FX Positioning: Dollar sentiment stabilised before Fed meeting

After a short-squeezing in dollar net longs in October, the USD aggregate positioning stabilised in the days before the November FOMC meeting, according to CFTC data. GBP had a net-long positioning before the BoE dovish surprise, while NZD advanced further into overbought territory

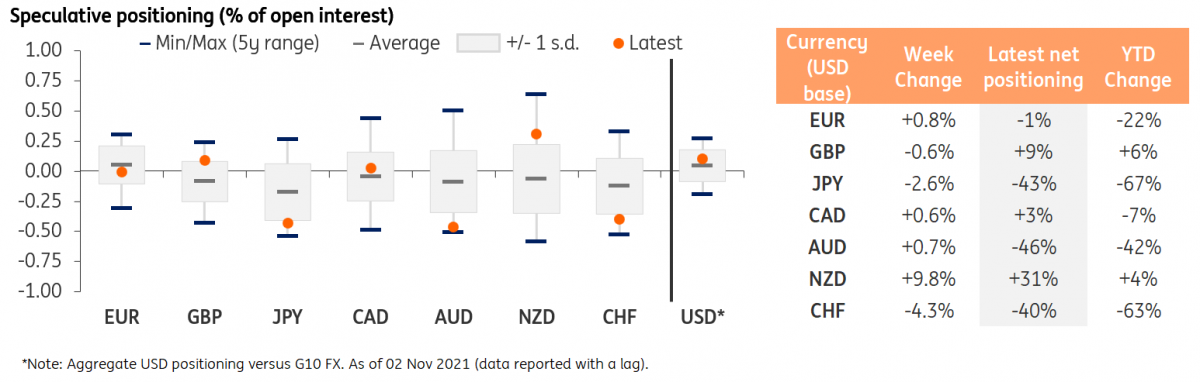

Dollar positions flatten in net-long territory before FOMC

CFTC data on speculative positioning shows that the dollar’s net aggregate positioning versus reported G10 currencies (i.e. G9 excluding NOK and SEK) flattened to around 10% of open interest in the week ending 2 November. The dollar had previously experienced some short-squeezing throughout October, although that dynamic paused in the run-up to the 3 November FOMC rate decision.

The well-telegraphed tapering announcement by the Fed triggered a moderate (and short-lived) correction in the dollar, which may have been caused by some unwinding of USD net longs. Looking ahead, we think that the Fed’s tapering and prospect of tightening are both set to provide support to the dollar and the current USD positioning does not appear to be an obstacle, as it is only slightly above the average and well within the 1-standard-deviation band (in other words, not overstretched).

Speculators were net-long GBP ahead of BoE meeting

EUR, GBP, CAD and AUD saw only very small changes to their positioning in the week ending 2 November, according to CFTC data. The yen faced another increase in net shorts, falling deeper into oversold territory (-43% of open interest).

Like the dollar, sterling approached the week of its domestic central bank meeting with a moderate net-long positioning. Unlike the dollar, GBP positioning at around 9% (of open interest) puts it at the top-end of its 1-standard-deviation band. While that may be read as a signal GBP positions are overstretched to the long side, it must be noted that positioning on the pound had a tendency to be skewed to the downside until 2020 as the currency was embedding a certain degree of Brexit-related downside risk. Despite post-Brexit negotiations having some potential of impacting GBP again, there is little evidence they already are, hence a +9% net-long positioning does not seem overstretched, as things stand.

We expect, anyway, to see a short-squeeze in the pound in the next CFTC report as the 4 November Bank of England meeting saw policymakers surprise markets by holding the policy rate unchanged (a 15bp hike was priced in), which triggered a drop in GBP. In the last two months of the year, we however see the prospect of imminent tightening (we think the 15bp rate increase should come in December) to help GBP recover its post-BoE losses.

NZD even more overbought

The Kiwi dollar is by a large margin the most oversold currency in G10. Indeed, the currency is benefiting from the start of the tightening cycle by the Reserve Bank of New Zealand, good risk environment and a solid growth outlook in New Zealand. Still, the overstretched net-long positioning raises some position-squaring-related downside risk.

In particular, there is a stark divergence in positioning between the Aussie and Kiwi dollars: - 46% and +31% of open interest, respectively. With the Reserve Bank of Australia having made a step on the hawkish direction last week as they dropped the yield-curve-control policy, there is likely some room for the two currencies’ positioning to start re-aligning. Still, that may be a story more for the next year as 3Q restrictions in Australia may keep the data-flow quite unsupportive for longer, while the RBNZ still appears very likely to hike again on 24 November, and retain a hawkish stance.

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. Read more

Download

Download article