FX: Picking off the doves

- 5 November 2021

- FX

Volatility is rising across FX markets as investors re-price central bank policy. Outperforming currencies have been those where die-hard dovish central banks have been called out for untenable policy settings – such as in Australia. A dovish Fed looks to be called out, too, over coming quarters and is a good reason why the dollar should stay supported

When doves cry

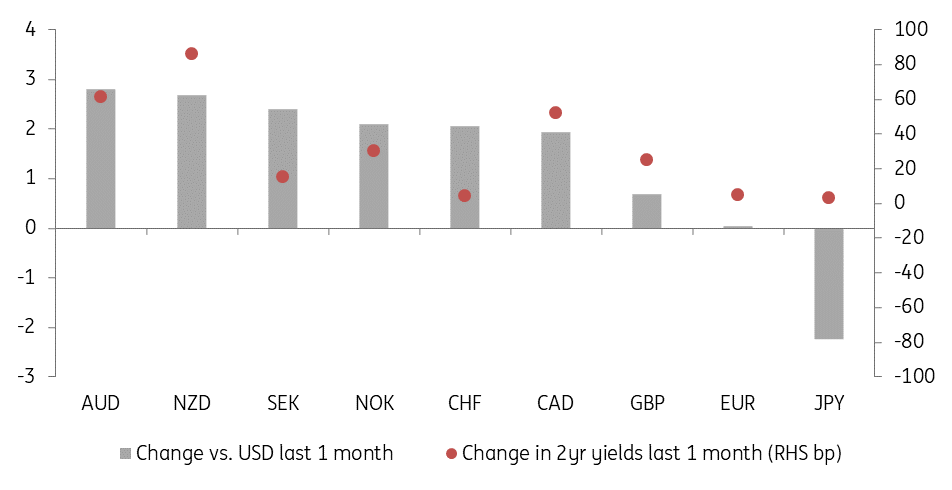

A core theme across international FX and rate markets has been the re-pricing of monetary policy in response to rising inflation around the world. This has come at a difficult time for the most dovish central banks which have tried to hold onto extreme forms of forward guidance. In the Reserve Bank of Australia’s (RBA) case, forward guidance had been backed by a commitment to target the April 2024 government bond at a yield of 0.10%. This week, the RBA abandoned that target with the yield on that bond above 0.70%. The re-pricing of the RBA cycle has surely helped the Australian dollar outperform over the last month.

And it has been a little surprising to see currencies like the Swedish krona and the Swiss franc perform so well recently. It looks again that investors are keen to stress-test the Riksbank’s forecast of keeping the repo rate unchanged until 3Q24 and also the Swiss National Bank’s commitment to resist Swiss franc strength with FX intervention. On that subject, the Israeli shekel is one of the top performing emerging market currencies over the last month as the Bank of Israel has stepped back from FX intervention after buying US$30b this year.

FX changes vs. dollar compared to change in 2yr bond yield

Backing the dollar

If there is a core central bank to be called out on its dovish policy, we think it is the US Federal Reserve. An economy back to pre-pandemic levels, strong momentum into 2022 and headline inflation set to hit 6% suggest there is more re-pricing of the Fed trajectory to be done. That could come through in a more truncated tapering cycle or the Fed formally acknowledging a sharper tightening cycle.

Seasonally, the dollar tends (no guarantee!) to perform well in November and soften in December. We think that may have something to do with financial institutions securing dollar funding in November to meet capital standard requirements such as the Liquidity Coverage Ratio. That could imply that if EUR/USD is to break below major support at 1.15 this year, the best chance of that happening is in November.

Yet even if the dollar does soften in December on seasonal trends – e.g. EUR/USD back to 1.17 – we suspect that many corporates needing to source dollars (especially to pay energy bills) will keep the dollar supported on dips. We retain a 1.10 end 2022 target for EUR/USD.

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more

Included in the following bundle

ING Monthly: Curve surfing

- This bundle contains 11 Articles