

The Swiss franc appears to be following the yen’s plunge into oversold territory with some delay, as CFTC continues to report an increasing amount of speculative short bets against the franc. As of 20 April, short positions exceeded long positions for the first time since January 2020. CHF positioning has often shown high volatility, so the weekly moves should definitely be read with some caution, but the alignment with the yen’s oversold condition would be warranted by the underperformance of the franc in 2021 (-3.1% vs USD).

Sterling also experienced a moderate drop (1.8% of open interest) in its net positioning gauge, but retained its status as the most overbought currency in the G10. As discussed in last week’s positioning note, we think net long positions on the pound are here to stay thanks to the upbeat expectations on the UK recovery that have been fuelled by fast vaccinations and looser virus containment measures.

CAD bullish bets rose ahead of BoC meeting, antipodeans diverge

The Canadian dollar’s net longs rose by as much as 6.3% of open interest in the week ending 20 April. This would be a counterintuitive move at first glance considering that the loonie had been on a loosing streak against USD due to the worsening virus situation in Canada. However, the rise in bullish bets might be showing how a segment (speculators) of the market was positioning ahead of the Bank of Canada rate (and QE tapering) announcement on 21 April, which eventually did surprise on the hawkish side and prompted a CAD rally.

The other two G10 commodity currencies reported in the CFTC report, the Australian and New Zealand dollars, took opposite directions, with the AUD dropping into (marginal) net short positioning, while the NZD's net longs jumped by 4% of open interest. The recent worsening in Sino-Australian relationships following the decision by the Australian government to scrap the Belt and Road Initiative (which would have allowed increased presence of Chinese companies in Victoria’s infrastructure projects), may be reflected in the next release of positioning data through a further widening of the divergence between AUD and NZD positioning. Indeed, AUD appears to be facing a materially larger set of downside risks compared to NZD at the moment.

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more