FX Positioning: Aggregate USD positions move into net-long territory

For the first time since March 2020, the aggregate dollar positioning vs G10 has moved into net-long territory, according to CFTC data. This was likely due to a combination of hawkish expectations on the Fed and unwinding of reflation trades. GBP and CAD saw the biggest reduction in net positioning in the week ending 20 July

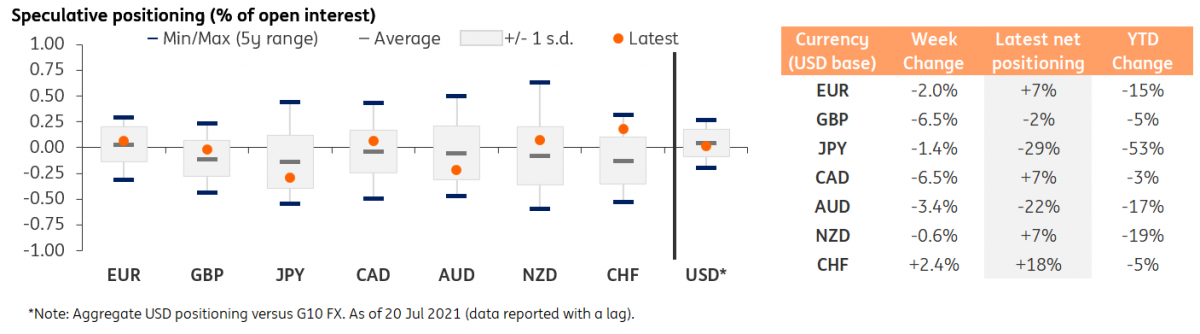

USD positioning jumps

CFTC data show a meaningful change in speculative G10 FX positioning occurred in the week ending 20 July. All G10 currencies except for the Swiss franc (although positioning data on CHF are not very reliable) saw a reduction in their net positioning, and in many cases the drop was quite substantial in open interest terms.

This caused the dollar’s aggregate positioning vs reported G10 currencies (i.e. G9 excluding NOK and SEK) to inch into net-long territory for the first time since March 2020. This is clearly a signal of how the combination of the Fed’s hawkish expectations after the recent shift in tone and the general unwinding of reflation trades has prompted a recovery in USD sentiment.

At the same time, the overstretched long positioning of some currencies likely left them more vulnerable to downside corrections favouring the dollar once the Fed turned more hawkish and the risk environment turned less supportive.

GBP and CAD see largest long-squeeze

While EUR positioning saw a relatively contained drop compared to other G10 currencies, and remains into net-long territory (+7% of open interest), this was not the case for sterling, which saw a 6.5% of o.i. decrease in net positioning in the week ending 20 July. The move made GBP shorts outweigh GBP longs for the first time in 2021. This is not fully aligned with what we have seen in the spot market, where most G10 currencies have performed worse than GBP over the past month or so. At the same time, speculators may start to be pricing in some risk premium related to the post-Brexit EU-UK negotiations on the Northern Ireland protocol, which appear to be at a stalemate.

CAD also saw a very meaningful trimming of long speculative positions. This is, however, not very surprising in our view, as the initial negative reaction to the July Bank of Canada meeting – where another round of tapering was announced – appeared to be a position-squaring event. With the BoC on track to end asset purchases by year-end, we continue to see CAD as a potential outperformer in G10 in the coming months. The more balanced positioning could also favour the recovery in CAD.

In the rest of G10, AUD saw its net positioning dropping further into net short territory (positioning now at -22% of open interest). If we see a significant jump in Australian CPI this week, the market may start pricing in more hawkishness by the so-far ultra-dovish Reserve Bank of Australia and the overstretched net-short positioning may favour some AUD outperformance.

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. Read more